Data was reported last week by the federal government on diesel inventories that was historic in the magnitude of the change from the prior week. It could mark a shift in the weak diesel market that has benefited carriers and drivers for several months.

Ultimately, the price of diesel will be set primarily by the price of crude. But the spread between crude and diesel is also an important factor in the final pump price. That spread has been trending near historic lows for months.

The primary reason has been refiners making too much non-jet fuel distillate relative to demand. Diesel is a distillate; so is jet fuel. The result has been that distillate/diesel inventories in the U.S. and the world have been at historically high levels. (Other products besides diesel in the category would include heating oil.)

That appears to have shifted. The most transparent and immediate numbers are the weekly Energy Information Administration statistics, released each Wednesday for the week that ended the prior Friday. And the numbers that came out last week (Thursday, actually, due to the Columbus Day holiday) were eye-popping when it comes to diesel.

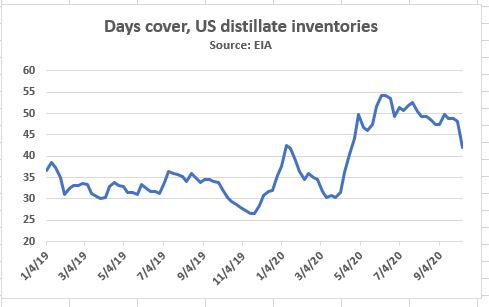

The most easily understood inventory number is “days cover.” That number is reached by taking daily consumption, dividing it into inventories and the result is the number of days of consumption that could be covered by existing stocks.

For distillate inventories that don’t include jet fuel, that number tends to run in the range of 28-35 days. But earlier this year, as diesel inventories began to soar due to changes being made by refiners seeking survival — more on that later — the days cover figure broke above 50 days. In the history of the EIA series going back to 1991, the days cover figure broke above 50 only a handful of times. It was never sustained above that level.

This year, the days cover figure broke through 50 days in late May and stayed above it for nine out of the next 10 weeks. The growth in inventories was unprecedented. It dropped below 50 days in early August but stayed in the 47 to 49 days’ range all through September and into October. That was unprecedented.

But last week, that number plummeted to 42 days, a drop of 6.1 days. It was easily the biggest one-week decline in the history of the series. It meant that in one week, six days of distillate/diesel inventory cover disappeared. That had never happened before.

Why? There were two major contributors to that decline.

The first is that demand for distillate/diesel soared. The fact that it had been lagging was somewhat of a mystery, given the strong trucking market. The “product supplied” figure for distillate/diesel rose to 4.175 million barrels/day in the week ending Oct. 9, the first time it had been above 4 million b/d since the second week of March. A year ago at this time, it was 4.36 million b/d.

Second, refiners made a lot less of it. Since the collapse in air travel, refiners have been doing everything they can to not make too much jet fuel. They’ve largely succeeded; days cover for jet fuel had gotten up to more than 70 days but now is less than 40, which is even lower than distillate/diesel. But to get to that level, refiners needed to shift their distillate output away from jet and toward other distillates.

Refiners have been trying through various means to not only reduce jet output but also to cut back distillate output as well. They succeeded in the first task. The second is harder. Put a barrel of crude through a refinery and you will get some level of distillate molecules. Cutting back on it can be a challenge.

There was another fuel that refiners didn’t want to make during the pandemic: gasoline. As a result, even during the height of the pandemic, distillate output topped 5 million b/d as every effort was made to reduce gasoline output when people weren’t driving. That 5 million b/d figure for distillate is not a crazy high number normally but it is in the middle of a sharp economic contraction.

However, the push to cut back on distillate output has succeeded. U.S. refiners in the week ended Oct. 9 produced 4.279 million b/d of distillates. That’s the lowest number since 2013. It wasn’t easy, but refiners took the steps to start making less distillate, as they already had done to make less jet fuel and less gasoline earlier. (With people driving again, refiners are back to making gasoline.)

The end result: the six-day drop in U.S. days cover, created by a drop in inventories on the back of less output, and a decline in demand.

But it is not just the U.S. In its latest monthly report, the International Energy Agency (IEA) said middle distillate inventories in Europe in September rose just 500,000 b/d. The five-year average is 9.3 million b/d. The result is a graph that showed that inventories are still above the five-year average but are no longer at historical highs. They’ve gotten down to levels closer to earlier highs, still excessive but not chart-busting.

In Asia, the IEA reported that middle distillate inventories rose with historic norms. (Autumn tends to be a time in oil markets of inventory building as the world prepares for winter.)

Although the decline in distillate inventories in the U.S. may have been historic, it hasn’t yet resulted in a significant price reaction. The price of crude has bounced around in the last weeks but ultimately gone nowhere. Brent crude, the world’s benchmark and the more relevant marker for comparison with diesel, was $43.15/barrel on Sept. 17. Last Friday, it settled at $43.32./b

During that time, the front-month price of ultra low sulfur diesel on CME rose to $1.1791/gallon from $1.1598/g. That increased the spread of ULSD over Brent to 14.09 cts/ga from 12.8 cts g on Sept. 17.

But by point of comparison, to show how much all that diesel inventory had held down prices relative to crude, the spread a year ago was about 53 cts/gallon.

The current diesel to Brent spreads aren’t sustainable. Diesel has not entered a permanent, long-term realignment against crude. If the move toward normalcy is going to start anytime soon, it could be that last week’s numbers were the signal that it has begun.

More articles by John Kingston

Good news for diesel consumers, tough news for oil patch drivers in federal report

Labor Day, Roadcheck one-offs catch diesel traders by surprise

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now