Fracking and horizontal drilling get top billing for the past decade’s meteoric rise in U.S. energy output, but don’t forget the overseas buyer in the role of best supporting actor. U.S. production would never have surged as it did without exports — and those exports are now in trouble.

After years of steep rises, trend lines are simultaneously turning negative thanks to COVID-19. From crude oil to liquefied natural gas (LNG) to coal, outbound volumes of U.S. energy commodities are falling, in some cases precipitously.

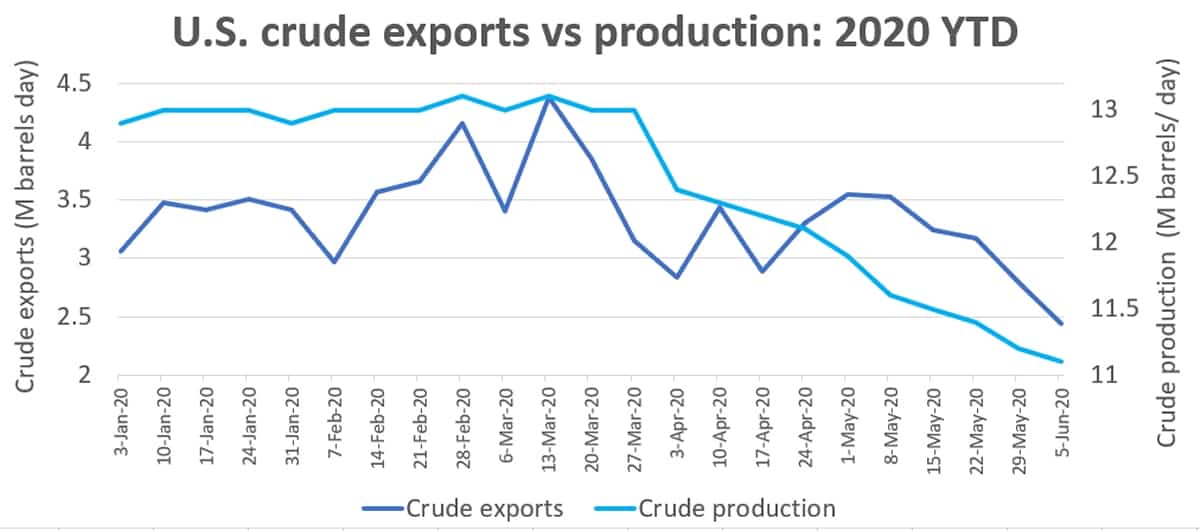

US crude exports on a precipice?

The biggest concern of tanker-stock investors is U.S. crude exports to Asia aboard very large crude carriers (VLCCs; vessels that carry 2 million barrels of crude oil). This trade has an outsize effect on the VLCC supply-demand balance — and thus, spot rates — because the voyage is so long; it’s 2.4 times the distance from the U.S. Gulf to Asia as it is from the Middle East.

The first concern on U.S. exports centers on floating storage. Record volumes have been loaded aboard ships at anchor, awaiting buyers.

The June 6 decision by the OPEC+ coalition to extend production cuts through July is expected to bring forward and accelerate the drawdown of that floating storage, most of which is already pre-positioned in Asia.

Why buy 2 million barrels of crude at the terminal in Texas, pay to have three smaller Aframaxes (tankers that carry 750,000 barrels each) “reverse lighter” (transfer) the crude to a waiting VLCC offshore, then pay over $50,000 a day to sail the VLCC to the other side of the globe via the Cape of Good Hope, when an equivalent load of crude is sitting in a VLCC at anchor off Singapore?

The second concern on U.S. exports involves production. Lower production in the Permian Basin equals lower pipeline flows to export terminals on the Gulf Coast. The Energy Information Administration (EIA) forecasts that U.S. production will fall from 12.3 million barrels per day (b/d) in 2019 to 11.6 million b/d this year and 10.8 million b/d in 2021.

These concerns appear justified. U.S. crude exports are already falling and the pace looks poised to accelerate, which could decrease tanker demand measured in ton-miles (volume multiplied by distance) in the months ahead.

Argus Media, citing data from the U.S. Census Bureau, reported that U.S. exports fell from 3.71 million b/d in February to 3.56 million b/d in April and 3.08 million b/d in May.

Argus quoted investment Tudor Pickering as saying that exports remained above 3 million b/d in May “almost single handedly” due to Chinese demand, and that in the first half of June, Chinese demand was down sharply — which could push U.S. crude exports below 3 million b/d this month.

Argus reported in a separate article that Chinese refiners bought only a quarter of the spot crude volumes (worldwide, not just U.S.) in the first 10 days of June that they did in the first 10 days of May, due to an overflow of previously purchased crude.

Meanwhile, April and early May U.S. export volumes were inflated by purchases of crude for floating storage — and such deals are no longer economically feasible.

Preliminary weekly estimates from the EIA show U.S. crude exports falling below 2.5 million b/d in the first week of June. The EIA’s exports estimates are following the same downward path as its production estimates.

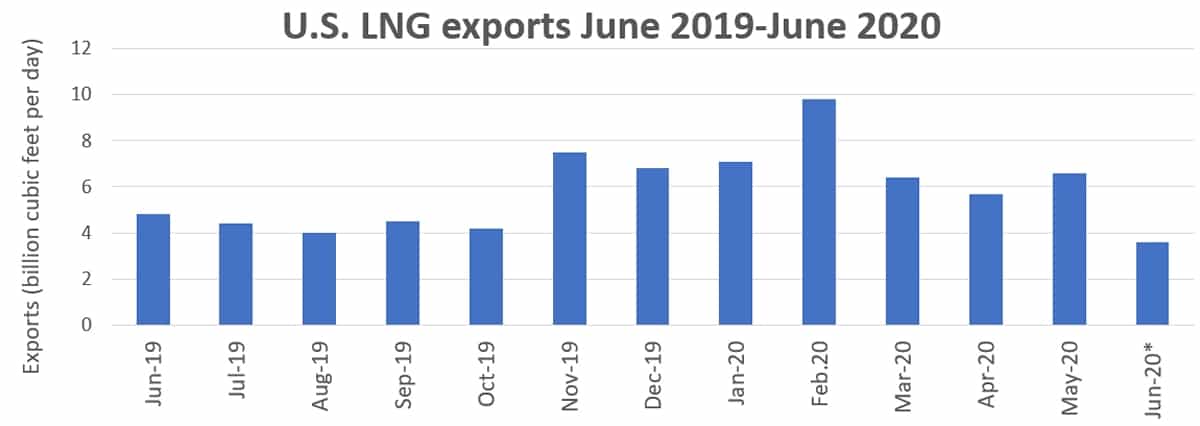

Mass cancellations for LNG cargoes

Just last year, the U.S. LNG export sector was in rapid ascent, with a new wave of final investment decisions (FIDs) for projects on top of those already under construction and the International Energy Agency predicting that America would top Qatar and Australia and become the world’s largest LNG exporter within the next half-decade.

That script has been totally rewritten. The commodity price of LNG sank to all-time lows in the wake of COVID-19, and the spread between the U.S. Henry Hub price and the European and Asian spot prices does not incentivize exports, given transport costs.

According to Stifel analyst Ben Nolan, “Currently, Henry Hub prices are $1.81 per MMbtu [million British Thermal Unit], prices in Europe are $1.66 per MMbtu, and [prices] in Asia are $2.07/MMbtu. At these levels, there is negative economics in shipping LNG from the U.S. to either Europe or Asia. Consequently, U.S. exports have been falling dramatically.”

Evercore ISI analyst Sean Morgan reported that between late March and early June, the volume of natural gas flowing to U.S. export terminals had shrunk by over 40% and new FIDs for export projects have “ground to an abrupt halt.”

According to Argus, “U.S. LNG buyers have cancelled 25-30 cargoes for June and another 40-45 cargoes may not be loaded in July.”

S&P Global Platts data shows that U.S. LNG exports during the first two week of June averaged just 3.6 billion cubic feet per day, down 45% from May’s full-month average.

LNG spot shipping rates have plunged on lower transport demand. According to Clarksons Platou Securities, spot rates are $31,000 per day compared to $90,000 a day at the beginning of this year $60,000 a day at the same time last year.

“LNG shipping rates are bad,” said Nolan. “In fact, if history is a guide they are at about as low as they can go and from these levels only utilization tends to fall further rather than rates.”

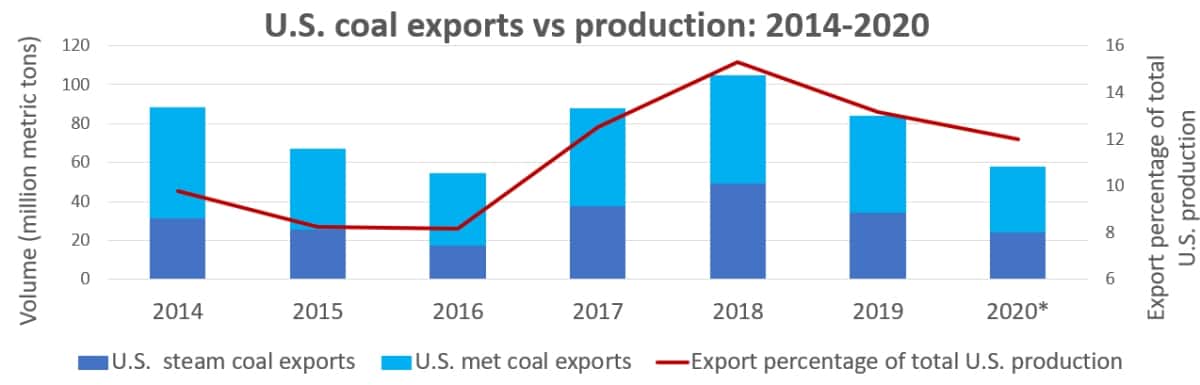

Coal trade collapses

Foreign buyers of U.S. coal threw a lifeline to America’s embattled mines in 2017-18. As domestic demand dwindled in the face of environmental regulation and competition from natural gas, exports helped fill the gap.

That relief proved short-lived. U.S. coal exports fell to 84.2 million metric tons in 2019, down 20% year-on-year, and the outlook has worsened considerably in 2020.

At the beginning of this year, the EIA predicted that U.S. coal exports would drop a further 11% in 2020. The outbreak spurred yet another script revision as ultra-cheap LNG undercut U.S. steam coal in overseas utility markets and demand for U.S. met coal crumbled in the wake of falling steel demand.

In its revised June forecast, the EIA predicted that U.S. coal exports would total only 57.7 million metric tons this year, a year-on-year decline of 31%. The EIA now believes 2020 coal production will fall to 480.8 million metric tons, the lowest level since 1963. Exports would account for 12% of production this year, down from a 15.3% in 2018.

Export and production drops are having a severe effect in the rail sector. Weekly carloads of coal received by Class I railroads (SONAR: RRAILCARCOAL.CLASSI) have slumped to 7,500-9,000 from 13,000-15,000 prior to the coronavirus.

The top four U.S. coal export ports are Hampton Roads, Virginia; Baltimore, Maryland; New Orleans, Louisiana; and Mobile, Alabama. Coal exports from Hampton Roads in April were down 16% year-on-year, to their lowest level since December 2016. Click for more FreightWaves/American Shipper articles by Greg Miller

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now