Once you’ve had prime rib, sirloin just ain’t the same. That is the way this year’s freight market feels: a little more gristle than before. Last year, the Outbound Tender Volume Index peaked at 11,072 on June 22. This year is far from over, but the summer peak may have already come and gone as the OTVI hit 10,585 on June 17h and has fallen slowly ever since to where it now sits at 10,223, 3.5% lower.

Every year is different in some way. Seasonality is defined as a predictable pattern or behavior that occurs around the same time in a cycle, in this case a year. Seasonality does not predict the magnitude of the pattern, only the timing and direction. This year’s seasonal increase in freight volumes is averaging roughly 4% lower in June versus June of 2018.

Not only was the top lower, but it ended sooner.

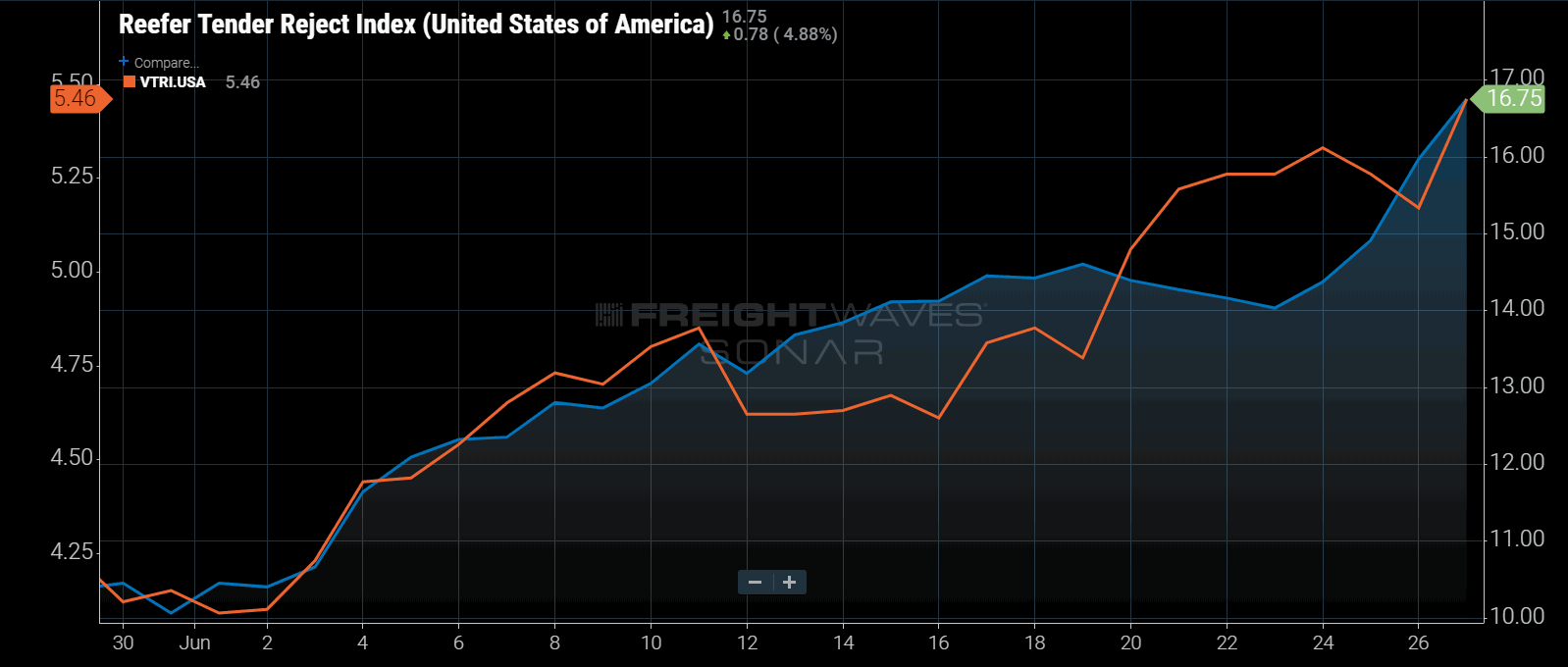

The temperature-controlled segment of truckload appears to be experiencing most of the volatility as national reefer rejection rates continue to climb after taking a brief pause last week. The Reefer Tender Rejection Index (RTRI) increased from 14.03% to 16.75% in the past 4 days. It is hard to discern the impact of the upcoming holiday on this figure. Looking into the data, reefer volumes increased roughly 1.1% versus the previous seven-day period.

The Van Tender Rejection Index rose to 5.46% from 5.06% a week ago, but declined for a few days early-week as carriers were more accepting of freight moving late-week. Unlike reefer dry van volumes have fallen just under 1% from the previous seven-day period.

Much of the volumes continue to move out of the port cities. Markets like Elizabeth, NJ, where the nation’s second largest port operates, are showing a 33% increase in outbound volume compared to 2018. Similarly, Savannah is pushing 37% more volume out of the market than last year.

The larger inland markets, like Atlanta and Chicago, are showing the largest year-over-year deficiencies in outbound volumes. Atlanta is currently averaging over 20% down from 2018 while Joliet is showing 25% off the same period last year.

The volume data suggests there is still a lot of freight available around the port cities, while there is much less activity further inland. The traditional peak of inbound containers occurs in August and September for many of the larger ports like New York and Los Angeles, although the growth of import volumes makes this difficult to discern. It is unclear what impact the tariffs and recent pull-forward will have on seasonal inbound container volumes.

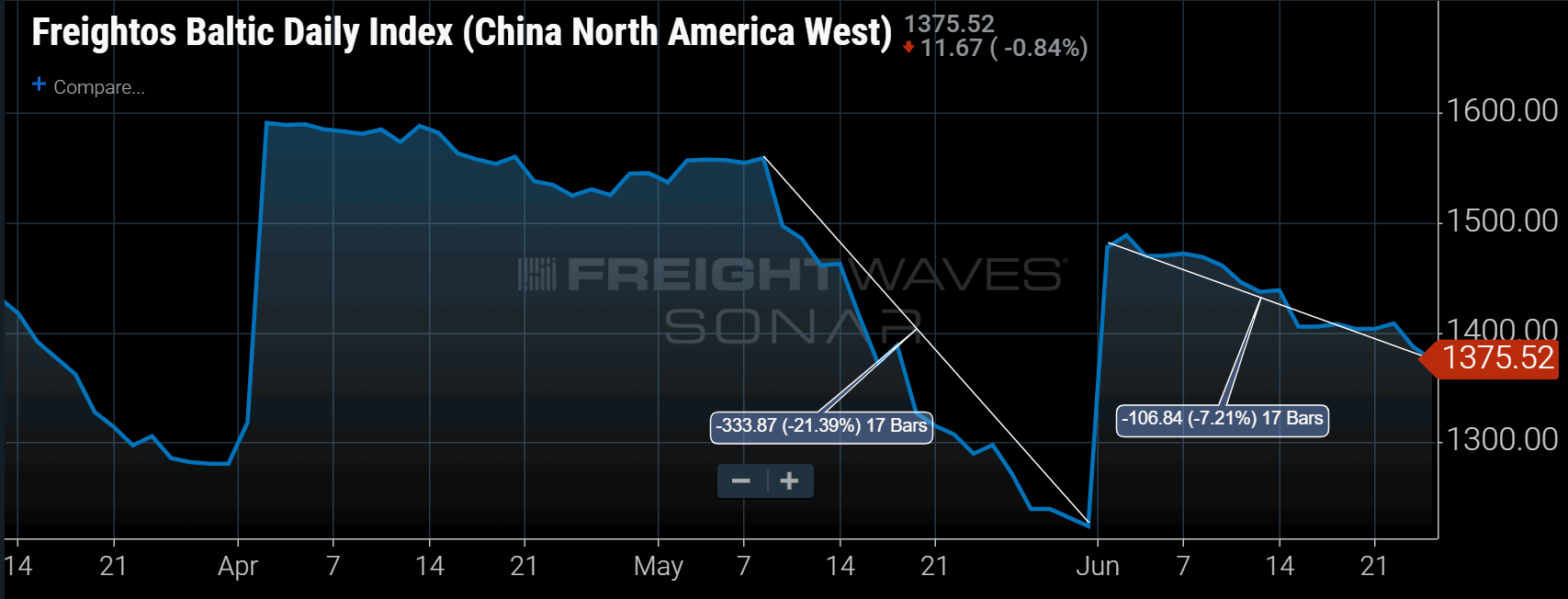

Looking at the Freightos Baltic Exchange Index for China to North American West Coast (FBX.CNAW), which measures the daily spot rate for 40-foot containers moving in the trans-Pacific lanes, the monthly rate increase has been stickier in June versus May. Maritime shipping rates fell 21% from the early May rate increase, indicating significant weakness in demand from China to North America throughout the month. This is also reflected in the tender volume data for the Los Angeles market (OTVI.LAX) where volumes fell dramatically a few days after the tariffs went into place. Maritime rates have only fallen 6% from early June levels in the same lane, an indication that the volumes are better than May in relation to expectation.

July is typically slower than June due to the impact of the 4th of July holiday, so volumes are expected to slide next week, while capacity becomes more limited for all modes due to driver availability.