The truck market is correcting. If you haven’t read the article that FreightWaves CEO Craig Fuller wrote last week titled, “Just 3 years after 2019 trucking bloodbath, another is on the way,” I recommend starting there. For those who prefer a video format and/or want more detail, Fuller discusses his thesis on the most recent Loaded and Rolling episode.

In short, the truck market softened considerably in March, normally a robust month for freight, and the truck market is expected to correct further in the coming months after a two-year period of tightness. Freight demand is declining as the rising prices of essentials, such as food and gasoline, are crowding out more discretionary purchases, like clothing and electronics. Plus, the much-anticipated return to consumption of services instead of goods appears to be upon us. Many shippers’ inventory levels are now highly elevated, as evidenced by a lack of available warehousing capacity in many areas. Meanwhile, truck capacity is coming into the market at a pace faster than most expected, as evidenced by record numbers of new fleet registrations.

Chart: SONAR

What does a loosening freight market mean for CPGs? I’ll start with the obvious. Most clearly, the emerging correction in the truck market means that CPG companies should have an easier time getting their loads covered as carriers are more compliant with contracts, CPGs should be able to negotiate lower contract rates as they come up for renewals, and CPGs should experience fewer of their loads fall through routing guides on to the spot market. For CPGs that utilize rail intermodal, a decline in freight demand should lead to less rail congestion and greater container and chassis availability — which have been major issues in the past year.

CPGs will become carriers’ preferred shipper segment again. It would be incorrect to say that CPG demand is free from elasticity. In the past year, in my view, most CPG companies have been cautious when raising prices in order to not disrupt sales volume and have generally absorbed a couple/few hundred basis points of gross margin contraction rather than raise prices enough to fully offset rising costs. CPGs and grocers justified mid-single-digit price increases to investors, in the face of double-digit price increases, by citing historical elasticities that suggest consumers will accept moderate (mid-single digit), but not extreme (10%+), price increases for most CPGs.

But there is no question that the sales volume of most CPG items are less sensitive to rising prices than most other goods that are bigger-ticket items, such as electronics, and/or products that are sensitive to interest rates, such as autos and construction materials. Recent analyst calls have illustrated that. Last week, General Mills told investors that elasticity has been no worse than historical norms, while this week, Restoration Hardware described furniture demand that eroded quickly in the past six weeks.

As freight demand weakens and the competition for loads intensifies, carriers will seek stable freight to keep their equipment highly utilized. CPG items are considered preferred freight in that market not only because demand is less elastic, but also because they run regular routes, in fairly consistent volumes, from manufacturing facilities to distribution centers — which is key for the efficient use of equipment. As freight markets weaken, carriers often put more of their equipment in the contract market, rather than the more volatile spot market, and CPG loads fit into that strategy well. Therefore, as freight contracts come up for renewal in the coming months, CPGs should find themselves in a more advantageous negotiating position than they have been the past two years and relative to shippers in most other industries.

From the perspective of CPG companies, a looser freight market may help alleviate one inflationary cost segment, but many others remain. Most CPG companies experienced gross margin contraction last year as the costs of ingredients, labor, packaging, freight and outsourced manufacturing rose faster than companies could pass price increases through their retail channels. The highly concentrated packaged meat industry is one of few exceptions where CPG margins widened last year.

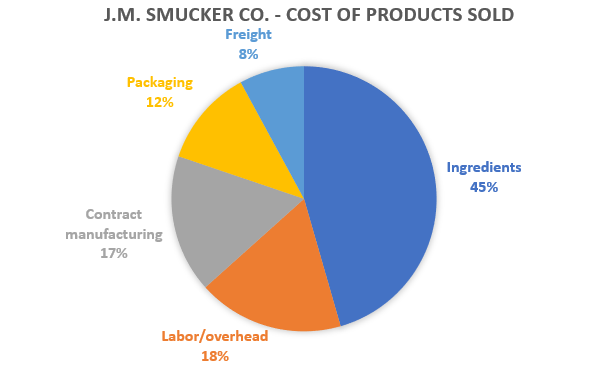

The breakdown of J.M. Smucker Company’s cost of products sold puts the impact of a softer freight market in perspective. CPG companies’ freight costs, as a percentage of their total cost of product sold, are typically in the high single digits to low double digits. The J.M. Smucker Company pegs its freight costs as 8% of its cost of goods sold, which I believe is roughly representative of most CPG companies. Assuming that the emerging thesis of a truck capacity oversupply fully comes to fruition, the most impactful 2022 event for CPGs remains the intensifying inflation in energy and agriculture, following the start of the war in Ukraine, which had led to higher ingredient and packaging costs. As a result, I expect some CPG companies to adjust margin guidance when they report their first-quarter earnings with fewer expecting to restore their margins to pre-pandemic levels this year.

Chart: Company data and FreightWaves

I encourage readers of The Stockout to join us at The Future of Supply Chain event May 9-10 at the Rogers Convention Center in Northwest Arkansas. Keynote speakers include Arkansas Gov. Asa Hutchinson and Jonathan Hoffman, former chief Pentagon spokesman. The CPG industry will be well represented with speakers from Nestle (Greg Kessman, senior director of supply chain) and Tyson (Ildefonso Silva, EVP of business services). Click here to purchase tickets.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, please click here.