The green shoots keep coming.

Fewer trans-Pacific sailings will be “blanked” (canceled) in the third quarter — potentially many fewer — as U.S. importers recuperate from the first COVID-19 wave more quickly than expected.

Blank-sailing data has proved to be an accurate leading indicator of U.S. demand.

When ocean carriers do not get enough advance bookings to sufficiently utilize container slots, voyages are canceled. With blank sailings announced a month or more in advance, liner scheduling decisions offer a window on forward U.S. import demand, and by extension, the health of the U.S. economy.

It’s now less than two weeks until the start of the third quarter. Ships arriving early in the quarter have either already left Asia or are about to. If the 2M Alliance (Maersk, MSC) was going to announce large-scale blankings for the third quarter, it probably would have done so by now. 2M announced third-quarter blankings for the Asia-Europe route back on June 3.

New data on blank sailings

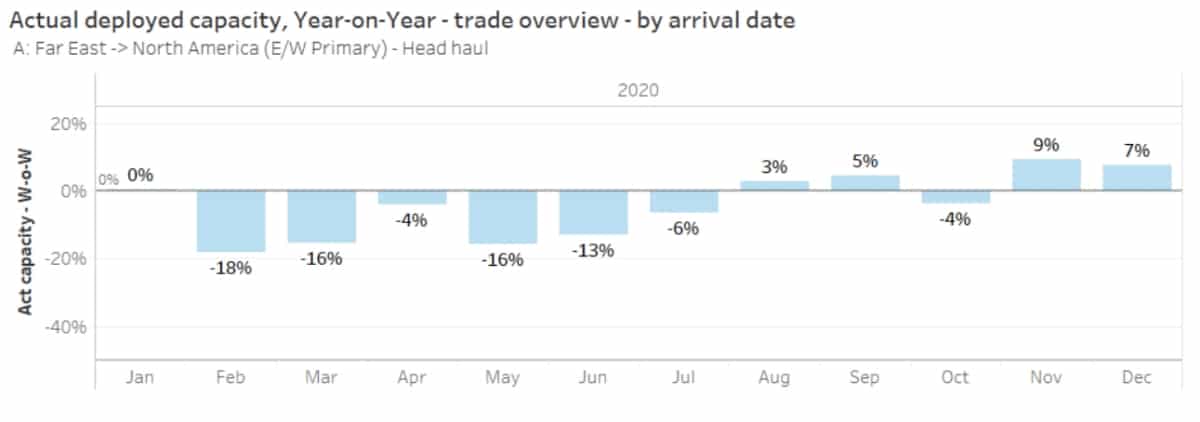

Detailed trans-Pacific blank-sailing data is provided to FreightWaves by Copenhagen-based eeSea. The latest data, calculated based on the arrival date in the U.S., not the departure date from Asia, shows a stark difference in scheduling in the third quarter versus the second.

As of Wednesday, only 26 blank sailings had been announced for third-quarter U.S. arrivals, compared to 105 in April-June.

“Blank sailings in the third versus second quarter are definitely down,” eeSea founder Simon Sundboell told FreightWaves. “That’s a sign — if it wasn’t clear already — that we’re coming out of a very abnormal trough. There’s still room for some cancellations in August and September, but I’m not sure they’ll come.”

Blank sailings represented 14% of total sailings originally scheduled to arrive in the second quarter. So far, they’re averaging only 3% for third-quarter arrivals.

The caveat, said Sundboell, is that “the level of capacity [in the third quarter] is still down year-on-year, so that points to a weaker peak season than in 2019,” despite fewer blank sailings in the third quarter than the second.

Too many blank sailings in 2Q

Carriers blanked too much capacity in the second quarter amid uncertainty about U.S. demand. The evidence that they overshot: Several blank sailings were reinstated, “extra loaders” (extra sailings) were added, and trans-Pacific rates have jumped.

“The surging trans-Pacific spot freight market shows how capacity decisions will be challenging as the world emerges from lockdown,” commented U.K.-based consultancy MSI in its June market outlook.

Eytan Buchman, chief marketing officer of Freightos, marveled at current rate strength on the trans-Pacific, noting that rates were at a two-and-a-half-year high and carriers were able to implement not one but two general rate increases (GRIs) in June. He said it was the first instance of two successful GRIs in one month since January 2019, “which is all the more striking for happening … with much of the world entering or in a recession.”

Buchman attributed the rate spike to a combination of increased U.S. import demand and restricted carrier capacity.

On Wednesday, the Freightos Baltic Daily Index for the China-West Coast route (SONAR: FBXD.CNAW) was at $2,408 per forty-foot equivalent unit (FEU), up 85% from its late-February lows and up over 40% versus rates at the same time in 2019 and 2018.

Higher-than-expected rates are translating into improved financial outlooks. A.P. Moller-Maersk (APM) just revised its second-quarter outlook, estimating that volume will fall 15%-18% versus the previous estimate of 20%-25%, and that its second-quarter adjusted earnings before interest, taxes, depreciation and amortization should be slightly higher than in the first quarter.

APM CEO Soren Skou asserted Wednesday that the company has been successful in “adjusting capacity to demand to maintain high utilization.”

What’s next for trans-Pacific?

In the second quarter, 2M announced its blank-sailing schedule early and for much of the entire quarter. THE Alliance (Hapag-Lloyd, ONE, Yang Ming, HMM) followed suit, while the Ocean Alliance (CMA CGM/APL, COSCO/OOCL, Evergreen) made cancellations on a more piecemeal and strategic basis but ultimately canceled around the same percentage of sailings as the other two.

However, the alliances may not announce third-quarter blank sailings in the same pattern. They could opt to decide on cancellations throughout the quarter, meaning the currently low blanking percentage could turn out to be somewhat deceptive.

“The carriers could be waiting to see who pulls the trigger first and jostling for market share,” said Sundboell.

If the alliances do end up keeping most of their third-quarter schedules intact, they could start competing more on price, which could bring trans-Pacific rates back down again.

According to Frode Mørkedal, managing director of equity research at Clarksons Platou Securities, “Idle capacity through blanked sailings is likely to be gradually returned [starting in] the third quarter, which could result in lower freight rates per TEU [twenty-foot equivalent unit].”

“The spike in trans-Pacific spot rates is likely to be a temporary phenomenon, but it seems liner companies are more likely to under- than overestimate volumes across different trade lanes,” said MSI. “Market share-grabbing strategies remain a risk, but the evidence of the crisis so far suggests that undercutting [price] activity is not an attractive strategy for the major liner companies.” Click for more FreightWaves/American Shipper articles by Greg Miller

Freight Fraud Symposium

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Rock & Roll Hall of Fame • Cleveland, OH Register NowPast the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post Office • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now