Management from logistics real estate giant Prologis said Tuesday the nation’s warehouse market will remain tight moving forward as the supply side is facing headwinds.

The company said “true months of supply” — a measure of current vacancies and space coming online compared to trailing net absorption — stands at 30 months. The metric is up from 25 months at the close of 2022 but remains below the 10-year average of 36 months. Management believes the recent increase has more to do with a large amount of real estate coming online recently and is likely to revert quickly as leasing trends remain strong and deal financing is becoming more cumbersome.

Prologis said the industry took delivery of 375 million square feet of space last year and that 445 million square feet will be delivered this year. Vacancies are expected to rise to the 4% range in 2023 from the low-3% range last year. However, the market is normalizing and the pipeline is expected to continue to empty, which will push vacancies back into the 3% range next year.

“Demand has normalized from exceptionally high levels and the supply response has been in excess of that normalization of demand,” co-founder and CEO Hamid Moghadam told analysts on a Tuesday call. He said the knock-on effects from Silicon Valley Bank’s failure as well as broader macro concerns have resulted in a pullback in construction plans as lenders have tightened the purse strings.

Development starts were down 40% from the peak during the first quarter.

“I’ve never seen such a sudden slowdown in construction volume in our business,” Moghadam said. He noted that a downtrend was already underway prior to the SVB crisis but has worsened since.

The company maintained its 2023 forecast of 10% rent growth in the U.S. and 9% globally. CFO Tim Arndt said Prologis has traditionally held pricing power even when vacancies climb to as much as 6% and 7%, which is twice as high as what is expected next year.

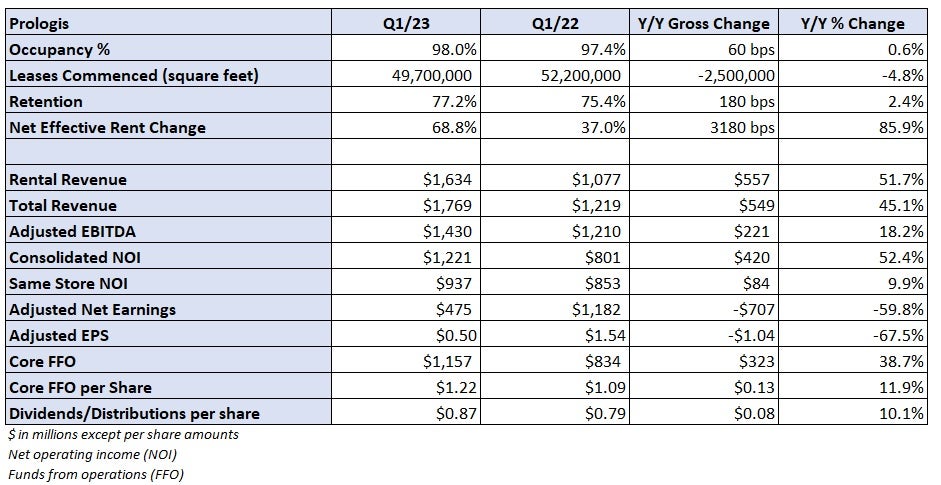

Prologis (NYSE: PLD) reported core funds from operations (FFO) of $1.22 per share in the first quarter, in line with the consensus estimate and 13 cents higher year over year (y/y). Revenue was up 45% due to prior acquisitions and increased rents. Same-store growth was up 9.9% y/y in the period.

Average occupancy across the portfolio increased 60 basis points y/y to 98%, and net effective rent change (over the entire lease term) was up by more than 30 percentage points to 68.8%. Approximately 99% of Prologis’ 1.2 billion square feet of space was either leased or in negotiation during the quarter.

Management estimated that the lease mark to market of the entire portfolio by the year end is 70%, representing an incremental $2.85 in earnings per share.

Full-year core FFO guidance was raised by 2 cents at the low end of the range to $5.42 to $5.50 per share. The current consensus estimate was $5.50 at the time of the print. Management made no changes around its plans for stabilizations, starts and acquisitions in 2023.

Average occupancy guidance was raised slightly to a range of 97% to 97.5%.

“I would describe market conditions as very good to excellent,” Moghadam continued. “They’re not exceptional like they were a year and a half or two years ago.”

Management said it has ample capital and will remain opportunistic in the market.

Prologis ended the quarter with $6.7 billion in liquidity, which included $3.6 billion in recent debt issuances and a $1 billion increase to its revolving credit line. Debt-to-market capitalization was 19.1%, 100 bps lower than at the end of 2022.

“I think the supply response has been much more dramatic than the effect on demand. That’s why the market is going to tighten up again,” Moghadam said.

Editor’s note: Prologis Ventures is an investor in FreightWaves.

More FreightWaves articles by Todd Maiden

- ‘Freight recession’ snares J.B. Hunt in Q1

- Freight shipments, costs sag in March

- Container lessor Triton to go private in $13.3B deal

Look for margin expansion in CPG earnings

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now