Back in May, we warned that a second-half rebound in U.S. containerized import volumes was highly unlikely as it was becoming increasingly clear that importers were facing a clear shift in consumer spending (from discretionary goods to more essential goods) and a nagging surplus of inventories that were carried over from last year. The reverse bullwhip effect was clearly going to crack any chances of a robust peak season. We also warned that this dismal outlook for future U.S. import demand may drive carriers to go to extreme lengths to keep upward pressure on spot rates.

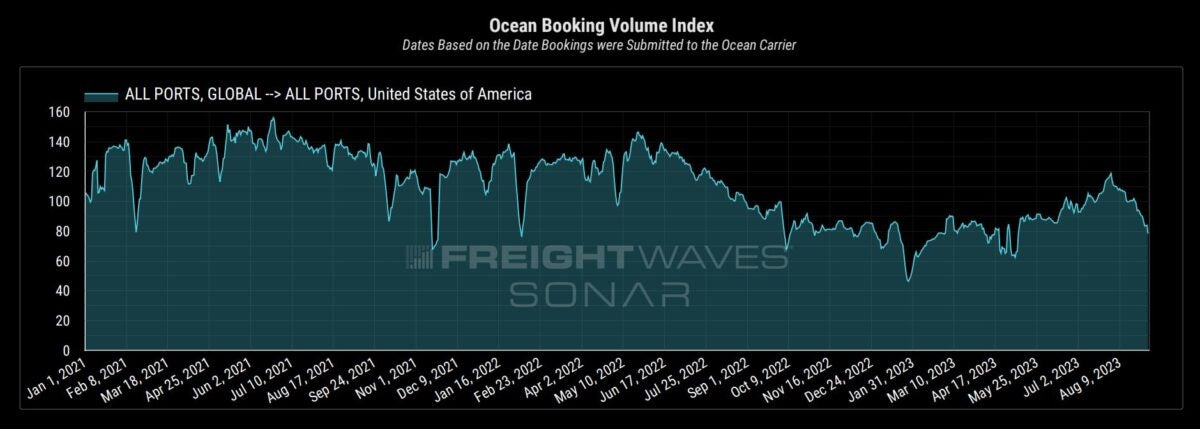

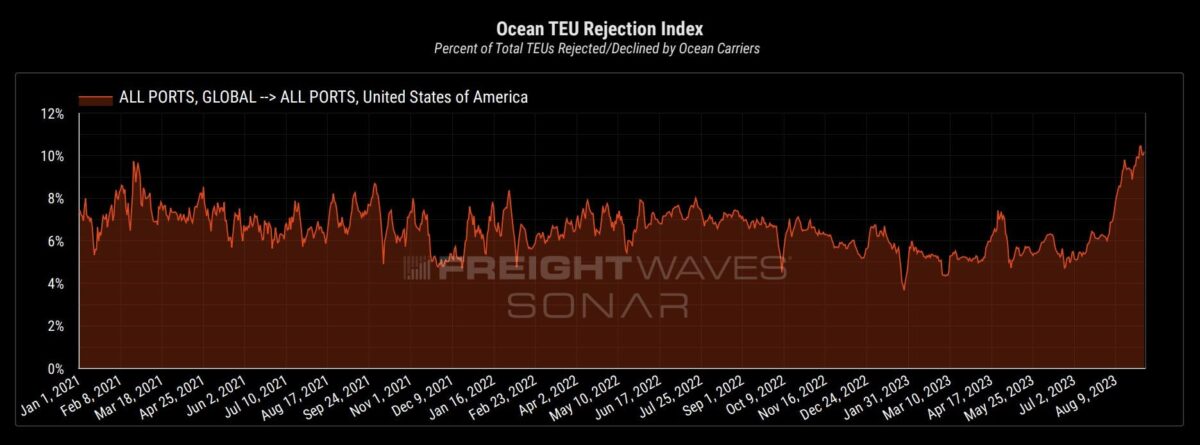

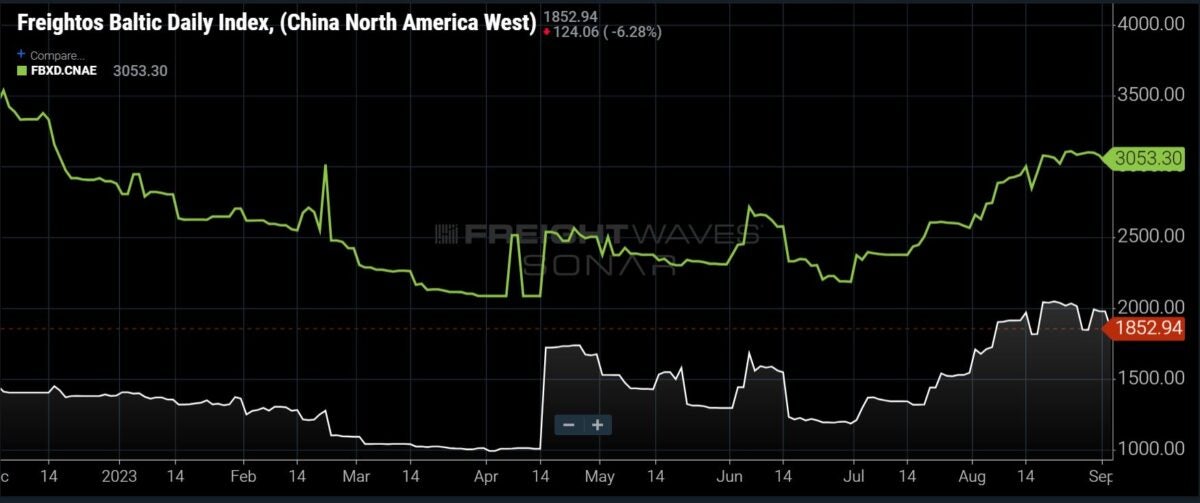

Fast-forward to today and the tide is indeed turning quickly, with recent data from SONAR’s Container Atlas showing new booking volumes plummeting over 35% from their peak reached on Aug. 1, a key indicator that U.S. import demand is rapidly deteriorating. While this significant drop in future demand is undoubtedly increasing the downward pressure on spot rates, ocean carriers have been pulling out all of the stops to help offset this downward pressure. This means going beyond blank sailings and rejecting a record amount of U.S.-bound containers in a seemingly desperate, last-ditch attempt to bolster spot rates ahead of (and after) their proposed general rate increase last Friday.

Whether the container market will continue paying higher spot rates at the beginning of this month is difficult to predict but thus far, it appears as if this unprecedented surge in rejections (and rolled cargoes) has been (at least somewhat) successful in altering the market’s perception/sentiment surrounding the imbalance between supply and demand, which has ultimately led to shippers and brokers paying higher spot rates.

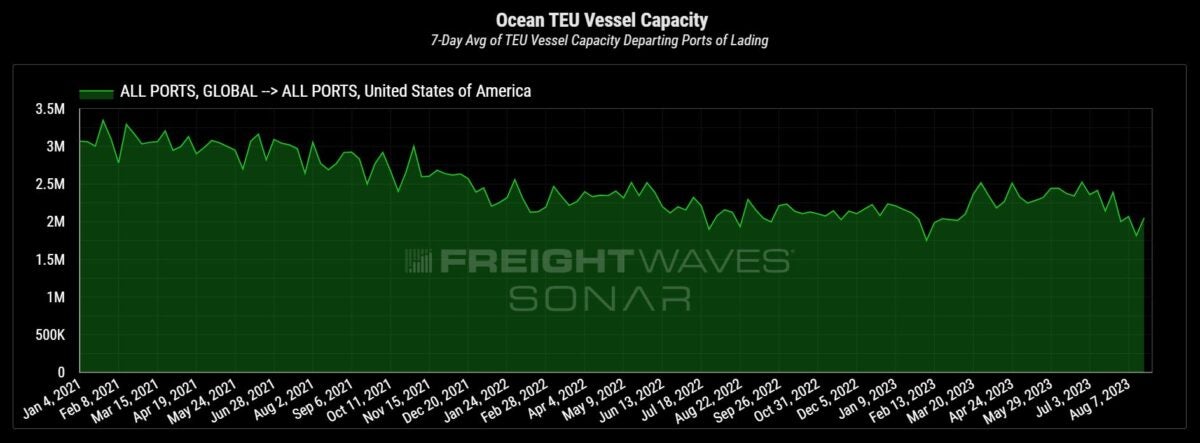

Ocean carriers utilizing blank sailings as a means to control available capacity (chart above) and help offset periods of weaker demand has been a known (and expected) tactic deployed by carriers for well over a decade and is one the ocean container market has (mostly) come to terms with. In a weak peak season, blank sailings are to be expected, but it is the recent spike in ocean TEU rejections (and rolled cargo) that has raised eyebrows over the last few weeks. Seeing these numbers climb during this part of the year that’s historically been (and continues to be) recognized as the tail end of peak season is not just unusual but worth greater scrutiny.

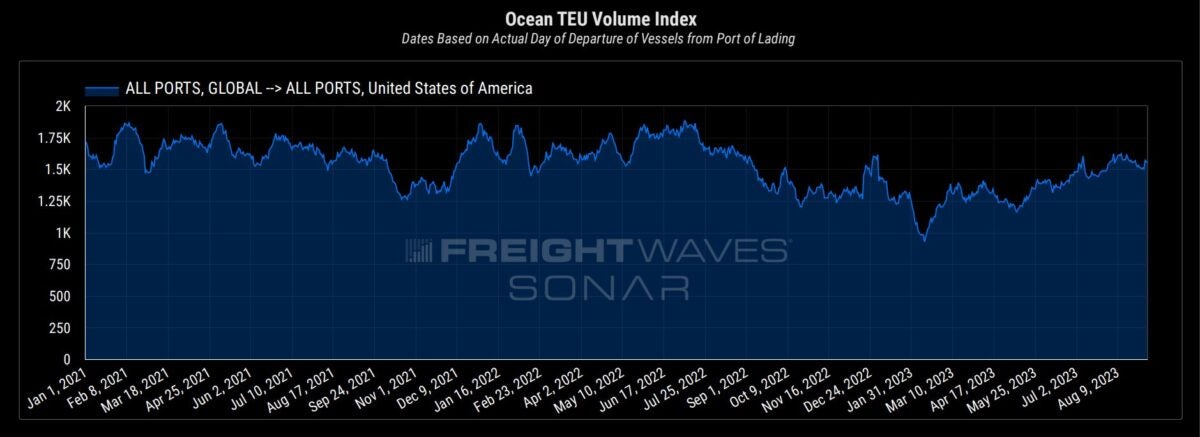

By increasing their use of rejections (and rolled cargo), carriers are able to actively slow down the velocity of containers departing from their respective origins. This has created a bottleneck to the flow of cargo from origin that has led to a higher for longer period of departing volumes (in the chart below), which has accentuated the market’s perception/sentiment that capacity must be tightening further from peak season volumes and, thus, increasing carriers’ utilization rates.

For BCOs, NVOCCs and freight forwarders actually booking containers, this paradox is baffling. Many within these various organizations are likely left asking questions like: How can spot rates continue to rise amid a backdrop of dwindling demand for U.S. imports? Are carriers artificially creating the perception of tightening capacity while simply in search of higher-paying spot rates instead of lower-paying cargoes on long-term contracts? If so, the intent is clear: Drive up spot rates and justify rate hikes in an attempt to bolster spot rates and earn as much higher-paying spot cargo as possible before market sentiment shifts and it becomes increasingly clear that demand is in clear decline.

Either way, it is also important to remember that in order for U.S. importers to cater to the holiday retail season, goods need to make their journey before early September (reaching their destinations before October). These importers are well aware of these lead-time constraints and are very much in tune with the fact that post-peak-season demand should be weakening moving forward, therefore making it much more difficult for carriers to continue using a surge in rejections to alter market sentiment and achieve any further spot rate increases.

The lack of transparency in the ocean market during these types of uncertain and/or volatile times provides these parties with little to no leverage in rate negotiations and can easily cause these same parties to simply pay higher rates to ensure they are provided the vessel spaces they need to meet their respective arrival dates and shipment deadlines here in the U.S. The volatility and disruption many experienced over the last few years only helps to exacerbate any sentiment and perception regarding current market conditions — and has likely helped spot rates move much higher than demand levels have warranted since early April.

This reality causes the recent surge in rejections to seem more like a desperate gambit by carriers to milk high spot rates before the winds change. When spot rates inevitably dip below contract rates, a challenging era awaits for carriers, when they’ll strive to lock the same customers (which are currently getting their cargo rejected and/or rolled) into long-term rates, but that is likely to prove ever more difficult if future declines in demand increase the downward pressure on spot rates.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now