Chart of the Week: Ultra-low Sulphur Diesel Rack Price, Diesel Truck Stop Retail Price, Retail – Rack Fuel Price Spread – USA SONAR: ULSDR.USA, DTS.USA, FUELS.USA

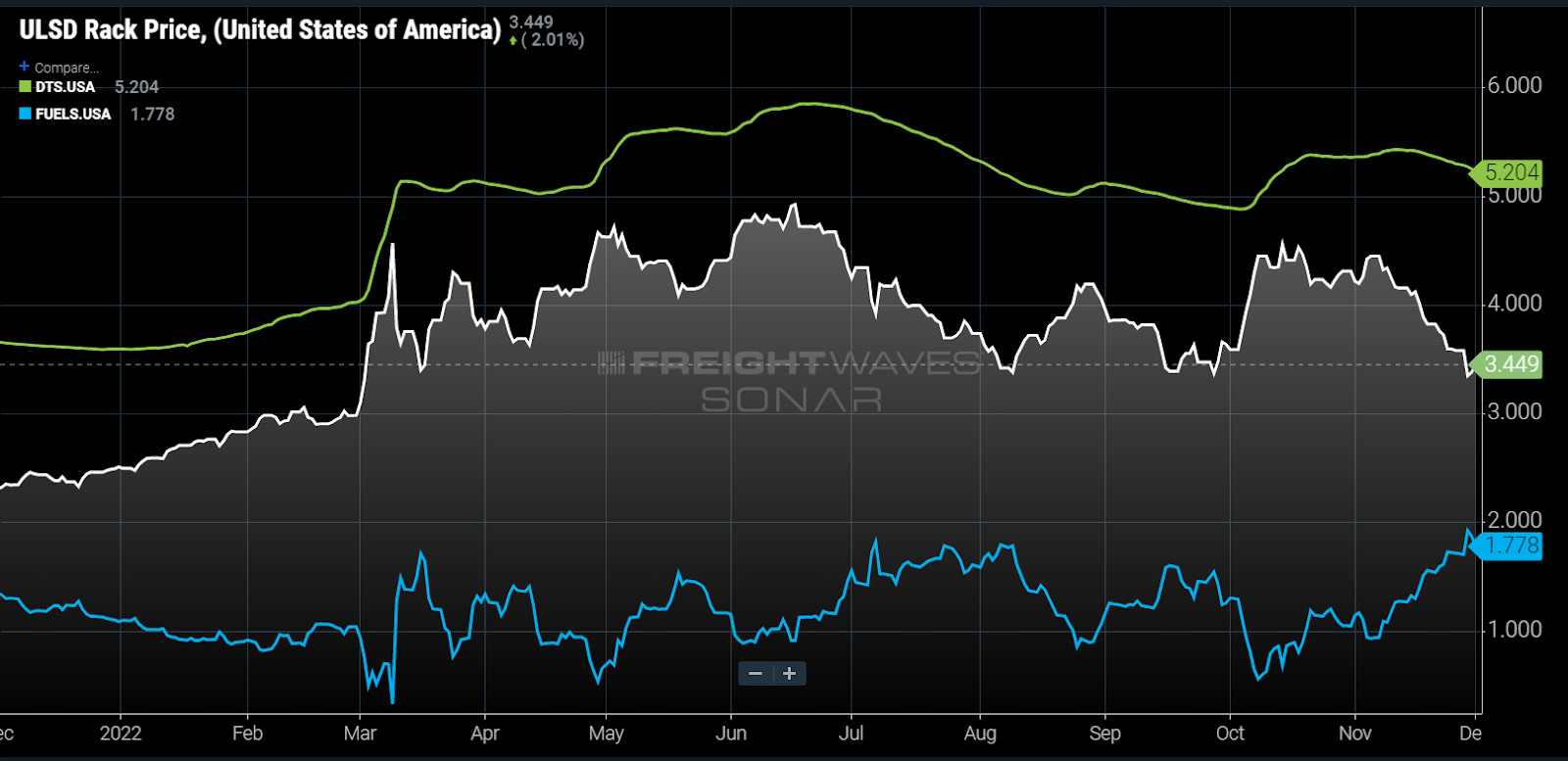

The national spread (FUELS) between the retail (DTS) and wholesale (ULSDR) price of diesel hit a multiyear high this past week as retail prices continue to lag the volatile wholesale market. The slow responsiveness of retail to wholesale price drops is a huge disadvantage to smaller operators that do not have the purchasing power to buy off the rack.

Since the Russian invasion of Ukraine, fuel prices have moved chaotically due to speculation over potential supply shortages. As unbelievable as it may seem, the retail price that most people see at the pump is much more stable than the wholesale or rack price that many retail gas stations purchase.

The variation between these two figures has become increasingly important to the trucking industry. The larger the spread, the bigger the advantage the large fleets with purchasing power have over smaller operators.

Spot-heavy operators are more exposed to fuel volatility

Smaller operators that rely on spot market demand felt the brunt of this past year’s collapse in freight volumes. Demand for domestic truckload capacity fell dramatically this spring.

Shipper requests for truckload capacity under an established rate agreement or tender volumes, as measured by the Outbound Tender Volume Index (OTVI), fell about 17% from Valentine’s Day to mid-May. Spot rates, represented by the National Truckload Index (NTI), fell 16% over the same time — putting an end to nearly 19 months of increasing spot rates.

Demand erosion and collapsing spot rates are not the whole story. During this same stretch, fuel prices jumped over 40% on the retail market. The NTI measures spot prices inclusive of fuel, meaning carrier margins were squeezed much faster than the rate drop implies due to the increasing cost of operating.

Larger carriers tend to rely more heavily on contracted freight, which is handled much differently than spot or transactional freight. The rates are typically set annually (not daily) and the volumes are relatively consistent (not sporadic).

The fuel cost is managed through a variable surcharge based on the DOE’s weekly retail diesel price release. In other words, contract freight was protected from the sharp rise in fuel cost from a carrier perspective.

Slow to respond

The spread between the retail and rack diesel price averaged $1.01 per gallon from February 2018 to March of this year, with a standard deviation (a measure of variance) of 17 cents a gallon. Since March 1, the average spread value has been $1.23, with a standard deviation of 31 cents a gallon. The fuel spread hit $1.93 last week. This is the largest spread since the index was created in 2018. The takeaway here is that fuel price volatility has favored large buyers of wholesale diesel since March.

One of the main drivers of elevated fuel spreads has been the slow responsiveness of the retail price to fall after the rack price drops. Fuel price volatility means the retailers have to be more nimble in their purchasing approach, but also seems to make them more hesitant to drop the price.

Since Nov. 7, the rack price has dropped $1.16 per gallon while the retail price has only fallen 23 cents a gallon. This is a huge cost advantage to carriers with buying power and that are contract heavy. Fuel surcharges are able to be passed along based on the higher retail number in this circumstance. The higher the spread, the larger the potential advantage for carriers that can purchase off the rack.

It should be noted that this mechanism does not always work in the carrier’s favor. In early October, the rack price shot up 23% in a five-day period, exposing carriers to a sharp drop in the fuel spread — hitting 56 cents a gallon on Oct. 8. Surcharges would have been based on a relatively low retail figure at that point.

For now, the conditions favor the larger operators that have the infrastructure to manage a volatile fuel environment. While declining demand has already hit many carriers hard, the inflationary pressures may only accelerate a consolidation of capacity where small operators get acquired or absorbed into larger fleets. This would once again set the table for the next cyclical turn for trucking as competition is removed.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now