XPO’s third-quarter results came in ahead of expectations on Thursday before the market opened. Efficiency initiatives and higher yields pushed operating income higher at the Greenwich, Connecticut-based company’s less-than-truckload segment.

XPO (NYSE: XPO) reported adjusted earnings per share of $1.07 for the quarter, 5 cents higher than consensus and the year-ago result. The adjusted EPS number excluded transaction and restructuring costs. It also excluded a previously disclosed charge of $35 million stemming from environmental and product liability claims at a truck manufacturing subsidiary of Con-way, which XPO acquired in 2015.

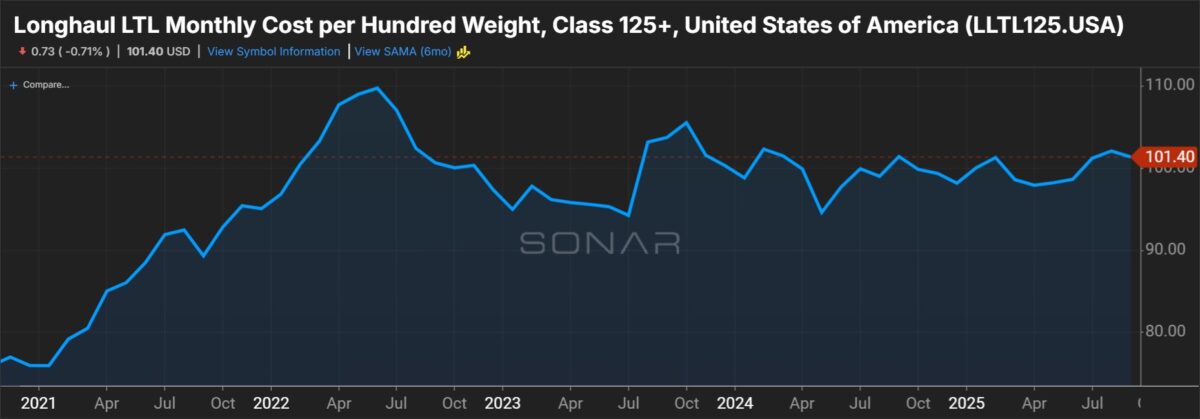

Click for full report – “XPO defies weak LTL demand with margin gains”

Consolidated revenue was up 3% y/y to $2.11 billion, which was ahead of the $2.07 billion consensus estimate.

Less-than-truckload revenue increased slightly y/y to $1.26 billion as a 6% decline in tonnage per day was offset by a 6% increase in revenue per hundredweight, or yield. (Yield was up 3% sequentially, excluding fuel surcharges.) The tonnage decline was due to the combination of a 3.5% decline in daily shipments and a 2.7% dip in weight per shipment.

Both length of haul (up 1.3%) and lower shipment weights were supportive of the yield metric.

Tonnage was off in the period even as the prior-year comps have eased. But the company has been improving its freight mix, which is pushing yields higher. Yield (excluding fuel surcharges) was up 12.6% on a two-year-stacked comparison.

The LTL unit reported an 82.7% adjusted operating ratio (inverse of operating margin), 150 basis points better y/y and 20 bps better than the second quarter. The result was ahead of management’s guidance, calling for no sequential change. (XPO normally sees 200 to 250 bps of OR degradation from the second to the third quarter).

“Our intense execution is resulting in record service quality and margin expansion at the trough of the cycle,” CEO Mario Harik said in a news release. “We’re in the early innings of realizing our long-term margin opportunity, and we expect performance to accelerate as our strategy continues to gain traction.”

Click for full report – “XPO defies weak LTL demand with margin gains”

XPO’s European transportation segment reported a 7% y/y increase in revenue to $857 million, but an operating loss of $2 million was an $8 million y/y swing. Adjusted EBITDA of $38 million was down 14% y/y.

XPO will host a call to discuss third-quarter results on Thursday at 8:30 a.m. EDT.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now