Bank of America said Tuesday it was more bullish on truckload stocks in 2023 as truck demand appears to have bottomed.

BofA Securities (NYSE: BAC) research analyst Ken Hoexter made a rare two-step rating upgrade to “buy” from “underperform” on the shares of Schneider National (NYSE: SNDR) and Werner Enterprises (NASDAQ: WERN). Below-historical-valuation multiples, “truck demand near [the] floor” and a leveling in spot rates were some of the catalysts for the call.

“With a building demand base (according to our Truck Shipper Survey Demand Indicator) and historically attractive valuation levels, we turn more positive on select truckload carriers,” Hoexter said.

His biweekly survey for truck demand returned the first sequential increase in December after falling for 10 straight months. The latest survey update gauging shipper demand for trucks over the next three months (published Thursday) fell 4% from the update at the end of the year. However, it was still higher than the “historic low” set in early November. The demand indicator remains below the average of the past three freight recessions.

The report also pointed to higher operating costs for carriers, which will likely result in capacity exiting the industry and ultimately easing rate pressures.

“We believe these are early signals of a bottoming in freight demand, with a potential inflection in 2H23,” Hoexter continued. “Truckload demand may inflect positive in 2H23 aided by a low base, while capacity adds will slow as smaller operators face margin pressures on materially higher costs and lower rates.”

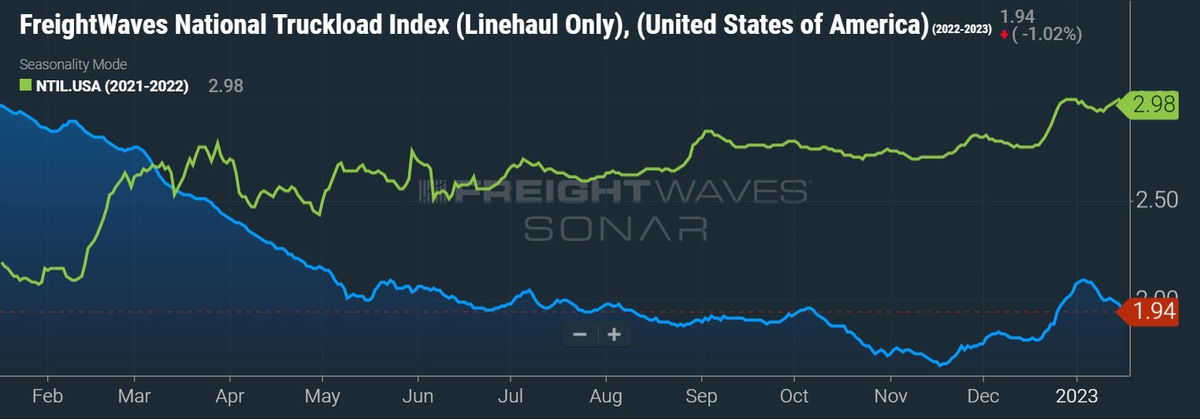

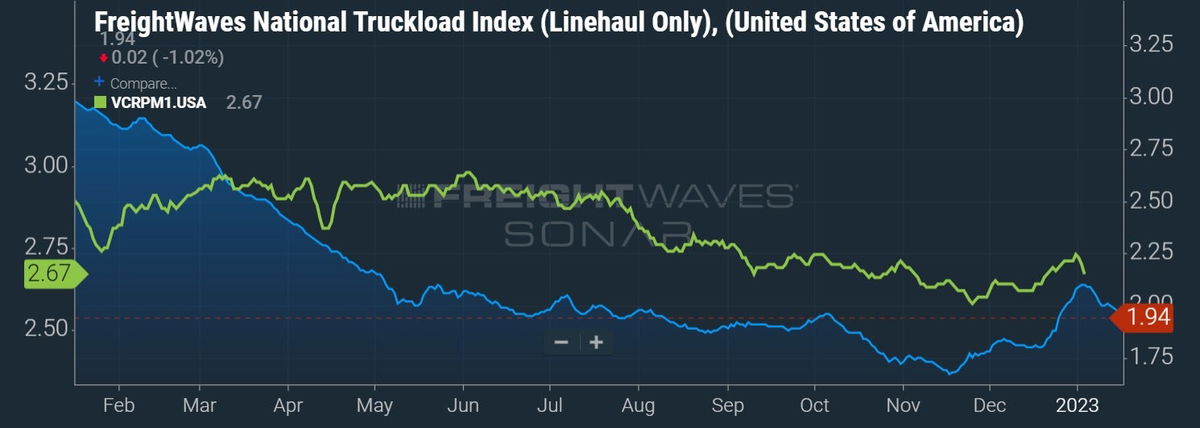

Recent updates in FreightWaves National Truckload Index (linehaul only excluding fuel) shows TL spot rates bounced off a mid-November low but have remained volatile in recent weeks.

Hoexter also noted that the gap between spot and contract rates has closed, as spot rates have moved off lows and contractual rates continue to reset lower. “Given historical correlations between spot and contract rates, we expect contract rates to reach a similar stabilization in roughly 7-9 months.”

He cut 2023 earnings-per-share estimates on the TLs he follows by 6% on average, excluding estimate changes made to underperform-rated U.S. Xpress (NYSE: USX), which he now expects will lose money this year. A buy rating on Knight-Swift (NYSE: KNX) rounds out his TL carrier coverage list.

Several watch items for the group were noted, including new Class 8 truck capacity coming on line as OEM supply chain issues have eased; lower contractual rate renewals; carrier cost impacts from California’s independent contractor rule; and other general inflationary cost items.

Hoexter raised his rating for the shares of less-than-truckload carrier Old Dominion (NASDAQ: ODFL) to neutral from underperform but lowered his outlook on XPO (NYSE: XPO) to underperform. Earnings estimates for the five LTLs he follows were reduced by 5% on average.

“We lower our yield targets for LTL operators as we expect the combination of decelerating volumes, shifting consumer preferences, and moderating fuel prices to weigh on carrier pricing,” Hoexter said.

Volumes for the group fell at a faster-than-expected pace during October and November. December updates won’t be provided until carriers report fourth-quarter results in the coming weeks. Also, a material retreat in diesel prices would present an earnings headwind as fuel surcharges have been more margin accretive in the recent elevated price environment.

He thinks Old Dominion’s highly ranked service will allow it to “seize share from peers” as “the macro environment decelerates.” The rating cut on XPO was tied to potential difficulties the company may have taking market share in a declining volume environment. Hoexter also said XPO’s share price had already moved above his target price.

More FreightWaves articles by Todd Maiden

- XPO taps equities analyst as new chief strategy officer

- Total freight costs fall year over year in December for first time in 28 months

- Analysts make divergent calls on trucking in 2023

Michael Krawitz

When will the USX board realize that Eric Fuller Needs to be replaced