Freight volumes fell faster in July while expenditures stepped slightly higher on a year-over-year comparison. Choppiness in demand created by an uncertain trade landscape continues to overhang the industry, according to a Thursday report from Cass Information Systems.

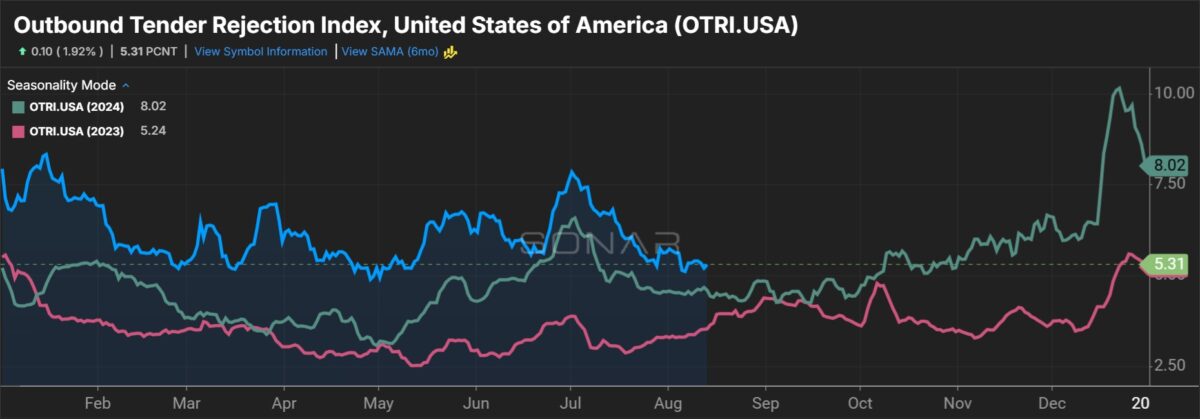

Shipments on the multimodal index slid 1.8% from June (down 1.7% seasonally adjusted) and were down 6.9% y/y. This was the largest y/y decline in the dataset since January. Volumes have fallen sequentially in three straight months.

“Tariffs hit shipments harder in the most recent data, as paybacks began from demand pull-forwards earlier in the year, though goods prices are still relatively steady,” the report said.

The index is expected to be down 8% y/y in August, assuming normal season trends. However, the report said a recent rise in imports may mute some of the expected decline.

| July 2025 | y/y | 2-year | m/m | m/m (SA) |

| Shipments | -6.9% | -7.9% | -1.8% | -1.7% |

| Expenditures | 0.4% | -5.8% | -1.5% | -0.6% |

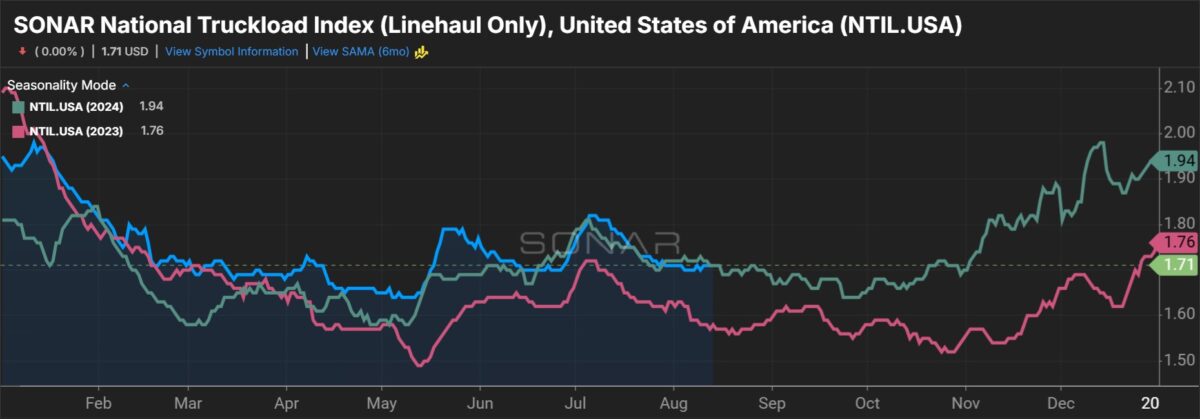

| TL Linehaul Index | 2.4% | -0.8% | -0.6% | NM |

Cass’ freight expenditures index, which measures total freight spend including fuel, declined 1.5% from June (0.6% lower seasonally adjusted) but was up 0.4% y/y. (Retail diesel fuel prices in July were up 5% sequentially but 1% lower y/y.)

The expenditures dataset was positive (y/y) for a fourth straight month in July following over two years of declines. On a two-year-stacked comparison, the declines narrowed again in the month to 5.8%.

Netting the decline in shipments from the increase in expenditures shows actual freight rates were up nearly 8% y/y in July. A mix shift to truckload from less-than-truckload again drove the change to the inferred rate index, the report said.

Cass’ TL linehaul index, which tracks rates excluding fuel and accessorial surcharges, dipped 0.6% sequentially but was 2.4% higher y/y. The dataset has been up on a y/y comparison in every month this year. This was the largest y/y gain since September 2022.

The index is “on track for a small increase in 2025.”

“As the economy is likely to absorb the effects of tariffs over the next several months, our freight demand outlook remains cautious,” the report said. “But the silver lining of lower [commercial] vehicle production and lost manufacturing jobs is that tighter capacity will likely drive freight back to the for-hire market next year.”

Data used in the indexes comes from freight bills paid by Cass (NASDAQ: CASS), a provider of payment management solutions. Cass processes $36 billion in freight payables annually on behalf of customers.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now