To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here.

Retailers, most CPGs at odds over prices

With the prices of many consumer packaged goods products about 15% higher than this time last year and 20%-25% higher than this time two years ago, and following visible declines in commodity prices, retailers and CPG companies are at odds over where prices go from here.

Whole Foods has reportedly told suppliers that it expects price reductions and, according to the CEO of Edgewell Personal Care Co., Walmart is making it harder for suppliers to raise prices. Retailers, in general, are gaining market share with their private-label brands, which are growing sales at roughly double the rate of the national brands after a record 2022 and, according to TreeHouse Foods (a manufacturer of private-label packaged foods), are priced 25%-30% below the national brands. That price gap and retailers’ recent investments in their private labels could limit CPG companies’ ability to take prices up further.

In addition to Edgewell, a few other CPG companies have recently suggested that most price hikes are behind them, including PepsiCo, Kraft Heinz and Clorox. It’s worth noting that some of those same companies’ retail prices are up by double digits year over year and just went through their latest price increase round in the past few months.

Meanwhile, many other CPGs say that the declines in traded commodity prices do not reflect their company-specific costs, and, therefore, additional commensurate price increases are necessary. Here are a few examples:

- Nestle’s management said its pricing still has “catching up to do” given its cost increases. Its anticipated 6%-8% sales growth forecast this year will be “pricing-led.” Nestle’s management also said that changes in pricing from here on will be “targeted by category.”

- Unilever’s outgoing CEO said we are past peak inflation, but not past peak prices.

- TreeHouse Foods’ management said despite traded commodity costs having come way down, the company’s nontraded expenses, such as packaging, labeling and labor, are still rising.

- Mondelez’s management said its costs are still rising by double digits this year, which should be reflected in prices.

- Coca-Cola and Procter & Gamble have also suggested that prices will rise further.

In short, the national branded food companies are not interested in cutting prices to reflect the decline in commodities, but it appears that the inflationary rate will decelerate this year to something in the single digits. That might feel like a relief to consumers after the past two years. While pressure from retailers is rising (both directly as well as indirectly via promotion of, and investment in, private labels), rising elasticities would be a bigger driver of changes to CPG pricing. So far, CPG elasticities have remained relatively muted based on historical trends, but that seems to have changed slightly the past two quarters.

End of SNAP emergency allotments to hit packaged food demand

Next month, the end of the three-year enhancement to food-stamp benefits is poised to have a significant impact on both retailers and packaged food companies. At times, the big-box retailers have highlighted the beginning of the month as a period of heavy sales as a result of benefits cards being turned on as the month begins, which also complicates their supply chains.

The Wall Street Journal had a good article on this. Here are a few statistical highlights:

- SNAP benefits made up 12.3% of total at-home food and beverage sales, up from 7.1% in 2019.

- SNAP participants in 35 states will lose $95 a month in benefits starting in March, or $3 billion in total. A three-person household would see its benefits go from $759 a month to $592.

- After the offsetting cost-of-living adjustment, SNAP benefits will decline 7% on a net basis.

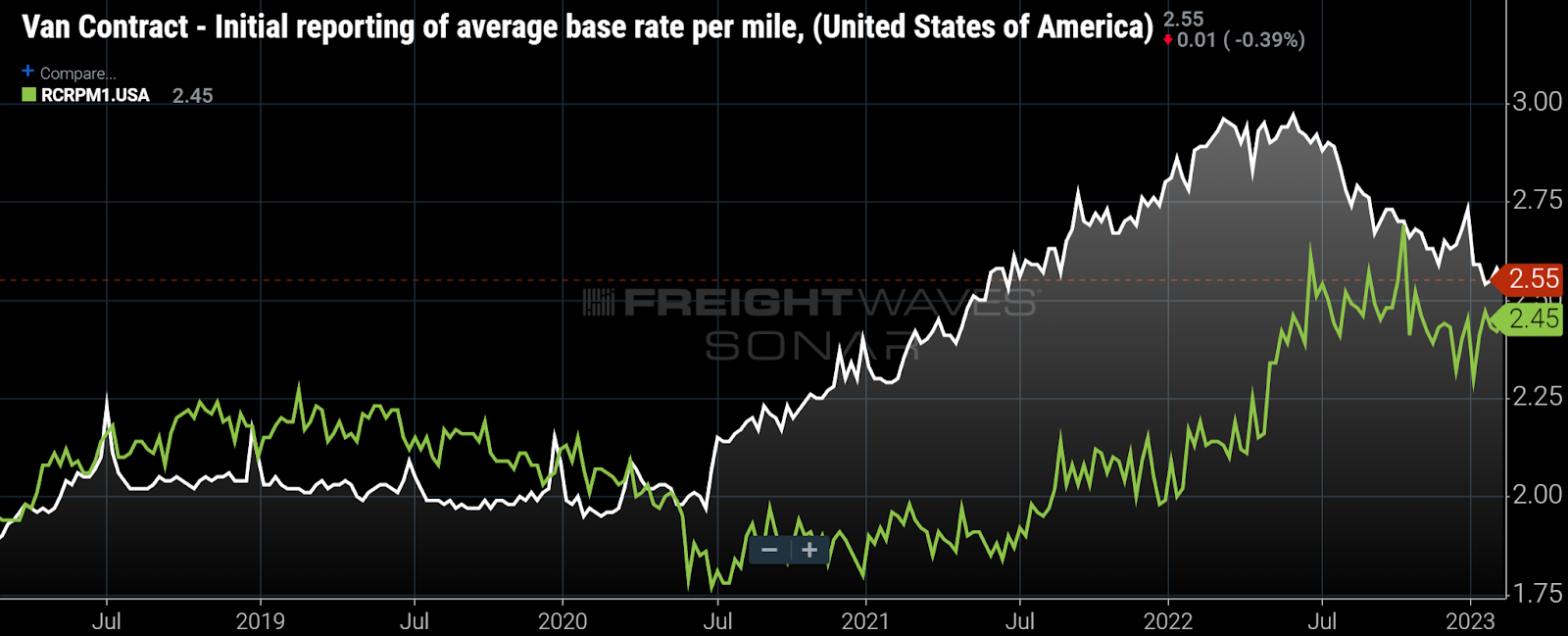

Additional evidence that dry van contract rates have further to fall?

In last week’s newsletter, I discussed the still-meaningful premium that dry van contract rates have over comparable dry van spot rates. That spread suggests that dry van contracts have further to fall.

The chart below, which compares two distinct markets — dry van and reefer — shows that freight markets, in general, have not yet normalized. Under typical conditions, reefer rates per mile should be above dry van rates to reflect reefer’s higher equipment and higher operating costs as well as a more concentrated carrier segment.

Yet, since mid-2020, dry van rates have been higher than reefer and reefer rates have reacted less aggressively to tight capacity conditions during the pandemic. And, dry van linehaul rates remain 10 cents above reefer linehaul rates. Throughout an economic cycle, dry van rates tend to be more volatile in both directions, so I would not be surprised to see the two lines in the chart below cross again in the coming quarters.