This week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 30 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 35 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Consumer debt is a looming headwind for future freight demand

In terms of freight volume, truckload markets have continued to express a trend of typical seasonality. Freight demand was relatively stable throughout late January and much of February but is now slowly beginning to ramp up at the start of March. A few factors are providing slight tailwinds to volume growth: After reaching a nadir in early February, the flow of ocean freight from China to the U.S. is shaking off the lull created by the former country’s Lunar New Year celebrations. Produce season, which first affects markets in Florida and Texas (including Texas’ cross-border markets), is just around the corner.

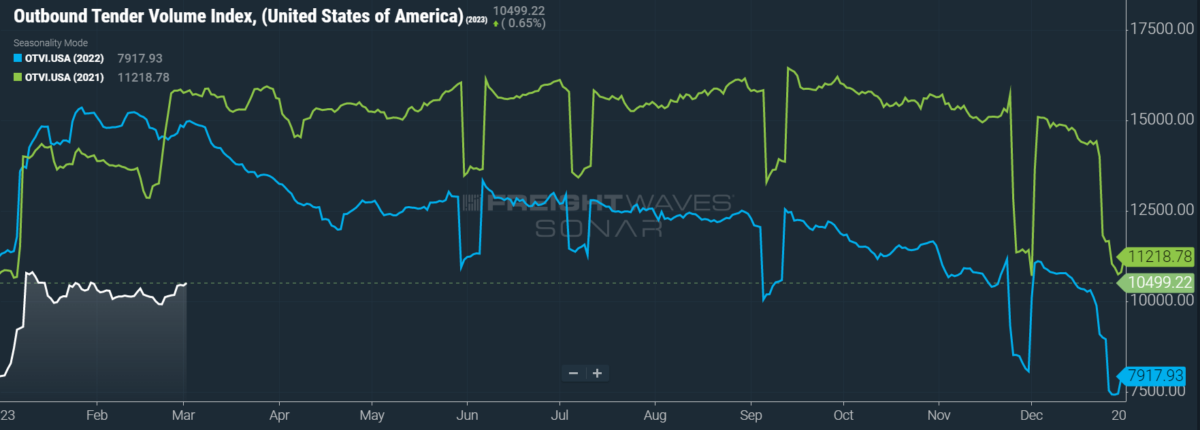

SONAR: OTVI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

This week, the Outbound Tender Volume Index (OTVI), which measures national freight demand by shippers’ request for capacity, rose 3.85% on a week-over-week (w/w) basis. On a year-over-year (y/y) basis, OTVI is down 30%, although such y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be artificially inflated by an uptick in the Outbound Tender Reject Index (OTRI).

SONAR: CLAV.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volumes (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a rise of 3.73% w/w as well as a fall of 16.8% y/y. This y/y difference confirms that actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI lower.

Earlier this week, FreightWaves CEO Craig Fuller sat down with Zach Strickland, the “Sultan of SONAR,” to discuss current market trends. Their conclusion, with which I agree, is that the market is presently in a confusing state of stable imbalance: stable, because freight demand has not totally cratered and is abiding by seasonality once again, but imbalanced, because there is still a glut of capacity from the 2020-21 gold rush. Although deteriorated, contract rates (discussed below) escaped from the worst possible Q1 scenario. Much worse is the prolonged atrophy in spot rates, which has proved punishing for smaller, newer carriers.

A healthy number of industry analysts predict that consumer demand for goods will return in the second half of 2023, spurring truckload volumes and returning a bit more balance to the market. I am not overly hopeful about this forecast, however. On Tuesday, the U.S. Supreme Court heard arguments on the Biden administration’s plan to forgive $430 billion in federal student loans. The court’s conservative majority expressed doubts about the legality of such forgiveness, though some of these justices also questioned if the plaintiffs had the requisite legal standing to press the issue. Whether such forgiveness will be approved or denied will likely remain uncertain until June; student loan repayments will resume in late August after a three-year hiatus.

Non-revolving credit, a category that includes student loans, has risen steadily over the past five years. This consistent trend is in stark contrast to that of revolving credit, debt which includes credit card balances. After receiving stimulus money from the pandemic measures of 2020-21, consumers rapidly paid off their credit cards and then splurged on household goods, largely neglecting to put these funds toward their student loans. When student loan repayments come back into effect, particularly if the court rules their forgiveness unconstitutional, it will majorly dampen consumers’ already-weakened demand for goods, driving down freight volumes and possibly kickstarting — or worsening — a broad economic recession.

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, 83 reported weekly increases in tender volume, with large and small markets alike benefiting from returning freight demand.

Over the past seven days, a diverse assortment of markets benefited from a seasonal uptick in shippers’ activity, including seaport markets and heavyweight industrial regions. The market of Ontario, California, which stores and distributes freight from the nearby ports of Los Angeles and Long Beach, saw volumes climb 5.68% w/w. Seattle, which is both a cross-border market and a port market in its own right, saw a 14.1% w/w increase in freight demand. Michigan’s two manufacturing hubs of Detroit and Grand Rapids, meanwhile, saw respective w/w gains of 8.6% and 11.11% in tender volumes.

By mode: Heavy winter storms drove reefer volumes in the Upper Midwest and the Northeast this week, as shippers strove to protect their temperature-sensitive goods from freezing. Accordingly, reefer volumes saw their highest growth in relatively small markets, such as those of Cedar Rapids, Iowa, and Syracuse, New York. Though to a lesser degree, appreciable growth was also seen in the major reefer markets of Lakeland, Florida, and Joliet, Illinois. On a national scale, then, the Reefer Outbound Tender Volume Index (ROTVI) rose a solid 4% w/w. Produce season, which begins in Florida and Texas, is right around the corner and ROTVI, if it is truly abiding by seasonal trends, should see corresponding growth. Though ROTVI is down 27.45% y/y, accepted reefer volumes are actually up by a slim 0.9% y/y.

Van volumes, meanwhile, are slightly underperforming against the overall OTVI. The Van Outbound Tender Volume Index (VOTVI) is up 3.16% w/w. As discussed above, I do not see a terribly bright future for consumer-driven van volumes over the coming months, especially since student loan repayments are set to resume right as the back-to-school and holiday shopping seasons kick off. While VOTVI is down 31.2% y/y, accepted van volumes are only down 18.4% y/y.

In like a lion …

Rejection rates are slowly climbing, albeit to a fairly insignificant degree. This recent uptick is less likely to mark the resurgence of tender rejections, given the persistent overabundance of capacity in the market, and more likely to signal that rejection rates have reached their point of dynamic equilibrium for the foreseeable future. A recent outbreak of severe weather, however, might throw a wrench into capacity in the coming days.

SONAR: OTRI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, rose to 3.55%, a change of 12 basis points (bps) from the week before. OTRI is now 1,512 bps below year-ago levels.

Earlier this week, load board provider Truckstop.com announced a wave of layoffs to its roughly 800 employees. The size of these layoffs, which are rumored to be the second wave in as many months, is currently unknown. On Thursday, a spokesperson for Truckstop.com did not address the layoffs directly, saying instead that the software-as-a-service company “restructured [its] organization” in order to “operate more efficiently and deliver more customer value.” As faithful readers of this column know, these layoffs are just another falling domino in a chain of layoffs that include the digital freight platform Convoy, freight forwarder Flexport and logistics provider Ryder, among others.

Despite this doom and gloom, supply chain SaaS provider Descartes is cautiously optimistic for the remainder of 2023. While acknowledging the impact of inflation, higher interest rates and the instability of commodity markets following Russia’s invasion of Ukraine, Descartes noted that its retail shipping customers anticipated growth in shipment volumes in the back half of the year. Descartes, a company known for its aggressive acquisition strategy, said that its latest acquisition of final-mile automation platform GroundCloud presented a minor headwind for the near term as its integration is settled.

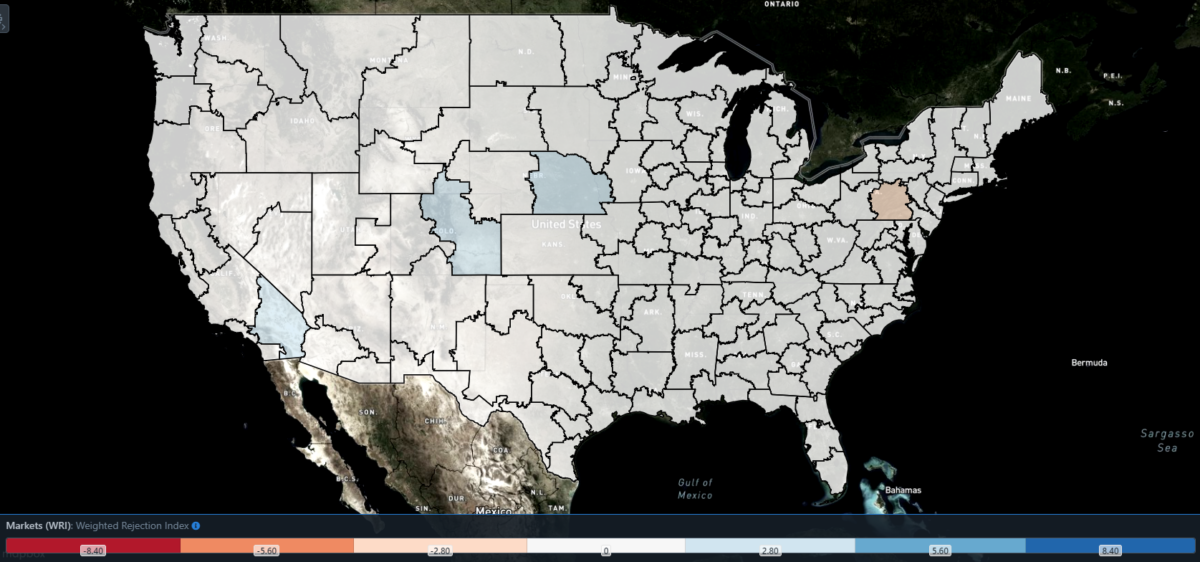

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight this week, a few regions posted blue markets, which are usually the ones to focus on.

Of the 135 markets, 71 reported higher rejection rates over the past week, though 48 of those saw increases of only 100 or fewer bps.

Since OTRI, both on a national and market level, is calculated as a seven-day moving average, the effects of recent storms have yet to be felt fully. But a rash of severe weather, including tornadoes and flash floods, has been marching from Texas and Louisiana across the Southeast, disrupting capacity in the region. These storms are expected to push into the Northeast and Midwest in the coming days, bringing heavy rain and snowfall.

For the time being, however, markets like Denver are still reeling from the hazardous weather visited upon them several days prior. Last week, a snowstorm caused flight delays and heavy traffic in the Denver region, setting a new record-low temperature on Thursday. Accordingly, Denver’s local OTRI ballooned by 400 bps w/w to 10.32%. This performance was outdone by its regional neighbor of Omaha, Nebraska, which similarly suffered from winter storms and slick conditions on its roads. Omaha’s OTRI climbed 402 bps w/w to 15.56%, the second highest in the nation.

To learn more about FreightWaves SONAR, click here.

By mode: Flatbed rejection rates retained distance from their low of 8.43% in early February, despite negative signals from the manufacturing and construction sectors. The Flatbed Outbound Tender Reject Index (FOTRI) dipped 12 bps w/w to 14.49%, but it has remained relatively stable over the past nine days. High mortgage rates continue to put the squeeze on construction of single-family homes, though recently released data shows that January spending on nonresidential construction saw slight growth over December.

Surprisingly, given the latest uptick in reefer demand, the Reefer Outbound Tender Reject Index (ROTRI) performed worse. This week, ROTRI fell 18 bps w/w to 3.81%, putting it within spitting distance of the Van Outbound Tender Reject Index (VOTRI), which rose 10 bps w/w to 3.38%. That ROTRI should be so near to VOTRI is unusual, since reefers are generally a more costly mode of transport with a lower ratio of capacity to demand. Nevertheless, ROTRI does have some hope on the horizon with the upcoming produce season, while VOTRI has few sources of upward pressure in the near future.

Contract rates sidestep catastrophe

For the most part, contract rates are locked into a steady pace for the remainder of Q1. With the expectation that they will not change drastically until at least April, contract rates have avoided the worst-case scenario of a 7% to 9% quarterly fall from Q4 2022. Even so, they are currently locked into a level 5% below Q4’s average, which will negatively impact larger carriers’ bottom lines in the next round of earnings calls.

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

Contract rates, which exclude fuel surcharges and other accessorials, remained flat on a w/w basis at $2.54 per mile. Since contract rates are reported on a two-week delay, the current data displays trends seen in mid-February. If the aforementioned weather conditions prove anywhere near as devastating as the 2021 winter freeze, there is still room for contract rates to rise accordingly, but such gains are unlikely at the time of writing.

Mirroring OTRI’s stability, spot rates appear to be leveling out. This good news should be tempered by a reminder that spot rates retain the possibility to fall even further and that the National Truckload Index (NTI) — which includes fuel surcharges and other accessorials — has already declined more than 8% from its average in Q4 2022. This week, the NTI rose 2 cents per mile w/w to $2.39. The linehaul variant of the NTI (NTIL), which excludes fuel surcharges and other accessorials like contract rates, saw a higher gain of 3 cents per mile w/w to $1.71, which indicates that falling diesel prices arrested some of the NTI’s growth.

To learn more about FreightWaves SONAR, click here.

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the data set, which dates to early 2019. Throughout that year, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs on a seemingly weekly basis, while contract rates slowly crept higher throughout 2021.

Despite this spread narrowing significantly over the first few weeks of the year, tightening by 20 cents per mile in January, it has continued to widen again. Since linehaul spot rates remain 83 cents below contract rates, there is still plenty of room for contract rates to decline over the coming months.

To learn more about FreightWaves TRAC, click here.

The FreightWaves TRAC spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, has been on an unstoppable decline since mid-January. Over the past week, the TRAC rate fell 5 cents per mile to $2.01, a far cry from its year-to-date high of $2.39. The daily NTI (NTID), which sits at $2.42, is greatly outpacing rates from Los Angeles to Dallas.

To learn more about FreightWaves TRAC, click here.

On the East Coast, especially out of Atlanta, rates have been fairly steady over the past few weeks but are similarly outpaced by the NTID. The FreightWaves TRAC rate from Atlanta to Philadelphia rose 2 cents per mile this week to reach $2.36. Except for Q4’s holiday run, rates along this lane have been dropping stepwise since July 2022, when the TRAC rate was $3.48 per mile.

For more information on the FreightWaves Passport, please contact Michael Rudolph at mrudolph@www.freightwaves.com or Tony Mulvey at tmulvey@www.freightwaves.com.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now