J.B. Hunt Transport Services declined to offer a formal outlook for 2026 during an investment conference this week. However, the multimodal transportation provider emphasized its commitment to control the controllable in the coming year as it remains hopeful that conditions will finally improve after the calendar flips.

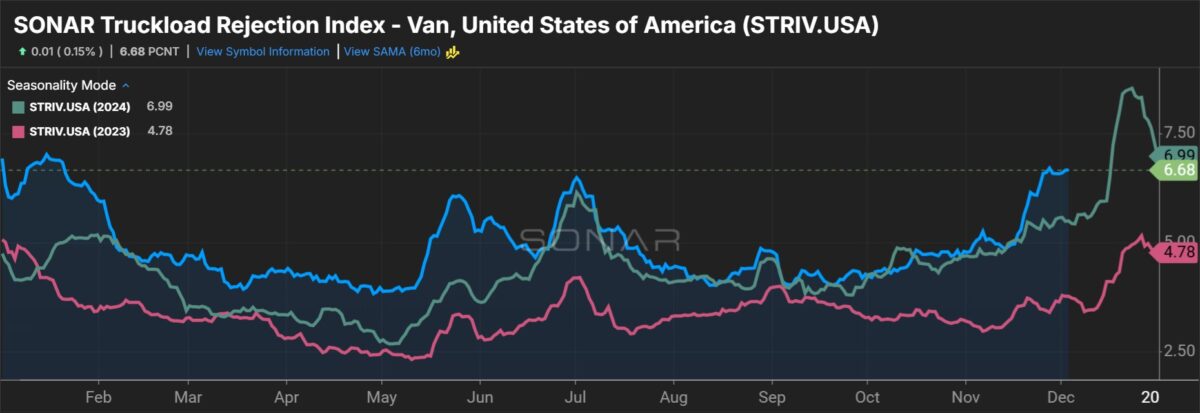

While acknowledging that overall freight demand remains soft, management from J.B. Hunt (NASDAQ: JBHT) pointed to some green shoots and peak-like conditions across its five service offerings at the UBS Global Industrials & Transportation Conference in Palm Beach, Florida on Tuesday.

“It’s not the biggest peak we’ve seen. It’s not the worst peak we’ve seen,” President and CEO Shelley Simpson told investors.

The company’s brokerage business is seeing “pockets of tightness” in a few markets, but management said capacity largely remains plentiful and that the operating environment is “still extremely challenging.” The unit has incurred operating losses for 11 straight quarters, although the most recent period produced the smallest of the downturn.

The truckload business is seeing more mini-bid opportunities as some customers are struggling with service performance at other carriers and as shippers see a need to lockdown capacity given heightened regulatory enforcement on drivers. The unit has grown load counts by double-digit percentages in the past two quarters.

J.B. Hunt’s dedicated pipeline remains healthy and the company is seeing new customers inquire about service. Management said deals are taking longer to finalize from the time of inquiry, but new accounts are ramping to profitability a little faster. It estimates dedicated truck service to be a $90 billion total addressable market and it reiterated a goal for net truck additions of 800 to 1,000 annually.

Management said parts of its final-mile offering are performing well, but called out continued softness in demand for big-and-bulky delivery.

Why can’t J.B. Hunt have 2 rail partners in the East?

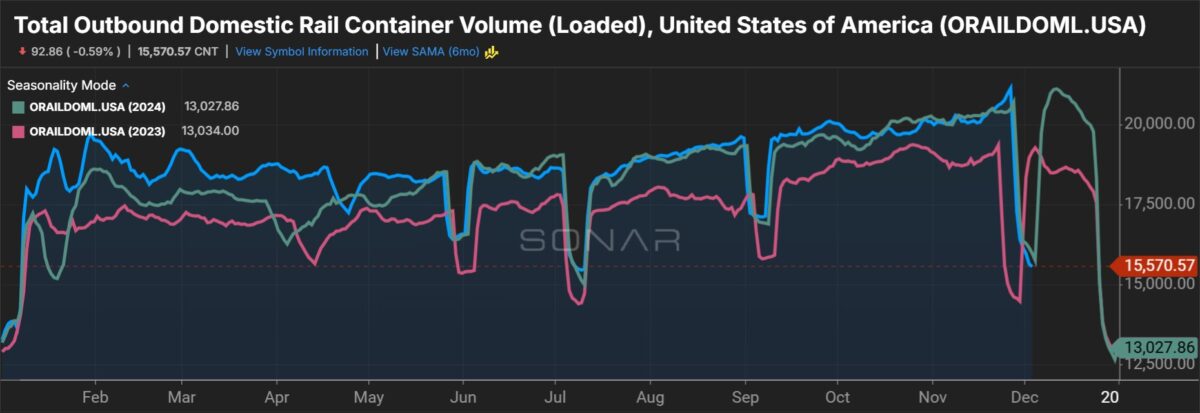

The company addressed the changing intermodal landscape following the Union Pacific (NYSE: UNP) – Norfolk Southern (NYSE: NSC) merger announcement.

Darren Field, J.B. Hunt’s president of intermodal, said the company prefers the optionality of having two different Eastern rail providers, noting that each provides something that the other doesn’t. He said any recent share shift from Norfolk Southern to CSX (NASDAQ: CSX) is a consequence of new coast-to-coast service agreements signed between its Western rail partner, BNSF Railway (NYSE: BRK.B), and CSX. He emphasized that J.B. Hunt is “not actively looking for ways to shift business from one railroad to another.”

“We’re not out trying to work on transitioning market share from Norfolk Southern to CSX,” Field added. “That’s not part of our daily effort, and we don’t have anything in the works. I think there are a number of announcements that seem to be coming out from certainly BNSF and CSX over ways that they can work together.”

J.B. Hunt reiterated its primary goal is to move freight off the road and onto the rail. It said “best-ever” service across the network is helping with road-to-rail conversion, touting recent market share wins in the East. However, it acknowledged that still-depressed truck rates and modest fuel prices are weighing on overall intermodal demand.

Operating leverage to burst through in a recovery

J.B. Hunt has tightened the belt as the downturn lingers.

It outlined a $100-million cost reduction program on its second-quarter call, but said “internal targets are much greater than that.” It views the takeouts as structural cost elimination that won’t reverse when volumes return. (In comparison, J.B. Hunt’s last-12-months’ operating income was $842 million.)

Revenue was down slightly year over year in the third quarter but operating income grew 8% as enhanced productivity and efficiency initiatives took hold. Also, the company’s headcount sits 15% below the prior peak and many of those jobs won’t be coming back given AI- and other tech-related workflow enhancements.

“I think that operational torque, or operational leverage, will show well in an environment where we’re recovering,” CFO Brad Delco said. “I feel confident that this team is set up to win regardless of what the environment is. I just don’t know what winning will look like in 2026, but I feel like we’re set up well.”

He said the company doesn’t have any outsized cash needs as it already has ample capacity for an upturn and annual maintenance capex is just $700 million (on operating cash flows of roughly $1.5 billion). That will allow the company to continue to repurchase shares (share count down 7.5% over the past two years) and fund the dividend, which it has consistently raised over the past 21 years.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now