C.H. Robinson chief sees no truckload pivot until second half of 2024

The president and CEO of brokerage and third-party logistics provider C.H. Robinson Worldwide Inc. said he doesn’t see any meaningful pivot in the fortunes of the North American trucking market before the second half of 2024, noting that customer caution about ordering and still-bloated wholesaler inventory levels will mute activity through the first six months of the year.

In an interview with FreightWaves this week, David Bozeman said that in his first six months at the helm of Robinson (NASDAQ: CHRW) he has been struck by the “continued degradation” of the current downcycle, especially in truckload. The amount of oversupply of truck capacity this late in the cycle has not been what he expected.

Customers of the Eden Prairie, Minnesota-based company remain cautious about demand and inventory replenishment. Though much of the retailer destocking is behind the industry, red stocking efforts have yet to begin in earnest, Bozeman said. At the same time, wholesalers are more top heavy with product than he would like them to be.

Spot, or noncontract, truckload rates continue to bump along the bottom, curbed by the unfavorable supply-demand climate for providers, Bozeman said, noting that Robinson is in a strong financial position, though a “lot of our competitors remain in survival mode.”

In theory, the struggling brokerage market might be ripe for the M&A picking for a big player like Robinson. However, Bozeman said M&A is not a top priority and noted that acquisitions and subsequent integrations can be heavy drains on time, financial and human resources.

Well before Bozeman’s arrival at the end of June, there was talk that Robinson might be looking to sell its global forwarding operation, which could command premium prices in the wake of the post-pandemic period. As markets and prices cooled, however, the unit began to struggle and the notion of commanding a high sale price evaporated.

Bozeman said he “feels good” about Global Forwarding’s competitive position, noting that it is deeply involved in the big-ticket global trade lanes. He added, however, that if a prospective buyer offered to write a massive check for the unit, he would be obligated to have a conversation.

Bozeman said he will push to develop synergies between North American Surface Transportation (NAST) and Global Forwarding, Robinson’s two largest units, to drive integrated solutions and value propositions for customers. He is also targeting a 15% improvement in productivity metrics for 2024. Without elaborating, Bozeman said he felt “pretty good” about Robinson’s portfolio of tech solutions.

Bozeman is far from the only executive to wax downbeat about the truckload sector in the near term. The consensus among a recent gathering of representatives of privately held companies sponsored by investment firm Cowen & Co. was that truckload market weakness has persisted through the fourth quarter and would likely continue into the first quarter.

The over-the-road market continues to be “a mess,” one participant was quoted as saying in a note published by transportation analyst Jason H. Seidl, with rates looking similar to what pricing was in the trucking market 20 years ago.

Freight conditions worsened after Thanksgiving following a very modest seasonal uplift through November,” according to the consensus at the gathering. Digital brokers continue to bid down freight, and one participant said that freight capacity and pricing will be influenced by the fate of these brokers, many of which are facing tough times. One of the panelists — identified as a transportation attorney — said there will be many more bankruptcies to come in 2024.

Nuclear verdict alert: More than $16M awarded in Georgia court

If the definition of a nuclear verdict in trucking is more than $10 million, there is a new entry on the list of court actions topping that amount.

A jury in DeKalb County State Court in Georgia awarded Avnish Dalal $16.6 million on Dec. 14 in a case filed against Brown Trucking.

Romi Jayswal of the firm of Deochand & Jayswal told FreightWaves the move to a jury trial came after a “disputed liability, where the offer from the trucking company was about $2 million.” Jayswal said the $2 million offer was not received until the trial was about to begin.

He said Dalal was 21 at the time of the accident in August 2021. It left him with physical injuries and limited mobility even after “several” surgeries. Dalal also suffered a traumatic brain injury “which has affected his life,” Jayswal said.

“I think the insurers and the trucking company pretty much took a stance where they saw basically no fault on the part of their own truck driver,” Jayswal said. “They took the stance that they did nothing wrong, which is why it ended up at trial.”

Reporting by the Courtroom View Network (CVN) from the courtroom trial site in Decatur, Georgia, said jurors assigned 60% liability to Brown and 40% to Dalal.

The CVN reporting described the incident as beginning with truck driver Ebans Tshongwe of Brown stopping his truck on I-285 to avoid a van that was moving through Tshongwe’s lane. Dalal was riding behind the truck. He said he swerved to avoid the Brown truck but did collide with it, hit another truck and then went under the Brown truck.

Reporting on the closing statement from Brown’s lawyer, John Dixon, the CVN article said Dixon presented video and data evidence “that he said showed Tshongwe acted appropriately under the circumstances to avoid striking the van.”

Dixon did not respond to an email sent by FreightWaves.

“Dixon added that Tshongwe did not have time to safely evaluate other potential alternative maneuvers as the van passed through his lane,” according to the CVN article. “Meanwhile, Dixon argued, Dalal was following trailing traffic too closely.”

The counterargument presented by attorneys from the firm of Fried Goldberg, according to the CVN reporting, was that “Tshongwe broke industry standards in failing to apply his brakes as soon as the truck’s acoustic warning system indicated the van passing into his lane. And Goldberg added Tshongwe compounded that error by failing to accelerate once the van left the lane.” Fried Goldberg represented Dalal along with Deochand & Jayswal.

Andy Marquis, a partner with the trucking-focused Scopelitis law firm, said while the $10 million number is an accepted definition of a nuclear verdict, the reality is “$15 million doesn’t even bat an eye too much.”

A more important guideline, Marquis said, is the relationship between the medical costs of a plaintiff in a trucking accident and the legal payout. A payout of $1 million in a case with medical costs that might top out at $10,000 would be a nuclear verdict to Marquis’ way of thinking.

And while the immediate medical costs with Dalal were estimated to be about $900,000, Marquis said the fact that there are brain injuries to a 21-year-old does portend a lifetime of significant medical expenses. “I’m not even sure that anybody would try real hard to say, ‘Gosh, that’s excessive,’” Marquis said.

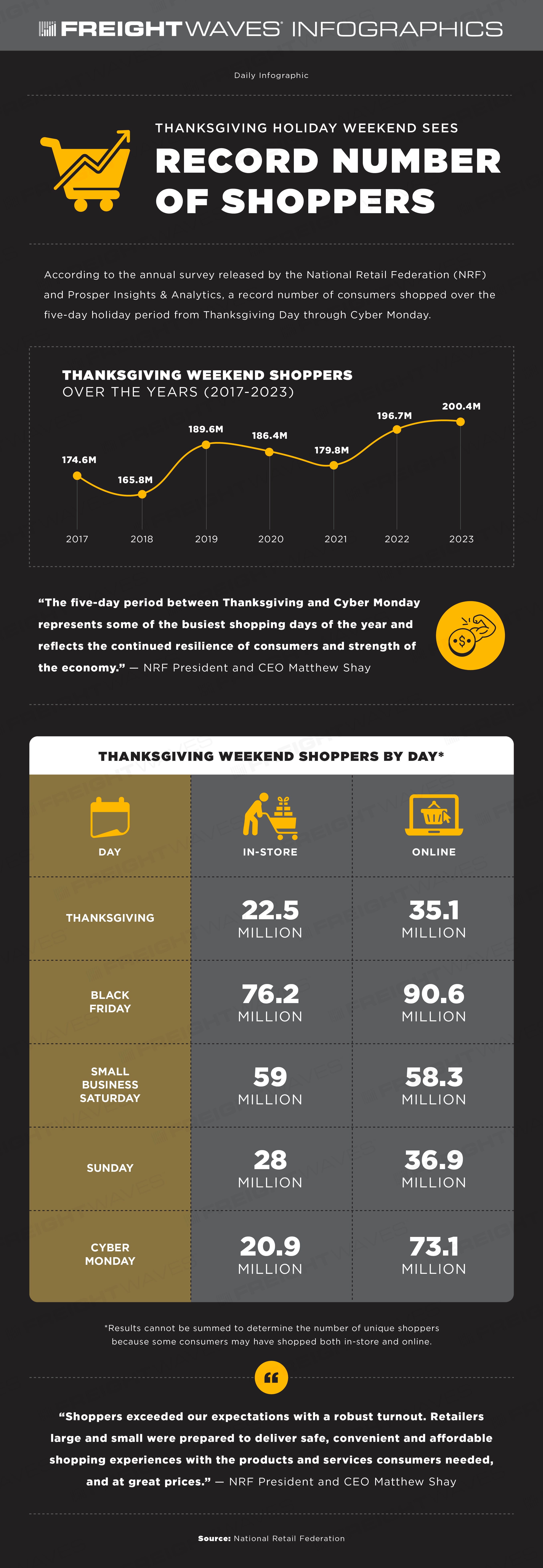

Daily Infographic: Thanksgiving holiday weekend sees record number of shoppers

To view more FreightWaves infographics, click here

Derailment, safety, partnerships among rail’s big issues in 2023

2023 seemed to kick off quietly for U.S. freight railroads: The industry had seen the resolution of the labor contract impasse between craft unions and U.S. Class I railroads in December 2022, while rail service was steadily improving after some struggles earlier in the year.

However, the February derailment of a Norfolk Southern train in East Palestine, Ohio, brought an unanticipated and sometimes harsh spotlight on rail safety, with congressional lawmakers and other public officials scrutinizing the industry’s safety record and calling for reforms to bolster safety standards.

Other unanticipated events, such as partnerships that arose in the intermodal space following the finalization of the merger between Canadian Pacific and Kansas City Southern, also played out throughout the year.

Here are some of the key events and happenings in the freight rail industry in 2023:

Government, general public raise concerns about rail safety

About 20 cars involved in the Feb. 3 NS train derailment contained hazardous materials. Several days following the derailment, public officials and NS decided to vent five tank cars containing vinyl chloride out of concern that the cars could explode because of chemical reactions happening inside them.

That decision, which resulted in a large plume of smoke over the incident site, rattled the community and raised questions about the handling of hazardous materials at the site. While the Environmental Protection Agency has been monitoring the site and NS (NYSE: NSC) has pledged to invest in the community and in safety measures on its rail network, the derailment pointed a spotlight on rail safety, prompting mainstream news outlets to question how their communities would handle a similar situation.

As a result of the derailment — which is still being investigated by the National Transportation Safety Board — the U.S. Department of Transportation and the Federal Railroad Administration recommended a number of safety measures or issued advisories related to how rail operations might have been handled in East Palestine. Members of Congress, including the Senate delegations for Ohio and Pennsylvania, drafted a rail safety bill. That bill is still awaiting action although it passed the Senate commerce committee in May. The rail industry and industry stakeholders also addressed ways they are seeking to bolster rail safety.

Unions and rail carriers reach sick leave agreements but other union concerns remain

The labor contracts agreed upon in December 2022 — under the supervision of Congress and President Joe Biden — involved more than 30 railroads and 12 rail unions, according to the National Railway Labor Conference, the group representing the Class I railroads at the bargaining table.

While the final agreement addressed general wage increases and medical leave, it did not address sick leave, which was a sticking point for the unions. That exclusion caused the unions to threaten to strike, but Congress and the White House intervened. A three-person advisory board appointed by Biden had also earlier in the year recommended that sick leave agreements be arranged at the local level.

As a result, 2023 saw a number of sick leave agreements between individual unions and rail carriers. A few agreements also dealt with work schedules.

However, other issues that the unions keep track of are ongoing. Those include whether federal regulators will require freight train crews to have at least two people operating a train and whether FRA and the freight railroads can agree on terms that would establish a federally supported anonymous tip line to report safety concerns.

The downturn in rail volumes also brought into question whether the railroads would consider furloughs, with Union Pacific (NYSE: UNP) deciding to furlough some workers in the second half of 2023. The industry had used furloughs historically to address seasonally related changes in maintenance or to cut costs when volumes are lower.

The Surface Transportation Board appeared to get closer to reaching a decision on reciprocal switching.

Reciprocal switching is a process that grants a shipper access to the network of a second Class I railroad at an interchange, with the idea that the shipment would continue on the network of the competing Class I railroad because of lackluster service on the originating Class I railroad.

The board first heard the calls to allow reciprocal switching in the U.S. more than a decade ago when the National Industrial Transportation League brought the issue before the board in July 2012.

In September, STB had issued a notice of proposed rulemaking calling for reciprocal switching as a remedy that shippers could use to address deteriorating rail service. A comment period followed and was extended. While some shippers appreciated that there was movement on the issue, they also wished the proposed rule had addressed more thoroughly plans to increase rail competition, particularly for shippers with limited options.

A final rule could come out in 2024.

The board’s actions on reciprocal switching reflect what stakeholders see as one of the most active boards in years. The heightened activity — much of it coming from concerns over subpar rail service in 2022 — was due in part to the leadership of STB Chairman Marty Oberman. But Oberman surprised rail observers this fall, saying that he would not seek another term as board member. Stakeholders will be watching not only who will replace Oberman as chairman but also who will be nominated to fill his spot on the board.

CARB sees future in zero-emissions locomotive configurations

In late April, the California Air Resources Board issued new rules, effective in various stages starting in 2030, that would require zero-emissions locomotive configurations for trains operating in the state in place of diesel locomotives.

The new rules, which CARB says are aimed at reducing the emissions of locomotives operating within California, have two notable deadlines: Switch, industrial and passenger locomotives built in 2030 or after will be required to operate in zero-emissions configurations, while locomotives built in 2035 for freight linehaul operations will need to comply with the zero-emissions configurations.

The new rules also limit locomotive idling to 30 minutes except for certain circumstances, such as maintaining air brake pressure or providing heat or cooling to the locomotive cab, and they require locomotives operating in California to register with CARB and annually report on their activity, emission levels and idling data. These two conditions would go into effect in 2024.

Following CARB’s issuance of the rules, the Association of American Railroads and the American Short Line and Regional Railroad Association sued the agency, saying it is asking the rail industry to use technology that has neither been sufficiently tested in prototype and is not commercially available in today’s market. Short-line railroads have argued that modifying existing locomotives or purchasing new ones could be cost-prohibitive for companies. That suit is in the federal courts.

After years in the making, the merger between Canadian Pacific and Kansas City Southern was finalized in April, with the company now calling itself Canadian Pacific Kansas City, or CPKC. CPKC touted itself as having single-line service that spans Canada coast to coast, traverses the U.S. Midwest and reaches several points in Mexico, including the Port of Lázaro Cárdenas on Mexico’s Pacific coast.

While CPKC launched daily intermodal service shortly thereafter, other Class I railroads also appeared to start making plans to increase volumes among the U.S., Mexico and Canada.

Indeed, all the Class I railroads seemed to have new intermodal offerings. Canadian rival CN (NYSE: CNI) announced a Falcon Premium service with UP and Mexico’s Ferromex, and it unveiled a domestic intermodal service with NS in September. Meanwhile, BNSF (NYSE: BRK-B) and J.B. Hunt (NASDAQ: JBHT) unveiled plans for a new customized intermodal offering, and those two companies plus Mexico’s GMXT also announced intentions to develop a Mexico-to-Midwest intermodal service. And CSX (NASDAQ: CSX) and CPKC are seeking to establish a new rail corridor between the U.S. Southeast and Mexico.

These new partnerships even appear to be ushering in a new period of consolidation between the railroads themselves and the railroads and other transportation carriers, industry leaders remarked in November.

A second lot of Yellow’s terminals have found new homes, according to a Wednesday filing in a Delaware bankruptcy court. The latest auction for a portion of the defunct less-than-truckload carrier’s leased properties raked in $83 million across 23 locations.

The first wave, which included 130 terminals — only two of which were leased — fetched nearly $1.9 billion.

Carriers that participated in the first auction again hold winning bids.

The recent auction, which included winning bids from just six LTL carriers, occurred Monday and Tuesday. Estes holds the largest bid at $35.3 million for five properties. The carrier previously locked up 24 terminals valued at $248.7 million.

RAMAR Land Corp. (R+L Carriers) landed three terminals valued at $9 million. The carrier took home $211.5 million in real estate in the first auction.

Saia (NASDAQ: SAIA) has a winning bid for 11 sites at $7.9 million across several Western states with a concentration in Montana, South Dakota and Wyoming. It won 17 terminals for $235.7 million earlier this month.

Other bidders included ArcBest (NASDAQ: ARCB) with one property in Bethlehem, Pennsylvania, at a value of $7.8 million and Knight-Swift (NYSE: KNX), which got two properties at a little more than $400,000 in Montana and Washington.

FedEx Freight (NYSE: FDX), which wasn’t active in the prior auction, walked away with a winning bid of $22.5 million for one terminal outside of Reno, Nevada.

Bidder

Terminal count

Purchase price

Estes

5

$35.3M

FedEx Freight

1

$22.5M

RAMAR Land Corp. (R+L Carriers)

3

$9.0M

Saia

11

$7.9M

ArcBest

1

$7.8M

Knight-Swift

2

$417,150

Table: U.S. Bankruptcy Court — District of Delaware filing

The sale of Yellow’s leased properties also requires the new tenants to pay costs to cure the current leases as Yellow was delinquent in rent payments and had failed to make required repairs in many locations.

“Winning bids for certain properties include additional payments for cure costs in addition to the cash purchase price noted herein,” the filing read.

There are still 118 leased properties remaining to be sold as well as another 46 terminals that the company owns.

A hearing to approve the sale of the leased properties is scheduled for Jan. 12. Objections to the sales or assurance of future performance are due to the court by Jan. 5.

XPO’s (NYSE: XPO) $870 million bid for 28 properties was the largest winning bid in the first auction. The carrier recently said that it will make repairs and rebrand the terminals prior to reopening them, which will occur throughout 2024 and into 2025. It closed on the acquisition of the properties on Wednesday.

The relaunch of Yellow’s terminals may not upset the current supply-demand balance in the market.

Some of the recently acquired sites represent upgrades to better or bigger locations for carriers and are not full incremental capacity additions. Also, many of the service centers are now in the hands of more price-disciplined carriers versus Yellow, which was known as a low-cost provider. Lastly, some of the future sales will likely include buyers that will repurpose the terminals for use outside of LTL operations.

The court recently approved the sale of Yellow’s 12,000 tractors and 35,000 trailers through auction houses. That liquidation remains ongoing.

In April 2023, the Amelia Earhart Hangar Museum opened in Atchison, Kansas, and according to Executive Director Mindi Love Pendergraft, it is so popular with visitors — who often come from across the country — that it is in the running for USA Today’s Best New Museum.

Since this is a people’s choice award, the public is invited to vote.

“I think the editors recognized we are the first and only museum dedicated to the aviation legacy of Amelia Earhart, one of the world’s most admired women,” said Pendergraft. “It may also be that the museum offers a rare blend of state-of-the-art STEM [science, technology, engineering and math] interactives with history storytelling that uniquely takes visitors on a journey through Amelia’s trailblazing life.”

Pendergraft, a native of Kansas, grew up hearing stories about the famous aviatrix. She was at the museum on opening day.

“I was drawn by how the museum tells Amelia’s story in a way that brings her to life beyond the allure of Amelia the ‘icon’ to present a person who boldly faced real challenges and struggles in the pursuit of her dreams — and used her success to inspire others,” she said. “I’m also impressed by how the museum engages visitors, particularly young people, with hands-on STEM concepts as they journey through Amelia’s life. The museum is responding to an urgent need to help young people consider careers in aviation, aerospace and other STEM-related career paths of the future.”

The museum includes hands-on STEM activities for young people. (Photo: Amelia Earhart Hangar Museum)

The centerpiece of the facility is the world’s last remaining Lockheed Electra 10-E, named Muriel after Earhart’s younger sister. The airplane is identical to the aircraft Earhart used on her final flight in her attempt to fly around the world. Earhart’s aircraft disappeared over the Pacific on July 2, 1937. She was attempting to reach Howland Island to meet up with the Coast Guard cutter Itasca. There was sporadic radio contact, with Earhart indicating she was lost and running low on fuel, then radio silence.

The U.S. Navy spent weeks searching for Earhart and her navigator, Frederick Noonan, but no trace was found. To this day, the search was the largest effort of its kind by the Navy with the exception of the search for the wreckage of the space shuttle Challenger in 1986.

Beyond the aviatrix

Earhart was more than a pilot — she was a trendsetter and role model for women, advocating for them to pursue higher education and careers. She had a keen interest in the sciences and used her celebrity status to advocate for social causes. She was close friends with first lady Eleanor Roosevelt, even persuading her to skip out on a state dinner — despite the fact they were dressed in formal gowns — to go flying.

“Many of her accomplishments were underrated,” said Pendergraft. “I’m a native Kansan who grew up knowing about Amelia, but until I joined the Museum I had no real idea of her many accomplishments and influences beyond the headlines — many of which are underestimated, like working as a mechanic, nurse and student adviser at Purdue to encourage other women.”

Pendergraft said the museum started gaining attention before it even opened. In January, Smithsonian Magazine named the museum one of the Top 10 Most Anticipated Openings in 2023, and in the fall the museum was profiled by the Midwest Travel Journalists Association with its annual GEMmy Award as one of the “gems of travel” as it “offers an exceptional experience to travelers.”

A few weeks ago, museum officials were notified by the editors of USA Today’s 10Best readers’ choice awards that theirs was one of 16 museums in the country to be nominated.

“We didn’t know about the contest and were beyond thrilled to be nominated,” Pendergraft said. “We’ve since learned that 10Best nominees are submitted by a panel of travel experts, and then the 10Best editors narrow the field to select the final set of nominees for the public to vote on.”

Voting is done online and readers can cast a ballot once per category, per day, until the cutoff of noon next Monday.

“If we reach the No. 1 spot, the museum will be featured in USA Today and recommended across USA Today’s travel and tourism platforms as a top destination in the U.S.,” Pendergraft said. “This special honor will not only shine a bright spotlight on the Amelia Earhart Hangar Museum, but it will also heighten public interest in exploring the many stellar museums and tourism attractions across the Midwest.”

Other museums in the running include the Punk Rock Museum in Las Vegas, Museum of Broadway in New York, Gettysburg Beyond Battle Museum in Pennsylvania, the Buffalo AKG Art Museum in New York, and Cheech Marin Center for Chicano Art & Culture in Riverside, California.

FreightWaves Classics articles look at various aspects of the transportation industry’s history. Subscribe to our newsletter!

Have a topic you want us to cover? Email bjaekel@www.freightwaves.com.

Forward Air sells final-mile unit to Hub Group for $262M

Forward Air announced Wednesday that it sold its final-mile business to Hub Group for $262 million. The deal comes as Forward refocuses its efforts on increasing share in the premium less-than-truckload market.

Forward Air Final Mile (FAFM) has 46 locations and more than 640 employees, which will transfer to Hub Group (NASDAQ: HUBG), a news release said. The unit generated $289 million in revenue for the 12-month period ended Sept. 30., mostly from the delivery and installation of large appliances.

On its third-quarter call, Tom Schmitt, Forward’s chairman, president and CEO, said the company was undertaking a “strategic portfolio review” and potentially selling noncore assets that don’t fully support its LTL growth plans.

“Our Final Mile business grew revenue over 150% since inception in 2019 and returned significant value to Forward’s employees, customers and shareholders,” Schmitt said. “We are pleased the Final Mile team has joined a first-class company and team of people.”

In a separate statement, Hub Group said the acquisition of FAFM will more than double final-mile revenue on its platform. It said the deal was its largest nonasset transaction in company history. It expects FAFM to be immediately accretive to earnings starting next year.

“We are excited to welcome the Forward Final Mile team to Hub Group,” said Phil Yeager, Hub Group president and CEO. “Through this transaction, we will continue to grow our non-asset logistics segment and deepen our value to our customers through the addition of this excellent team and their best-in-class appliance capabilities.”

FAFM’s senior management team was provided contingent compensation targets to “incentivize their retention and drive continued growth,” Hub Group’s release said. FAFM will operate under the Hub Group Final Mile brand.

Shareholders have said the deal is too expensive and adds a significant amount of leverage. They have also voiced concerns with Forward’s growth ambitions outside of its legacy third-party sales channel, which potentially pits it as a competitor to existing customers.

An announced deal price of $3.2 billion (currently closer to $2.6 billion given the sell-off in Forward’s stock) includes the assumption of $1.5 billion of Omni’s debt.

Omni maintains it has met all closing requirements and that Forward is misconstruing a “what-if” scenario as a way for Forward to exit the merger. It has asked the court to force Forward to the closing table.

A hearing on the matter is set for Jan. 19.

Forward’s shareholders are still contesting the transaction in a Tennessee court.

“We believe Hub Group’s middle-mile and final-mile expertise, combined with our unique appliance delivery capabilities, will unlock significant value for our combined customers and through this combination we expect to accelerate our growth versus what we have each done individually in the past,” said Scott Robider, senior vice president at FAFM.

Port of New Orleans nets $73M federal grant for container terminal

The Port of New Orleans has been awarded a $73.77 million federal grant to advance the first construction phase of the $1.8 billion Louisiana International Terminal project.

The container terminal will be capable of handling 2 million twenty-foot equivalent units annually and ultra-large container vessels once completed in 2028.

“With Louisiana’s unmatched inland connections and with no bridges in its way, the new Louisiana International Terminal will meet market demands for much-needed supply chain solutions and bring prosperity to our region for generations to come,” Brandy D. Christian, the port’s president and CEO, said in a news release.

The Louisiana International Terminal will be constructed in the municipality of Violet, about 14 miles down the Mississippi River from the Port of New Orleans. Plans for the terminal include a 350-acre container facility with a 3,500-linear-foot wharf on more than 1,000 acres.

The new container terminal is aimed at eliminating air-draft restrictions that limit the size of vessels that can currently call the Port of New Orleans, officials said.

“This is exactly the type of investment that Louisiana and America need and builds upon our recent efforts to deepen the Mississippi River to handle the largest container vessels in the world,” U.S. Rep. Garret Graves, R-La., said in a statement. “The Louisiana International Terminal takes advantage of a newly deepened Mississippi River and Louisiana’s strong rail, highway, and maritime transportation network to connect our state even more closely to 31 states in the river’s northern watershed and the international market to our south.”

The terminal will be built through a public-private partnership between the Port of New Orleans, New Jersey-based Ports America and Switzerland-based Mediterranean Shipping Co.’s investment arm, Terminal Investment Limited. The partnership has already committed $800 million toward the project.

Louisiana lawmakers have already provided nearly $30 million toward early development costs for the project and $50 million for the design of the St. Bernard Transportation Corridor that will connect the terminal to the interstate system.

The Louisiana International Terminal project will generate about 32,000 jobs, including 4,300 in St. Bernard Parish and 18,000 in Louisiana, as well as more than $1 billion in state and local tax revenue by 2050, according to state officials.

“With this grant, the Port of New Orleans will be able to modernize and grow its operations for this century and ensure that it continues to be the economic driver for the entire region,” U.S. Rep. Troy Carter Sr., D-La., said in a statement.

Red Sea fallout much greater for containers than tankers, bulkers

Tuesday’s announcement of Operation Prosperity Guardian, a joint military operation to protect commercial shipping in the Red Sea, was met with skepticism — and jokes about the Seychelles, a popular island honeymoon destination off the coast of Africa.

The existing naval security operation in the Red Sea, Combined Task Force 153, is a 39-nation partnership. Operation Prosperity Guardian has just 10 partners: the U.S., U.K., Canada, France, Italy, Spain, the Netherlands, Norway, Bahrain and the Seychelles.

As of Wednesday, there were no details available on what Operation Prosperity Guardian will do beyond expanded patrols, or how long it will take for escorted convoys to be put in place, if at all.

“Officials have played down the idea that they will provide naval escorts for commercial vessels,” said ship brokerage Braemar on Tuesday.

According to Evercore ISI shipping analyst Jon Chappell, “The number of ships that transit the Red Sea is large enough that the U.S. is reportedly guiding against the idea that 100% convoy escort is viable.”

However, that could lead to escalating military action in the region, making ship operators even less likely to use the route.

Binary outcome

Current fallout from the Red Sea crisis is focused much more on container shipping than other vessel segments.

Virtually all container vessels are rerouting around the Cape of Good Hope. Container ships that had already transited southbound through the Suez but had yet to reach the Bab-el-Mandeb Strait are now turning back, paying another toll to get to the Mediterranean.

Numerous bulk commodity ships are heading to the Cape, as well, but not to the extent container ships are. That could change with a military escalation, which could increase reroutings across all shipping sectors.

“We see the outcomes as fairly binary here,” said Chappell in a research note on Tuesday. “Either the creation of the task force substantially restores confidence in shippers using the Red Sea/Suez route, or further escalation largely closes the route.

“The former is the dominant base case, but it is worth being attentive to the latter risk case, as the consequences could be macro-significant,” Chappell warned.

He sees the “strong base case” as “we revert to something tolerably close to business as usual.” But he believes the risk of escalation is “non-trivial.”

In a worst-case scenario, in which Red Sea transits for all ship types are heavily curtailed, “we could see freight prices go up multiples — think five to 10 times,” said Chappell.

“These costs would be passed through to the consumers and shippers and supply chain bottlenecks would re-emerge as the greater distances around Africa would tie up extreme amounts of shipping capacity.”

In the unlikely event of a full closure of the Red Sea/Suez route for more than a week, Chappell said it “would start to have global effects.”

Diversions require more container-ship capacity

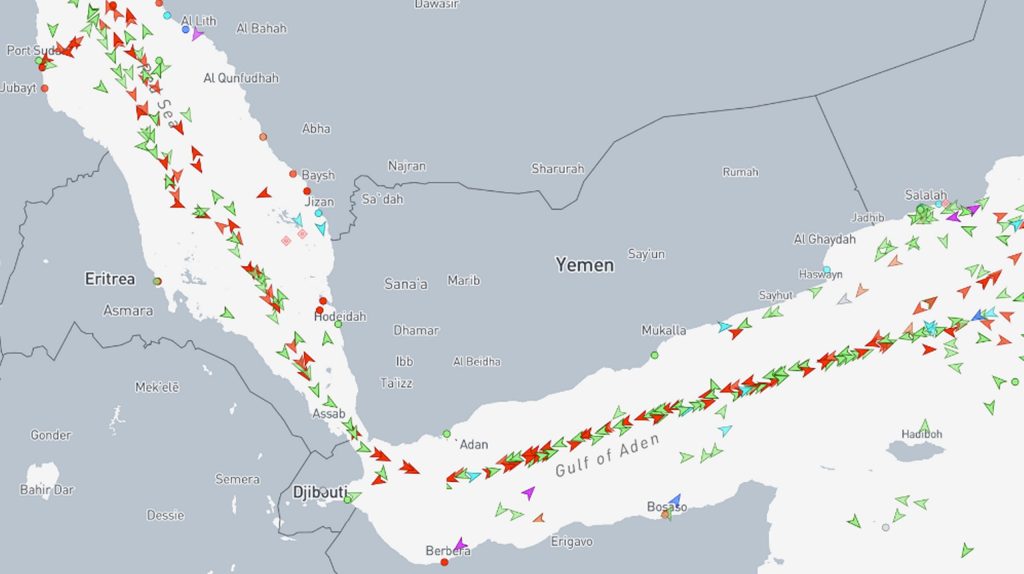

Automatic Identification System (AIS) ship-position data from Kpler-owned MarineTraffic shows how different vessel segments are dealing with the Houthi threat differently.

Larger container lines have rerouted all of their services to the Cape of Good Hope. Ship-position data on Wednesday morning showed no container ships transiting the Bab el-Mandeb Strait.

Longer voyages will ultimately require more container ships to maintain the same service levels. According to Sea-Intelligence, the switch to the around-Africa route will require 1.45 million to 1.7 million twenty-foot units of additional ship capacity.

That, in turn, will help container lines absorb newbuilding capacity that is now being delivered, which should keep container freight rates higher than they would have been minus the Houthi attacks.

Bulkers and tankers continue to transit

In contrast to container shipping, AIS data shows that the Bab-el-Mandeb Strait remained heavily trafficked by dry bulk carriers on Wednesday.

Dry bulk carrier positions as of Wednesday morning. (Map: MarineTraffic)

MarineTraffic ship-position data on tankers — including crude and product tankers as well gas carriers — also showed ongoing traffic through the strait.

Tanker positions as of Wednesday morning. (Map: MarineTraffic)

“Few tankers have thus far been rerouted via South Africa,” reported Braemar. “One or two fixtures via the Suez have failed in recent days, and we know of at least two Suezmaxes [tankers with capacity of 1 million barrels] that have been asked to delay passage through the Suez Canal until the situation settles down.

“We are still fixing cargoes via the Canal without Cape options,” confirmed Braemar. “Most owners we talk to are assessing [transits] on a case-by-case basis, even some of those that have publicly stated that they would not transit the Suez.”

Routing of laden tankers is determined by the ship charterer. Oil companies BP and Equinor have announced that they won’t route their cargoes through the Red Sea, but they are in the minority.

Lars Barstad, CEO of tanker owner Frontline (NYSE: FRO), told S&P Global Commodity Insights: “Shipowners have limited opportunity to reroute when the vessel is already under contract, if safety is deemed acceptable. Disappointingly few oil majors have adopted BP’s and Equinor’s policy.”

Another reason crude tanker flows are not seeing a big effect yet: Much of it is Russian crude, and the Houthis are backed by Russian ally Iran.

According to Ioannis Papadimitrou, senior freight analyst at Vortexa, “Of the approximately 1,200 laden crude voyages that transited the Red Sea in 2023, 60% originated in Russia. Given that Russian barrels are increasingly being carried by non-EU/Western operators, these flows face minimal risk amid the ongoing Houthi attacks.

“Additionally, these barrels are heading to non-EU/Western buyers, which further decreases the likelihood of disruption for these flows.”

Rates up for tankers transiting Red Sea

On the plus side for tanker markets, rates are rising for vessels that do take the Red Sea route.

According to Braemar, “While the attacks have failed to influence the broader tanker market, for vessels looking to transit the Suez Canal, the conversation — and the cost — has changed dramatically over the past few days. Suezmax charterers looking to fix Med-to-Far East via the Suez are looking at a jump of $850,000.”

Brokerage Fearnleys said Wednesday that Suezmax rates from the Middle East Gulf to Europe transiting the Red Sea “have firmed significantly … which is no surprise given developments there.”

Effect on shipping stocks

The container-centric effect of the Red Sea crisis is being reflected in near-term stock pricing.

Shares of container lines — particularly Israeli carrier Zim (NYSE: ZIM) — are rising faster than shares of owners of Suezmax crude tankers and product tankers.

Between Dec. 12 and mid-day Wednesday, shares of Zim were up 42%, albeit off highly depressed levels.

In contrast, shares of product-tanker owners Scorpio Tankers (NYSE: STNG), Torm (NASDAQ: TRMD) and Ardmore Shipping (NYSE: ASC) were up 16%, 15% and 11%, respectively, over the same period.

Shares of Suezmax owners Nordic American Tankers (NYSE: NAT) and Teekay Tankers (NYSE: TNK) were up 15% and 12%, respectively, since Dec. 12. Stock prices of mixed-fleet owners Frontline and International Seaways (NYSE: INSW) were up 11% and 10%, respectively.

Nikola cuts 10-year hydrogen deal with FirstElement Fuel

Nikola Corp. has entered a 10-year partnership with FirstElement Fuel to provide hydrogen for its push to sell fuel cell electric trucks in California.

FirstElement Fuel (FEF) is the leading hydrogen station operator in the Golden State. It is relatively new to heavy-duty truck refueling. It operates a fast-refueling station in Oakland. Thirty Hyundai Xcient fuel cell trucks participate in a pilot program at the Port of Oakland. The station received funding from the California Energy Commission under the NorCal Zero Project.

Fast-fill lanes for hydrogen-powered trucks

FEF expects to serve 200 hydrogen-powered trucks at an H70 fast-fill lane. Nikola fuel cell trucks could help soak up some of FEF hydrogen once it reaches scale production of the Nikola Tre in Coolidge, Arizona.

“FirstElement Fuel is a recognized leader in hydrogen vehicle fueling in California, and the Nikola team is inspired by the immense possibilities created by this agreement,” Nikola President of Energy Joe Cappello said in a news release.

FEF plans additional stations for truck refueling, which “signifies a powerful synergy between Nikola and FEF,” he said.

Joel Ewanick, FEF founder and executive chairman, said, “We are confident the synergy between our shared expertise and vision will help to reshape the landscape of clean and sustainable transportation, driving towards a future powered by hydrogen.”

Multiple paths

Nikola plans several paths to a network of up to 60 stations by 2026. That includes mobile and permanent stations under the HYLA brand. HYLA stations would be open to all makes of fuel cell trucks. Two locations — the FEF station in Oakland and a station in Ontario in California’s Inland Empire — expect to be online by the end of 2023. Nikola plans for several more by mid-2024.

Nikola’s broader strategy involves working with industry-leading partners to ensure a robust hydrogen supply chain, transport logistics, storage solutions and dispensing locations. The company has said it has enough energy offtake to support customer operations through the early months of 2024.

The company plans a series of HYLA hydrogen fueling locations throughout Southern California. Northern California follows to support the recent launch of the Nikola hydrogen fuel cell electric truck.