Most CPG companies will report earnings next month, but with an off-cycle fiscal year ending May 31, General Mills reported its fiscal third quarter Wednesday morning for the December-February quarter. General Mills’ size and its off-cycle reporting make it a bellwether for next month’s earnings reports. As I’ve discussed in other editions of The Stockout, the inflationary environment in general and rising transportation and logistics costs in particular will have major financial impacts on CPG companies in 2021. General Mills’ (NYSE: GIS) shares traded down on Wednesday after an earnings miss as investors focused on the impact that cost inflation will have on margins.

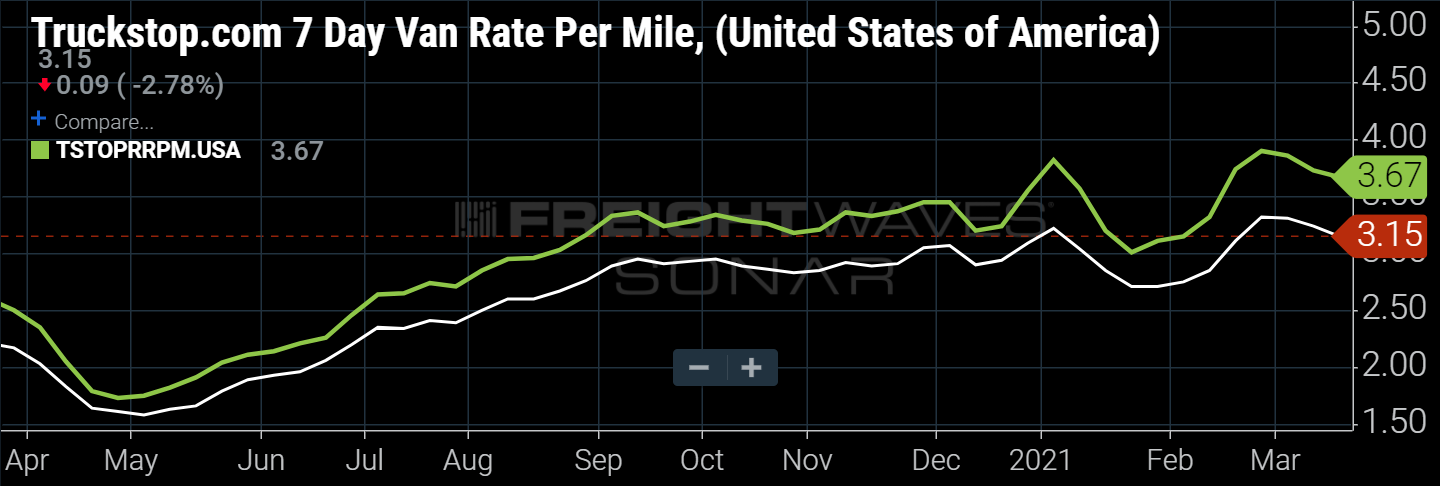

General Mills is seeing mid-single-digit freight cost inflation. As demand has risen, the company has needed to secure capacity in more lanes, utilize the spot market more often and at higher rates, and use external capacity more heavily. That has led to increased cost for delivering to customers and distributors.

Rising costs begin to take a bite out of General Mills’ gross margins. The company’s adjusted gross margin declined 90 basis points year-over-year in its fiscal Q3 driven by higher input costs, higher costs to secure incremental capacity and higher logistics costs. Those cost increases were only partially offset by improved pricing and mix.

That gross margin pressure was new this quarter; in the previous quarters, increased operating leverage associated with higher revenue more than offset the impact of cost inflation. For example, for its fiscal second quarter (the three months ending November 2020), the company had reported a 20-basis-point gross margin improvement year-over-year. I expect gross margin pressure to be seen at other CPG companies in the coming quarters as results are reported next month.

General Mills’ inflation expectation has been adjusted upward in recent quarters. The company expects its fiscal 2021 inflation (the period ending May 31, 2021) to be just over 3%. Management hasn’t given inflation guidance for fiscal 2022 but expects it to increase from the 2021 level. Interestingly, the company tweaked up its fiscal 2021 inflation expectation relative to the prior quarter from “rounding up to 3%” to “rounding down to 3%.”

In light of global inflation, General Mills expects to raise prices more significantly this fiscal quarter. Pricing is a sensitive topic so little detail was provided, but management indicated that it is looking at price increases across segments. Price increases are expected to be viable in the current environment because the inflation is very broad-based and global. It is unclear to me whether most consumer goods companies will be able to increase pricing enough to preserve margins in the coming year since food/beverage pricing has been generally fairly muted (low-single-digit growth for many of the large CPG companies) to this point.

General Mills expects an ongoing elevated level of demand for “at-home” products. Management does not believe that there will be a quick “snapback” in consumer behavior away from eating at home with many workers not returning to the office or only doing so a couple or a few days each week. An early indication is in Texas and Florida, which have been quick to reopen, but with relatively little change in consumer behavior.

Prolonged adjustments in consumer behavior benefit certain categories such as cereals and breakfast foods and hurt other segments, such as energy bars, that are typically consumed on the go. With the company’s overall revenue mix weighted toward at-home consumption, on a net basis, management believes that many analysts are overestimating the deceleration in the company’s net sales growth as a result of the world getting through the worst of the pandemic.

Consumer goods companies are investing heavily in advertising to build their brands. Many CPG companies believe that the pandemic created a once-in-a-lifetime opportunity to engage with customers who are normally difficult to reach, including on-the-go millennials who spend little time shopping inside of stores. To that end, consumer goods companies have ramped up their spending on advertising. General Mills is no exception, with 12% y/y growth in media spending in its fiscal third quarter. Much of that growth has been related to General Mills promoting its growing segments of premium pet food under The Blue Buffalo Company brand. Pet food has been the company’s fastest-growing category, which has also been true of Nestle, the world’s largest food company, and is related to the consumer trends of pet adoption during the pandemic and feeding pets higher-quality foods.

On Tuesday evening, General Mills announced the proposed sale of its European Yoplait business. The company announced that it had entered into an agreement to sell its 51% controlling interest in Yoplait to Sodiaal, a French dairy cooperative, in exchange for full ownership of the Canadian Yoplait business and a reduced royalty rate for use of the Yoplait and Liberte brands in the United States and Canada. Similar to actions taken by other CPG companies, the divestiture appears to represent the company focusing on its stronger products; traditional yogurt has struggled of late, losing share to Greek yogurt and dairy alternatives.

To receive this newsletter, please join us here: https://web.www.freightwaves.com/thestockout