The views expressed here are solely those of the author and do not necessarily represent the views of FreightWaves or its affiliates.

When trying to comprehend what’s going on in complex markets, it’s best to consider multiple expert opinions. It is also prudent to consider different ways to sort the data sets available and then display them against other matched datasets.

The more views, the better the comprehension. In the digital age, there are a lot more sources.

Figure 1 (below) identifies what FreightWaves data scientists like Mike Baudendistel view as a “pull-forward” ocean movement of containers into the U.S. market.

There has been a surge. Not everyone was confident as to the rapid recovery on global lanes. But if you watched closely, you could start to pick out certain lane indicators in mid to late June.

This is important for rail intermodal asset management folks. Why?

Because when these maritime shipments enter via a U.S. West Coast port like LA or Long Beach, there is a corresponding surge in the demand for intermodal train service.

Both BNSF and Union Pacific stand to benefit volume-wise if their business model quickly adapts to a recovery mode coming toward them way out at sea.

A recent daily FreightWaves broadcast (available on YouTube) discussed the pattern that could be watched on a railroad manager’s laptop computer. That’s shown as a graph plot in Figure 1.

You could see in near real time two spikes — the first during late April and into May, and the second in late July and into August.

When the boxes get off the ship, the logisticians in control are looking for either trucks or trains. It is a competitive business opportunity.

Not every global or domestic lane sees the same kind of traffic volume shifting. Some ports, such as the slide below shows for the Port of Los Angeles, have seen an incredibly significant August surge in container imports. Figure 2 shows that LA pattern. Who was watching that upward line slope since June?

Regardless of expectations, clearly there was an import surge at this U.S. port.

It was an oncoming surge of maritime boxes that has clearly caught the two big Western state railroads BNSF and Union Pacific a bit off guard. How did the railroad asset planners miss that? Or did they see it and somehow just not get themselves reset operationally?

Regardless of the cause, both railroad companies seemed to have found themselves in a bottleneck or congestion situation. They cannot seem to satisfy customer demand.

Evidence from multiple independent parties shows that instead of gaining market share, the railroads are surcharging and rationing their limited supply of available LA-area intermodal “well cars.”

The railroads have waited for decades for the chance to grab market share from trucking — and now they appear to be stumbling. Marketing-wise, that reflects a missed opportunity to demonstrate market relevance.

In the case of a precision scheduled railroading (PSR) high-efficiency-claimed service product, it is an unmet challenge to demonstrate how the so-called PSR model has laid the groundwork for a new era of volume and market share growth.

There will be a market-based audit by shippers and railroad boards to try to figure out exactly what went wrong and why. For the moment, the early judgment is that the market channel for rail intermodal missed the signal of the oncoming ship volumes out over the 14- to 21-day sailing period before the boxes landed at LA.

That suggests that something is amiss with the way the railroads’ logistics and operation models communicate with customer TMS supply chain GPS-based movement database sets.

Market position consequences

A deeper dive to this old railroad economist suggests that the two Western railroads have missed two valuable opportunities to double down on demonstrating their importance to both the Western state ports as well as to global logisticians.

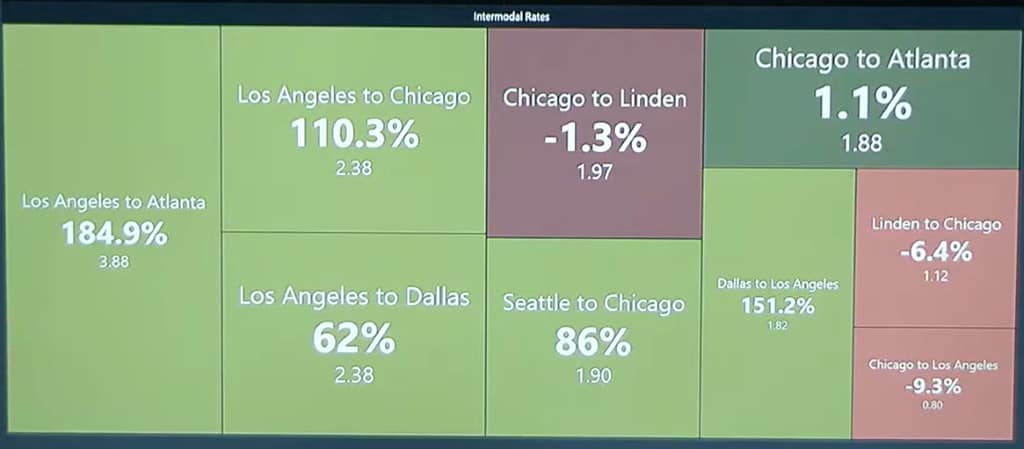

One impact from the railroads’ physical slowness at executing a rapid service and asset redeployment is that spot intermodal rates have ballooned. That leaves a bad experience in place — one that logisticians with their computer models as to mode choice can code up as a historical discount factor.

Railroads can’t afford to have that kind of negative discount factor sitting in logisticians’ vendor selection models.

The rail service shortage and the spot rate jumps were not “small change” adjustments.

Sixty percent to 180% range increases are a wow-like impact. This old railroad guy cannot remember such a huge U.S. rail industry change.

The second possible impact is that the two Western carriers are ignoring the chance to solidify the Western port market share. The Western ports like LA are in competition with both U.S. Gulf and Eastern Coast ports like Houston and Savannah, Georgia. Those ports (and others) have over the past decade been trying to increase their direct China and Asia market import share — at the expense of the West Coast ports.

Diversions from the West Coast ports threaten the two Western major railroad intermodal business units. Diversion of maritime containers to the Eastern and Gulf ports would directly reduce Western transcontinental rail volumes.

Losses of volume to those ports would threaten future Union Pacific and BNSF future margins and cash flow from the lost business.

You do not want to encourage customers to shift port entrances because you failed to deliver when you had the opportunity to do so these past several months.

For maritime containerized goods importers, what it comes down to is a mixture of time to market and cost difference between the two principal coastal entrances to the U.S. market.

And beyond service reliability, the price per container is a critical metric.

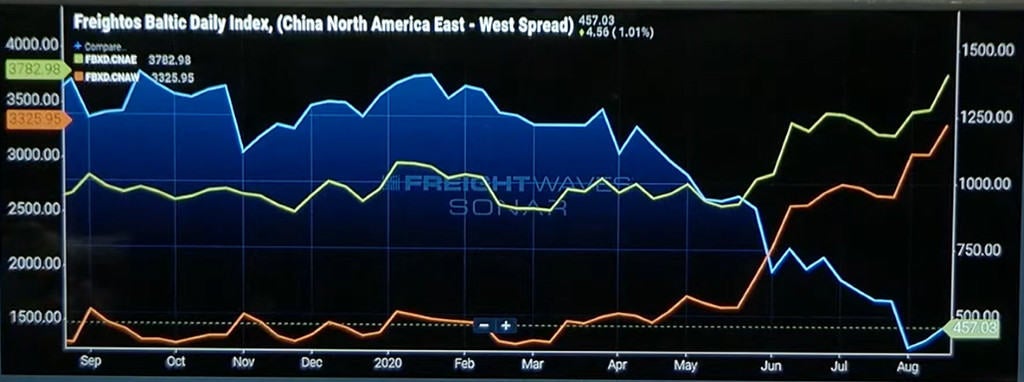

Yet, as the following FreightWaves plot shows, the Western railroads appear to be pricing the West Coast ports and themselves out of much of the market where receivers have a different port supply chain shift option.

In orange, the spot rate differential — largely controlled by the two Western railroad decisions — in effect is directing shippers and receivers toward the East Coast delivery option. A nearly thousand dollar or more price differential that favored the West Coast transcontinental rail option is gone.

That’s a very bad pricing message.

The railroads might argue they are merely using price and surcharges as a means of temporarily discouraging customers from tendering intermodal freight “because they just can’t handle it.”

The two carriers have not yet clearly communicated their marketing intent. Have they?

Here is a major takeaway as we review the issues: If you are hungry for business, you cannot afford in today’s digital age to miss the signals that key market lanes are recovering. Are you ready to service it?

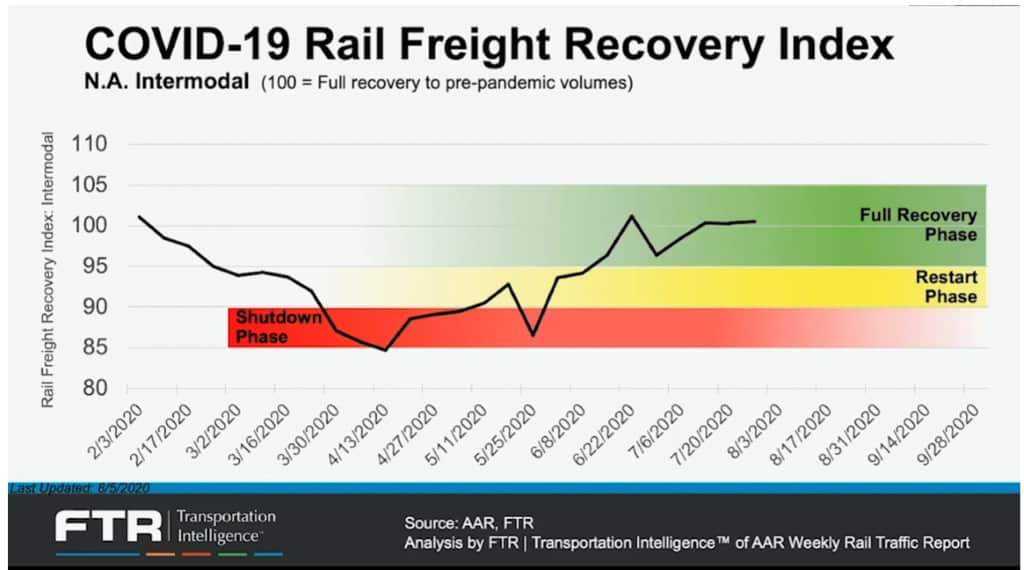

There were signs in June and July of a more rapid selective lane and port intermodal recovery. Another source for that intel is shown in the figure below from FTR.

How did the railroads miss that? Why so long a delay to restore assets like crews, locomotives and cars to the rich, recovering targets?

Intermodal was supposed to be the growth engine for rail. It has not reacted that way.

As always, reader feedback, even if contrary, is encouraged. That discussion is how we all learn.

Commentary: Is outlook for Mexico’s rail freight still relevant?

Commentary: What are the best practices for private railcar storage?

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now