Spot rates in the trans-Pacific ocean trade continue to reach epic new heights, leading to talk of price gouging.

“Container lines have done well during the global pandemic, but are they profiteering from the crisis?” asked U.K.-based consultancy Drewry.

“Perversely, lines look set to make more money than they have in a long time,” Drewry continued. The practice of “blanking” (canceling) sailings “has paid off handsomely.”

“From a public-relations perspective, the optics of making big profits during a global crisis are not great” and will lead to “more animosity and accusations of profiteering,” said Drewry, adding that it “is inclined to give carriers the benefit of the doubt for now.”

The ultimate question is: Will trans-Pacific rates prompt action by the Federal Maritime Commission (FMC), the agency that oversees alliances?

The answer appears to be: highly unlikely.

First, the FMC has given carriers specific permission to blank sailings in line with demand. Second, blank sailings are now rapidly dwindling at the same time spot rates are rising. And third, carrier agreements with the FMC do not forbid reasonable price increases and service decreases.

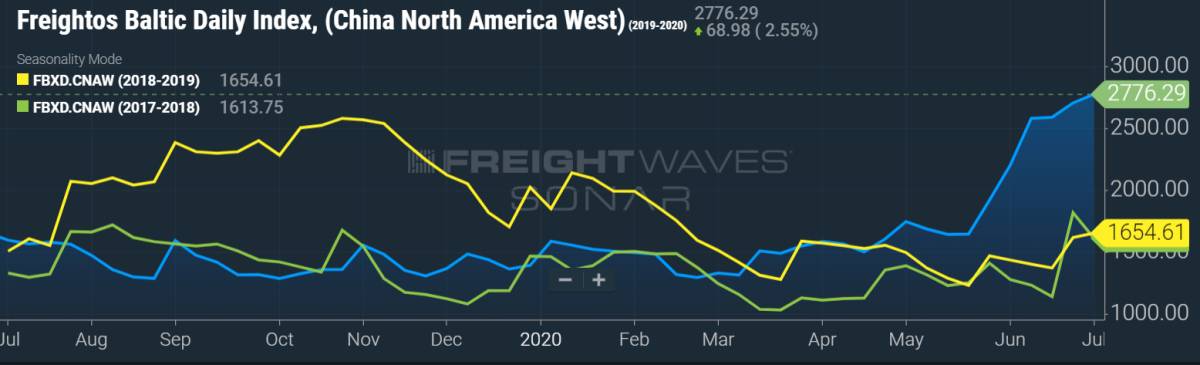

New peak for spot rates

Asia-West Coast spot rates (SONAR: FBXD.CNAW) were $2,776 per forty-foot equivalent unit (FEU) as of Monday, according to the Freightos Baltic Daily Index. That’s up around 70% versus the past two years and more than double late-February lows.

The Shanghai Containerized Freight Index put the cost even higher, estimating the Shanghai, China-West Coast rate at $2,920 per FEU for the first week of July, at or above decade highs.

At the beginning of this month, carriers successfully implemented their third general rate increase (GRI) in the past six weeks. According to Freightos Chief Marketing Officer Eytan Buchman, this “is a rarity in ocean rates that didn’t even happen in the lead-up to the trade war in late 2018.”

Blank-sailing permission for alliances

There wouldn’t be any debate on anti-competitive pricing if the container sector were not so acutely consolidated.

Alphaliner estimates that the alliances now control 89% of the market share between Asia and North America (including both coasts). The 2M Alliance (Maersk, MSC) controls 20%. The Ocean Alliance (COSCO/OOCL, CMA CGM/APL, Evergreen, HMM) has 39%. And THE Alliance (Hapag-Lloyd, ONE, Yang Ming) has 30%.

A letter to the FMC from the European Shippers Association (ESA) in September 2014, prior to 2M’s approval, exemplifies concerns toward alliances.

“Accepting that operators can ‘blank sailings’ can clearly be seen as market manipulation to restore freight rates if needed by playing on the supply side,” argued the ESA. It warned that cooperative agreements would allow carriers to “distort the market for the purpose of price increases.”

The FMC approved 2M and other alliances over shipper association objections. Alliance agreements with the FMC state, “The parties are authorized to blank sailings when utilization is likely to fall below such thresholds as may be established by the parties” and “blankings must be proportionate to the expected fall in demand.”

If at any time the FMC determines that an alliance agreement creates “an unreasonable reduction in transportation service or an unreasonable increase in transport cost” as a result of “a reduction in competition,” the FMC can bring a civil action in the District of Columbia district court “to enjoin the operation of the agreement.”

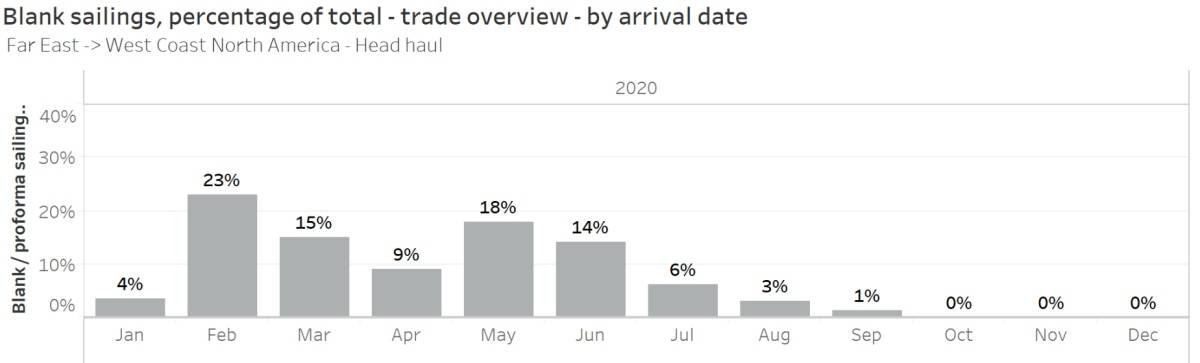

Blank sailings sharply reduced

By this standard, it’s hard to imagine how the trans-Pacific situation would elicit court action.

Carriers did indeed reduce capacity in the second quarter. But they did so in line with “the expected fall in demand,” which was inherently uncertain given the unprecedented nature of the coronavirus outbreak. As it turned out, demand exceeded expectations, so carriers added some sailings back in.

Rates are now rising despite carriers canceling many fewer sailings. Thus, rates are rising because demand is up, not because of a “reduction in competition” (i.e., reduced capacity).

Buchman described the early July GRI as “remarkable” because it was “happening as carriers have largely returned capacity to normal levels.”

Data provided to FreightWaves by eeSea.com shows that carriers blanked 12.7% of Asia-West Coast sailings in the second quarter, but only 3.3% so far for the third quarter (6% this month, 3% August, 1% September).

Surging US demand

Tightly restricted capacity increased rates in June, said Buchman. But demand is the rate driver this month, with importers favoring the West Coast over the East Coast.

“This demand surge is likely driven by many U.S. businesses adding inventory that’s finally run down since their last orders in May or April,” Buchman said. “As restrictions in some areas are reduced, businesses are reopening and even U.S. manufacturing is recovering somewhat.”

He added, “Some of this demand in what may be an early peak season could be motivated by the August expiration of certain tariff exemptions for hundreds of products, from coffee filters to skateboards.”

The reasonableness factor

While China-West Coast spot rates are extremely steep, it seems highly unlikely that they meet the regulatory threshold of being “unreasonable.”

According to FreightWaves Maritime Market Expert Henry Byers, some cargo shippers passed on the option to sign annual contracts at lower rates in April, wagering that they could do better in the spot market. Higher rates being paid by shippers are, at least to some extent, a function of their own bet on market direction. Is it unreasonable that some shippers pay more for betting wrong on rate trajectory?

SeaIntelligence Consulting CEO Lars Jensen also highlighted the reasonableness factor. “In very round numbers, ocean freight accounts for 1.3 cents of each dollar of goods,” he wrote. “The rate increase in 2020 means that each dollar of goods has seen a freight rate increase of $0.0009. Is that tantamount to profiteering?”

He continued, “My own recent estimate was that if carriers can maintain the [first-half rate] increase they could see profits of $9 billion in 2020. If they fail, the year could still end at a loss of $7 billion.

“Is $9 billion an unreasonable profit?” he asked, pointing to a McKinsey report estimating that carriers destroyed $110 billion in value on invested capital in 1995-2016. Jensen emphasized that this track record is clearly unsustainable. Click for more FreightWaves/American Shipper articles by Greg Miller

MORE ON BLANK SAILINGS: For an in-depth Q&A on blank sailings with Sea-Intelligence CEO Alan Murphy, see story here. For extensive data on blank sailings from eeSea.com, see story here. For a comparison of second- and third-quarter blank sailings to U.S. ports, see story here.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now