Less-than-truckload provider Yellow Corp., formerly YRC Worldwide (NASDAQ: YRCW), made it official Thursday after the market close. The company will operate under the Yellow banner again. Yellow will begin trading on the NASDAQ under the ticker “YELL” on Monday.

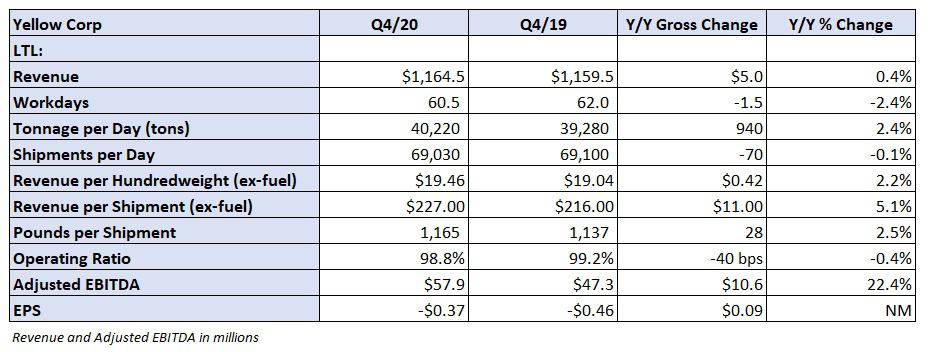

The Overland Park, Kansas-based company reported a net loss of 37 cents per share, worse than the consensus call for a 24-cent per share loss but 9 cents better than the prior-year result.

Yellow is the holding company for LTL brands Holland, New Penn, Reddaway and YRC Freight along with HNRY Logistics. The entities will continue to operate under those respective names until the first half of 2022 when the transformation to a super-regional carrier has been completed.

“As we continue our transformation into a super-regional, LTL freight carrier, it is the right time to reintroduce the Yellow Corporation name and modernize the holding company brand,” CEO Darren Hawkins stated in a press release.

The company’s restructuring has included the streamlining of leadership, sales and technology onto the same network with one point of contact. The turnaround received a boost from a $700 million Treasury loan in July, which allowed the company to catch up on health care and pension benefits payments as well as providing capital to begin replacing its rolling fleet.

“Migrating to one Yellow technology platform and creating one Yellow network are the key enablers of our enterprise transformation strategy, which is to provide a superior customer experience under one Yellow brand,” Hawkins continued.

Fleet replacement accelerates

On a Thursday evening call with analysts, management said it had spent the bulk of the $75 million October draw it received from the $400 million second tranche of the loan. That tranche was allocated for equipment capital expenditures.

Yellow received $176 million in January, which should be exhausted on new equipment purchases — 1,100 tractors, 1,900 trailers and 250 containers — in the next couple of months. The remaining $149 million will be used in 2021 and will include buying out existing leases on equipment. Management guided to $450 million to $550 million in capital expenditures during 2021.

$274 million of tranche A, $300 million in total for the repayment of deferred benefits payments, has been used, with the remainder to be distributed in the first quarter.

Fourth-quarter miss

A full-year net loss of $53.5 million was roughly half of 2019’s $104 million loss, which included $11.2 million in costs associated with its term loan refinancing.

Tonnage per day improved 2.4% year-over-year and revenue per hundredweight, or yield, was up 2.2% excluding fuel surcharges. Revenue was flat as there were 1.5 fewer work days in the quarter and yield was down 0.7% including fuel. Contractual renewals came in 5.6% higher during the quarter.

In January, contract prices increased 6% and tonnage per day was up between 2% and 3% year-over-year. The company implemented a 5.9% general rate increase on Monday.

The fourth-quarter operating ratio improved 40 basis points to 98.8%. Increased purchased transportation, 430 basis points higher as a percentage of revenue, was cited as a significant headwind in the quarter.

A lack of available drivers continues to be a challenge. Yellow will add to its driver school network and plans to have 12 academies operating by March.

Adjusted earnings before interest, taxes, depreciation and amortization increased 22% year-over-year and full-year adjusted EBITDA was $191.9 million, well ahead of the upcoming $100 million covenant, which goes into effect in the fourth quarter.

YRC ended the year with liquidity of $440 million and total debt of $1.28 billion.

“During the fourth quarter, volume and pricing continued to improve in a tighter capacity environment. As the industrial and retail segments of the economy rebound, a shortage of drivers is keeping a lid on LTL capacity. Overall, the industry is stable and well positioned for a strong 2021,” Hawkins added.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now