FreightWaves had a chance to talk with Andy Clarke, one of the activist investors looking to reshuffle the deck at expedited trucking company Forward Air (NASDAQ: FWRD). Clarke has held leadership roles with various transportation companies, including his time as CFO at Forward.

A December filing with U.S. Securities and Exchange Commission revealed that a group of investors, including Cleveland-based investment firm Ancora Advisors, Forward’s founder Scott Niswonger and Clarke, intend to make changes at the company to “enhance shareholder value.” Those changes include improvements in the capital allocation strategy and divesting noncore assets as well as making changes to the management team and board.

According to the filing, the group began acquiring shares at the end of October and now holds a 5.3% stake, $89.5 million, in the more than $2 billion Greeneville, Tennessee-based company. Ancora holds the bulk of the group’s investment.

Clarke believes the root of the issue with Forward is lagging valuation. The company’s returns have declined from past levels while its competitors are seeing improvement. He believes the further diversification of its transportation offering is the culprit.

He noted the success other less-than-truckload providers — Old Dominion Freight Line (NASDAQ: ODFL), Saia (NASDAQ: SAIA) and XPO Logistics (NYSE: XPO) — have had in recent years by remaining focused on the core business instead of “making decisions which don’t ultimately add to the value of the franchise and the value of the organization and therefore the value of the shareholders.”

Forward’s recent refocus of operations

The company refocused efforts in 2020, with current Chairman, President and CEO Tom Schmitt saying on the second-quarter earnings call, “We do not wait when we see something, we act with empowered teams, and we remove ceilings.” Those actions have included organic and inorganic initiatives centered on improving volumes and margins.

Forward announced in July that it would start offering a more traditional LTL service, beyond its legacy airport-to-airport routes, in efforts to improve density at its terminals and offset COVID-related demand declines at the airlines and cruise lines, key customers for the company. That service has been added to a few terminals in Forward’s network, including a new terminal in California’s Inland Empire. Additionally, Forward has allocated $40 million to a project at its national LTL hub in Columbus, Ohio, which will increase capacity by 30%.

Schmitt’s goal is to find the “sweet spot” in the more than $40 billion LTL industry, compared to the $700 million of freight it hauls now.

However, Forward’s inorganic efforts have largely centered on acquisitions in non-LTL offerings. In October, it acquired intermodal drayage provider Value Logistics. In September, it added final-mile operator CLW Delivery, which followed larger final-mile acquisitions announced in 2019: FSA Logistix and Linn Star. The company has also added final-mile service to existing LTL terminals to improve facility utilization.

In April, Forward announced plans to jettison its capital-intensive pool distribution segment within the next year. As of its third-quarter filing, the company hadn’t entered into an agreement with a buyer.

Operating ratio reversal

Clarke said he was surprised when he looked at Forward’s investor presentation for the first time in a while. It showed a much broader customer base than in the past as the company has continued to build out multiple transportation offerings.

“I don’t think we’ve seen the evidence that there is a strategic overlap between that core expedited airfreight LTL or near-airfreight LTL and that drayage business,” Clarke said. He said it’s left a “diffusion of focus” throughout the different initiatives.

He said that the company needs greater IT investment to bulk up all of the different offerings, “but to what end,” Clarke added. “Is there cross-selling, [are] there synergies, are there overlaps. Can you cross-utilize those terminals? Can you cross-utilize assets, resources, whatever it is? And if that’s the case, I just don’t think they’ve made it from a financial returns perspective.”

Of note, Forward’s consolidated operating ratio, operating expenses expressed as a percentage of revenue, has continued to deteriorate from the high-70s in the mid-2000s to the low-90s more recently. Forward’s expedited LTL segment had been operating at a mid-80s OR in recent years but that level has worsened.

The division reported an 87.1% OR during the 2018 freight boom, the last year expedited LTL results were broken out separately. The expedited freight segment now encompasses LTL, truckload and final mile. The division posted an 89.8% OR in 2019 and 91.7% in the third quarter.

By comparison, Old Dominion posted a company record at 74.5% in the same quarter and Saia reported 180 basis points of improvement at 88.5%. XPO posted a 79.7% OR, low-80s excluding a gain on sale, bouncing back from the 90.1% posted in the second quarter when the company didn’t adequately adjust for COVID-related cost increases amid weaker tonnage trends.

The overall LTL margin trend for the industry has been that of improvement over the past decade as carriers have regained price discipline, following an attempt by some to force a financially wobbly YRC Worldwide (NASDAQ: YRCW) to fail by aggressively cutting rates in 2009.

Forward’s management noted on the third-quarter earnings call that the 230-bp year-over-year OR reversal was the result of an increased reliance on brokered power, especially on the West Coast, which resulted in a 440-bp increase in purchased transportation expenses, well ahead of only modest increases reported by other carriers.

Management said the OR improved off of a 95% mark in the second quarter to 92.9% in July, reaching 90% by the quarter end in September. The company responded to rising transportation costs by implementing several surcharges in the fourth quarter. In October, tonnage was up 6% year-over-year, but management noted it was too early to tell if the incremental fees would have a negative impact on demand.

“The fact that their operating ratio has declined and the fact that their cost on a per-unit [basis] has risen as dramatically as it has, it’s outpaced their pricing and their pricing has lagged tremendously. Their pricing has not only just lagged their competitors, it’s lagged their cost,” Clarke said. He believes the expedited LTL market is a good one and that “a real heavy focus on the core business is needed.”

He said other modes like expedited TL and final mile are good business, “they just have to be operated.”

Another concern of Clarke’s is that Forward’s revenue growth is outpacing its operating income growth, and in recent periods the company has grown revenue while operating income has declined. Other carriers are seeing the opposite, posting incremental margins, retaining more profit from each additional dollar of sales. The implication is that the company may be spread too thin and not achieving the synergies gained from continuous refinement and reinvestment in the same business.

“You have issues on cost, issues on pricing. For us, the reason why we like it and the reason why we’re taking the approach we are is that we think there’s a better path forward, for everybody involved,” Clarke said. “Whether it’s on the operation or capital allocation side, we just think there’s a better approach.”

Financial returns sagging

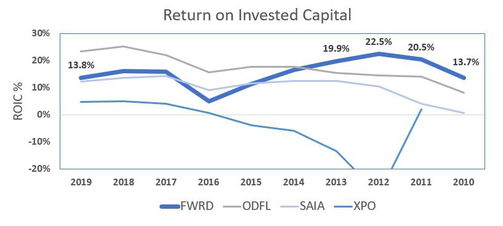

The divergence from the core offering has also resulted in diminished returns, according to Clarke. Forward’s returns on invested capital have stepped lower while competitors have seen increases. The company was generating ROICs in the low-20% range in 2011 to 2013, and significantly higher in prior cycles. Those returns have declined to the 13% range of late.

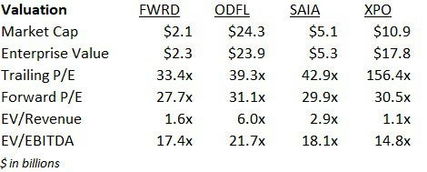

Most telling has been the change in the company’s market capitalization. Old Dominion’s market cap was just north of $4 billion five years ago. Today it’s approaching $25 billion. Saia is 10 times more valuable, XPO five times. Forward didn’t double in value over that period.

Shares of Forward were up only 10% in 2020 versus Old Dominion and XPO, which saw 50% increases. Saia’s shares almost doubled during the year.

Clarke asserts the diversification strategy is the reason for the underperformance in shares. “You get into these other businesses that have decreased the returns. In general, they trade at a lower multiple,” said Clarke. “And then you talk about your capital allocation of spending a billion dollars and [get a] decrease in the returns, how else could that money have been better spent?”

Forward’s valuation metrics modestly lag comparables, following a 30% run in the stock that took multiples a few turns higher. The stock’s rise began when the activist investor group started buying at the end of October. Shares of Saia and XPO have climbed by a similar percentage. But Old Dominion’s multiples have remained mostly level as its shares appreciated only slightly during that stretch.

Management at XPO is hoping for a rerating in value following a planned spin-off of its contract logistics segment. The goal is to shed the perceived conglomerate valuation penalty.

Not their first rodeo

Clarke has partnered with Ancora in the past. In 2018, Ancora took an activist stake in Canadian automotive, truck and equipment fleet manager Element Fleet Management (TSX: EFN), following a failed attempt to sell the company and subsequent sell-off in the stock. In March, the group took aim at discount retailer Big Lots (NYSE: BIG), following lackluster financial results. The plan included board changes and selling distribution centers to improve financial performance and unlock the value of the real estate.

Clarke holds board seats at both of those companies.

Ancora is largely a family wealth investment advisory firm and fund manager led by Chairman and CEO Fred DiSanto. The firm has $7.8 billion in assets under management.

Niswonger has founded other transportation companies in the past, including cargo airline General Aviation and the predecessor of Forward, Landair Transport, which primarily provided time-definite asset-based TL services to the air cargo industry at the time. Landair and Forward separated in 1998, with Covenant Logistics (NASDAQ: CVLG) purchasing the remainder of Landair in 2018. Niswonger is currently running an educational foundation in Greeneville.

Clarke has held several leadership positions in transportation following his 2000 to 2006 stint at Forward. He was the CEO at Panther Expedited Services, which ArcBest (NASDAQ: ARCB) acquired in 2012 and the CFO at freight broker C.H. Robinson (NASDAQ: CHRW) for a four-year period ending in 2019. He is currently the chairman of intermodal chassis provider Direct ChassisLink.

The investor group has met with Forward’s board and management team and will continue to engage in discussion to “create shareholder value,” according to the filing.

Forward plans to report fourth-quarter financials on Feb. 11, but results were likely negatively impacted by a ransomware attack that “may result in a deferral or loss of revenue as well as incremental costs,” according to a separate filing.

Tyrone

Work your salary people into the ground for less competitive wages and the quality will continue to decline. I’ve got videos on how dockmen are allowed to move freight across the dock. Starts with people and with poor culture comes poor quality. Customers should be concerned.