XPO registered tonnage growth in the fourth quarter, bucking an industry trend of mid- to high-single-digit declines, on its way to beating analysts’ expectations.

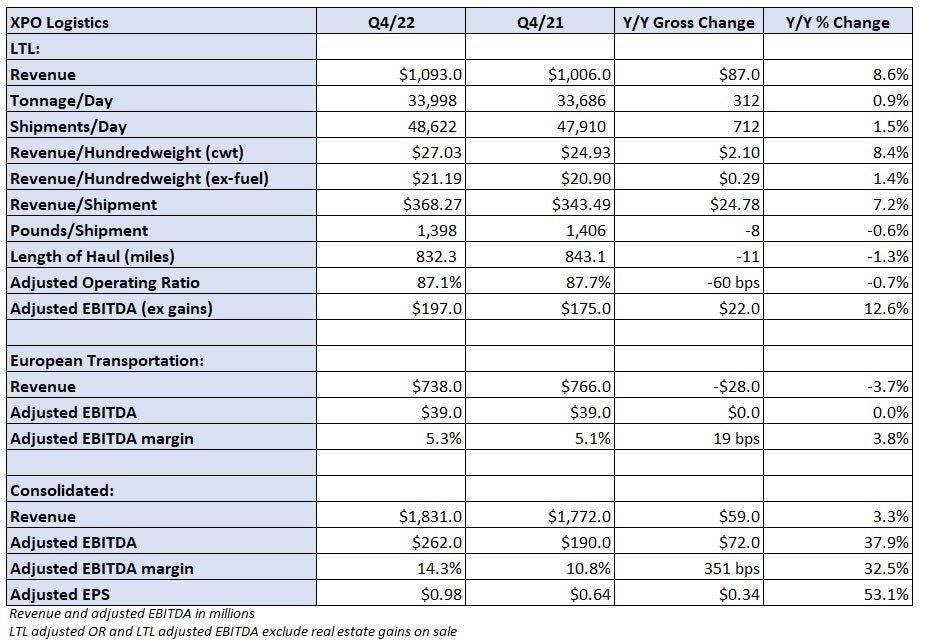

The company reported fourth-quarter adjusted earnings per share of 98 cents Wednesday after the market closed. The result was 14 cents ahead of consensus, according to Seeking Alpha, and 34 cents higher year over year (y/y).

The number excluded several items related to the spinoff of its brokerage unit (NYSE: RXO), a noncash impairment charge in its European transportation business and other acquisition, integration and restructuring costs. XPO (NYSE: XPO) announced in December that it was pulling the divestiture of the European business due to the deterioration in capital markets abroad.

Click for latest XPO earnings story – XPO says it’s ‘not sacrificing price to buy volume’

Adjusted earnings before interest, taxes, depreciation and amortization of $252 million in the LTL segment pushed the full-year figure to more than $1 billion and in line with management’s guidance.

Revenue in LTL was 9% higher y/y at $1.09 billion as tonnage increased 1% and revenue per hundredweight, or yield, grew 8% (up 1% y/y excluding fuel surcharges). Shipments per day were 2% higher but partially offset by a 1% decline in weight per shipment.

XPO had a mix shift toward local shipments with smaller shippers in the quarter. Those customers typically produce better yields but they are more sensitive to declines in macroeconomic conditions. Shipments from the group were up by mid-single percentages but tonnage was down by a similar amount due a reduction in shipment weights.

The company said it saw better than normal seasonality in January and that tonnage was up y/y by an undisclosed percentage during the month.

“Our growth plan for LTL is to invest in capacity ahead of demand and earn market share by providing best-in-class service,” CEO Mario Harik stated in a news release.

Fourth-quarter yields came in at the low end of management’s expectations and below that of peers as the company saw an increase in customers using next- and two-day lanes, which resulted in a lower length of haul (down 1% y/y).

Annual contracts renewed during the period came in 7% higher y/y.

“When you think about pricing overall in the industry, it’s still very disciplined,” Tavio Headley, chief investor relations officer, told FreightWaves.

Adjusted OR in LTL was 60 bps better y/y at 87.1%, but light of management’s guidance calling for 120 bps of improvement. Severe weather in the back half of December and higher than expected labor and maintenance costs were the culprits.

“We clearly drove above industry average tonnage growth and we ended the year at over $1 billion of LTL EBITDA,” Headley said. “We came through on the target that we promised.”

Beginning in the first quarter of 2023, XPO will report ORs in line with that of its peers. The number will exclude pension income and include roughly $20 million per quarter in previously unallocated corporate expenses that were part of its former transportation conglomerate model.

The all-in adjusted OR for the fourth quarter was 90.3% and 86.8% for full-year 2022. The company’s long-term guidance for at least 600 bps of OR improvement by 2027 began at the all-in 2021 OR of 87.6%.

Revenue from the European transportation unit was down 4% y/y to $738 million. However, excluding a drag from foreign currency exchange, revenue was 9% higher. Adjusted EBITDA was flat y/y at $39 million.

The company will host a call with analysts on Thursday at 8:30 a.m. EST. Stay tuned to FreightWaves for continuing coverage of XPO’s fourth-quarter results.

Click for latest XPO earnings story – XPO says it’s ‘not sacrificing price to buy volume’

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now