Schneider National announced first-quarter earnings ahead of analysts’ expectations on Thursday but lowered its outlook for 2025.

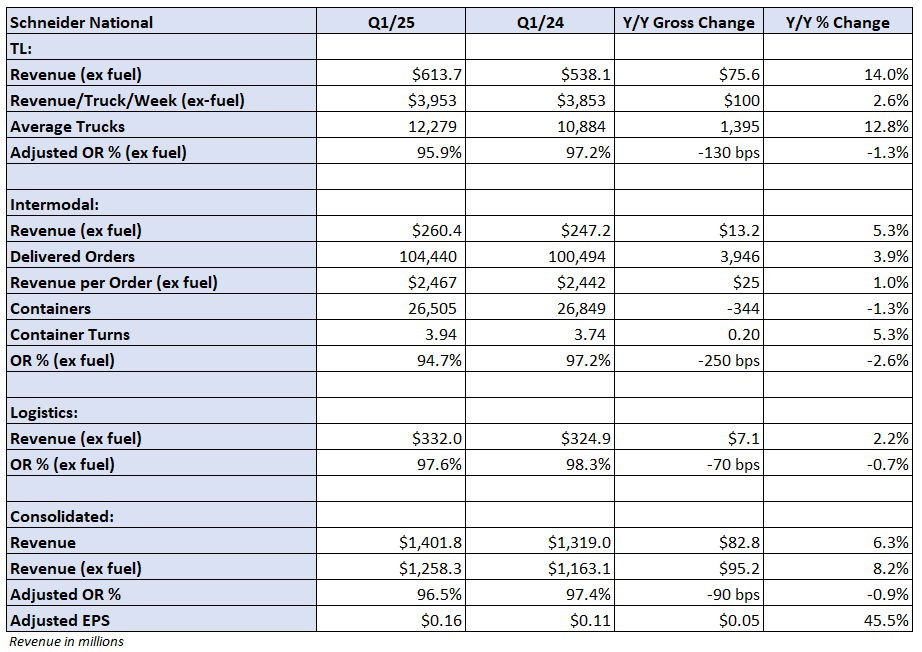

Schneider (NYSE: SNDR) reported adjusted earnings per share of 16 cents, 2 cents ahead of the consensus estimate and 5 cents higher year over year. The y/y increase was driven by the December acquisition of Cowan Systems. The adjusted EPS number excluded 1 cent per share in acquisition costs.

Full-year guidance was cut to a range of 75 cents to $1 from the initial guide of 90 cents to $1.20 (a 17% reduction at the midpoints). However, the new outlook bracketed the 89-cent consensus estimate at the time of the print. (Analysts have been lowering estimates in recent weeks to reflect potential demand destruction from a protracted trade war.)

“While the current macro-economic environment is leading to declining consumer sentiment and increasing shipper uncertainty, we expect to deliver improved year over year results through 2025, although tempered versus our previous outlook,” said Schneider CFO Darrell Campbell in a news release.

Click for full report – “Tariffs trim Schneider National’s 2025 growth expectations”

Schneider’s truckload segment reported a 14% y/y revenue increase to $614 million. The bulk of the increase was tied to the acquisition, but revenue per truck per week in both its dedicated and one-way segments increased by approximately 2% y/y as rate per mile increased.

Like many carriers in the industry, Schneider has worked to cull its one-way fleet to improve utilization. Revenue per truck per week, however, was off 4% sequentially for the entire TL fleet from the fourth quarter to the seasonally weakest first quarter.

The unit reported a 95.9% operating ratio (inverse of operating margin), 130 basis points better y/y and 60 bps better than the fourth quarter.

Click for full report – “Tariffs trim Schneider National’s 2025 growth expectations”

The company’s intermodal segment reported a 5% y/y increase in revenue and 250 bps of OR improvement to 94.7%.

Schneider also saw 70 bps of margin improvement in its logistics business.

“Revenues excluding fuel surcharge of nearly $1.3 billion were the second highest for a first quarter in our history, and all our reportable segments improved revenues, earnings, and margin year over year. As the quarter progressed, increasing economic uncertainty lowered consumer sentiment and market expectations,” said Schneider President and CEO Mark Rourke in a news release.

Shares of SNDR were off 0.5% at 9:49 a.m. EDT on Thursday compared to the S&P 500, which was up 1%.

Schneider will host a conference call to discuss first-quarter results at 10:30 a.m. EDT on Thursday.