Procter & Gamble highlights the combination of commodity, freight and foreign exchange as having a combined 22% headwind on core EPS in its fiscal 2022 (ending June 30). The company’s organic sales grew 10% in its just-reported fiscal Q3 2022, broken down into pricing, volume and sales mix contributing 5, 3 and 2 points, respectively. Despite 5% higher prices and 170 basis points in productivity savings, the company’s core gross margin contracted 400 bps. The implication is that the company’s costs of products sold rose about 10.7% y/y. P&G’s cost pressure is most acute in its baby care, personal care and fabric/home categories. Any products that use resin as an absorbent material are among the most inflationary. Yet, unlike the fallout of many CPG companies’ results during the past few quarters, P&G’s cost pressure did not surprise the market and the company’s overall performance exceeded analysts’ expectations with shares trading 2% higher Wednesday.

Similar cost pressure is occurring across most of the CPG space, with CPG companies taking significant gross margin hits despite sharply rising prices. There are a few reasons why CPG costs are rising faster than pricing. One reason is simply timing — CPGs have to honor pricing commitments with retailers and cannot immediately raise prices in response to changes in commodity costs. Plus, CPGs recognize that there is at least some degree of elasticity for all CPG products and consumers are much more tolerant of mid-single-digit price increases and more likely to change buying behavior and try cheaper brands when prices rise by double digits. P&G describes this pricing methodology as having a reasonable recovery time (with no specific timeline specified) on the dollar impact of inflation.

A few other takeaways from P&G that may be relevant to other CPGs:

- P&G is not seeing consumers trade down to lower-cost brands, and premium categories continue to sell well.

- Price elasticities are 20%-30% lower than what P&G had assumed.

- The lockdowns in China will be impactful, particularly for the beauty category.

- P&G is ramping up its supply chain investments, particularly in North America and Europe.

- P&G lists the potential for significant further increases in commodity and freight costs as possible headwinds to its fiscal 2022 guidance. In other words, the company is not seeing immediate relief in its freight rates.

J.B. Hunt’s comments suggest that CPGs should expect higher freight rates in 2022. FreightWaves has written extensively about its expectation for a loosening in truck capacity and the slowdown we are already seeing in freight demand. But earnings reports this week from carriers served as a reminder that a bearish outlook does not immediately translate into rate relief for shippers. While FreightWaves’ analysis is forward-looking and expressed a view on how the market will likely develop in the coming quarters, freight rates often reflect the recent history of market conditions, such as the relative tightness in capacity during the most recent peak season. In fact, Shelley Simpson, J.B. Hunt’s chief commercial officer, said she is seeing the best results (from the carrier’s perspective) from contractual negotiations in recent memory. Meanwhile, J.B. Hunt’s core intermodal segment is turning down thousands of loads per week.

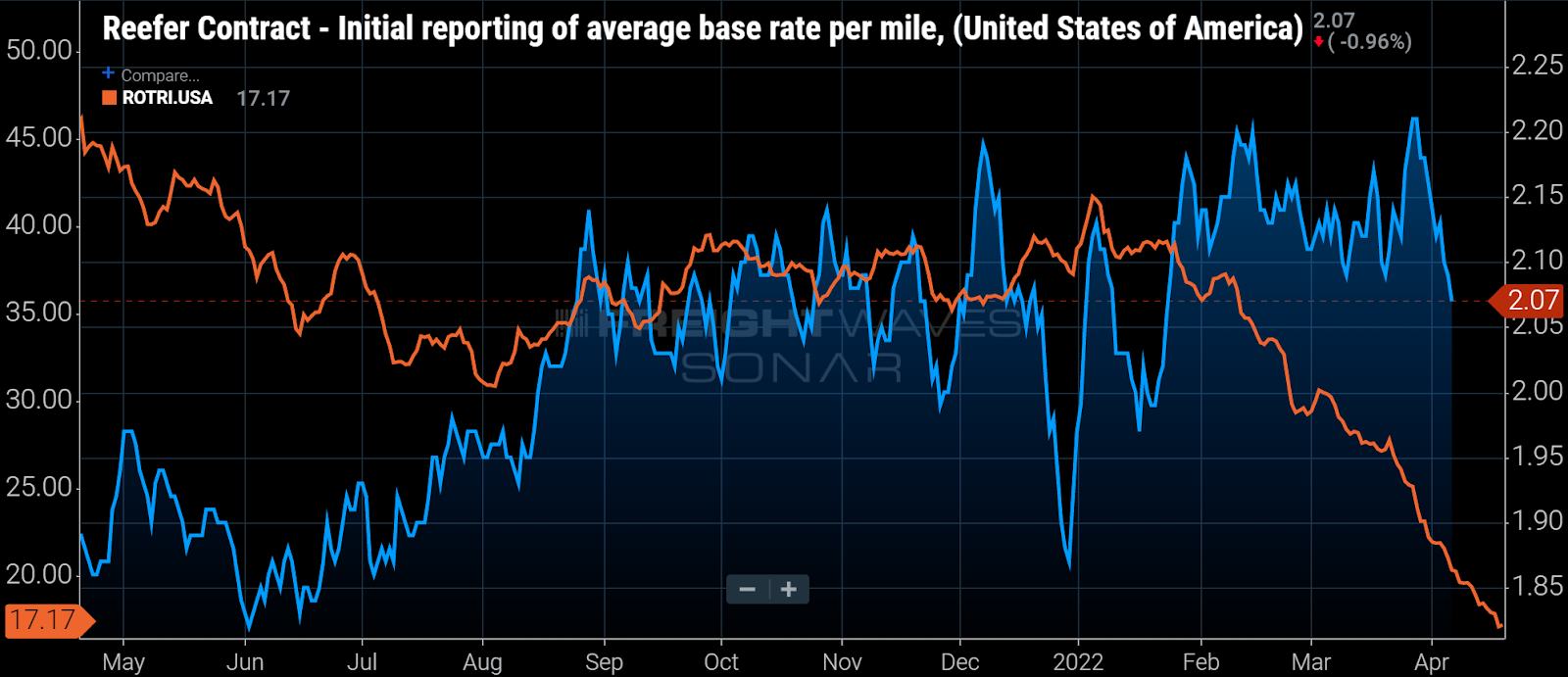

Marten Transport’s results illustrate tightness in reefer. The carrier’s revenue increased 24% y/y in Q1 2022 excluding fuel surcharges or 29% including fuel surcharges. Marten’s operating stats show how much reefer rates have run in the past year and how that has allowed the carrier to operate more efficiently. In the company’s core truckload segment, revenue per loaded mile increased 28.7% on a 7.7% decline in loaded miles. The company managed its fleet for greater profitability with a 22.6% y/y improvement in revenue per truck per week, net of fuel surcharges, which led to a record operating ratio of 85.4%, its best since going public in 1986.

On a separate note, I encourage readers of The Stockout to join us at The Future of Supply Chain event May 9-10 at the Rogers Convention Center in Northwest Arkansas. The CPG industry will be well represented with speakers from Nestle (Greg Kessman, senior director of supply chain) and Tyson (Ildefonso Silva, EVP of business services). Click here to purchase tickets.

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, please click here.