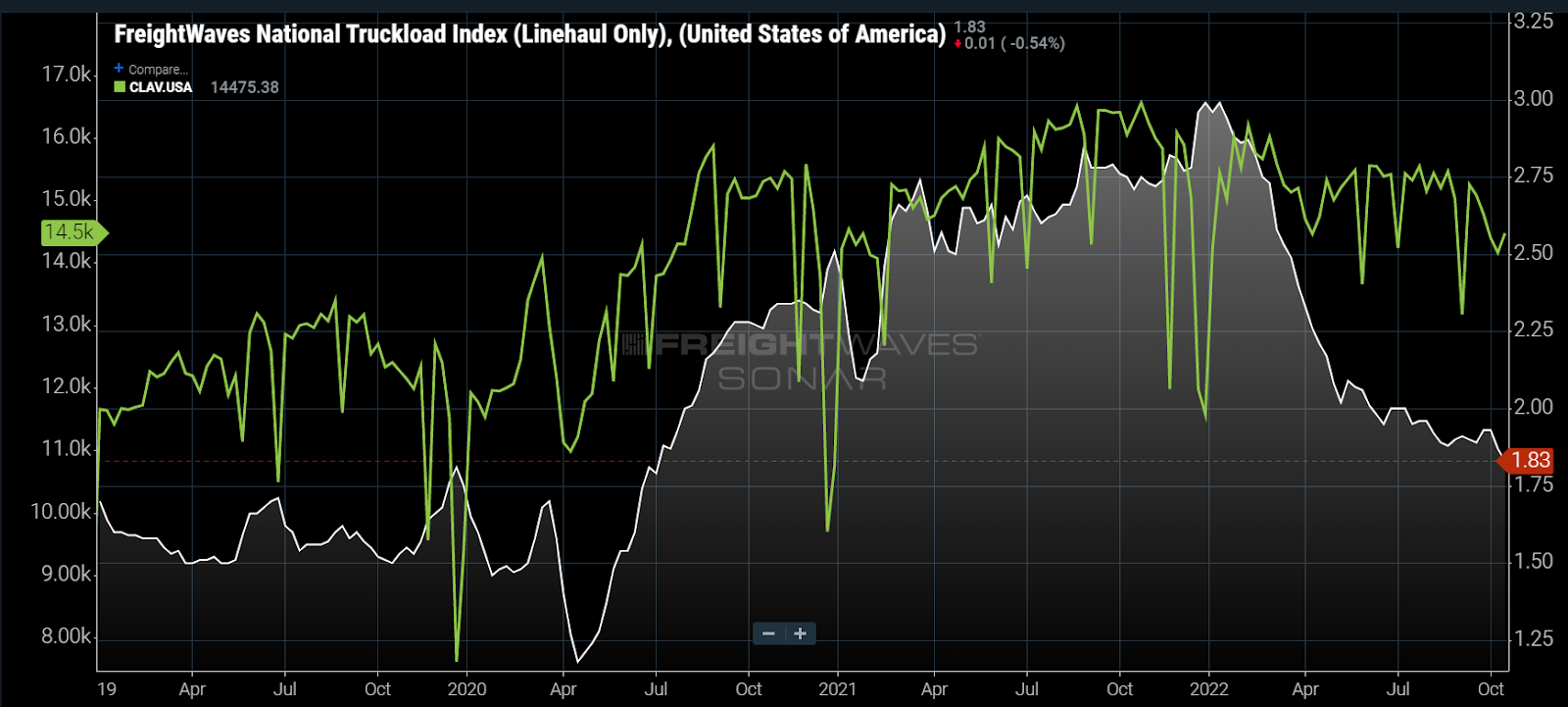

Chart of the Week: National Truckload Index (Linehaul Only), Contract Load Accepted Volume – USA SONAR: NTIL.USA, CLAV.USA

Truckload spot rates excluding total estimated fuel costs have dropped 37% since their peak value achieved in the first week of January, according to the National Truckload Index, Linehaul Only (NTIL).

The bulk of that decline occurred in a 13-week period between the first week of February and early May, leveling off throughout most of the summer and early fall. Demand appears to be on shaky ground once again with a drop in accepted volumes earlier this month.

How much room do spot rates have to fall?

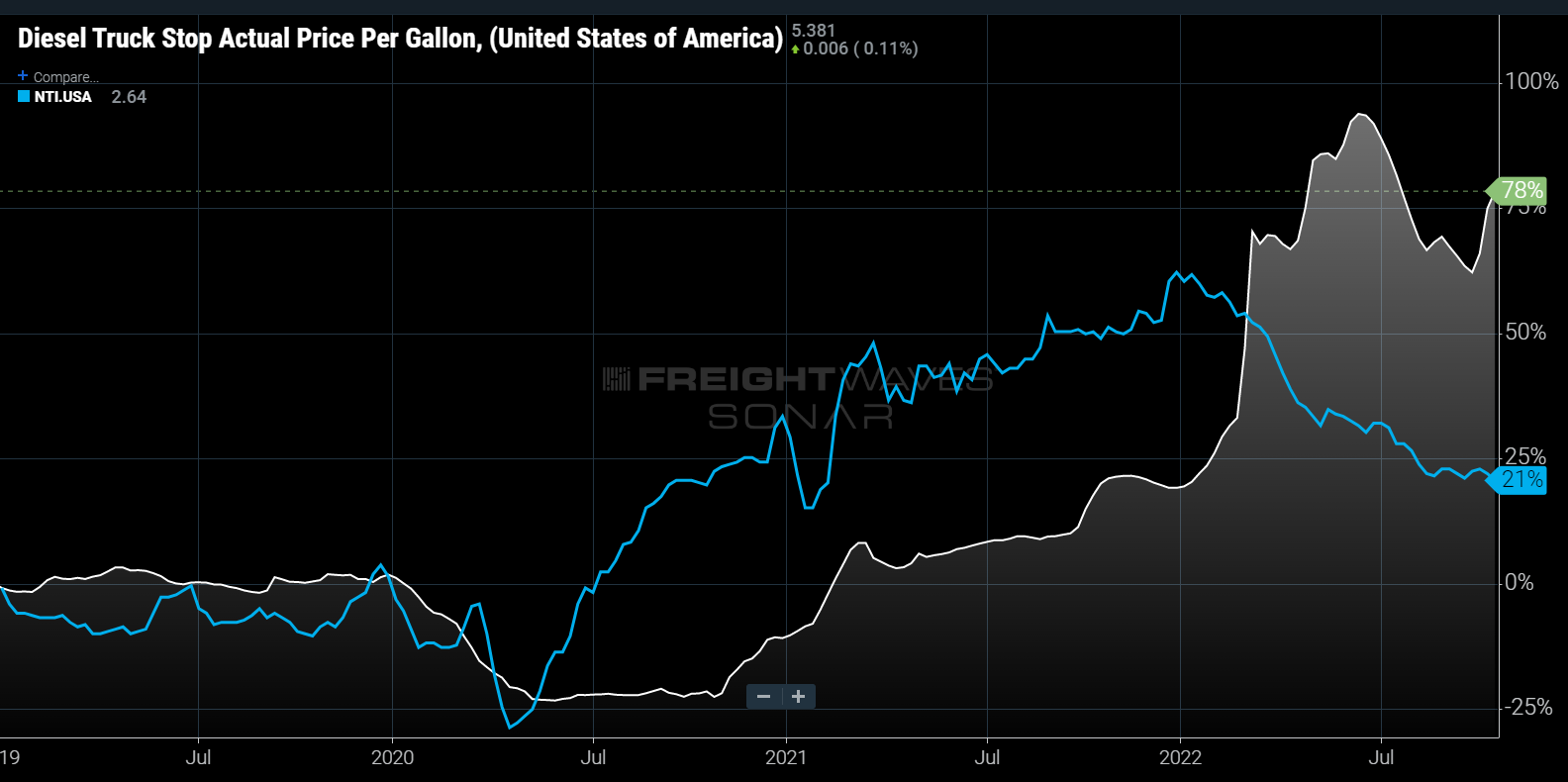

Perhaps the most revealing thing about the collapsing truckload market this spring was its rapid decline as fuel prices skyrocketed. It’s an extremely rare occurrence when spot rates and fuel costs are moving in opposing directions, especially when fuel is increasing.

Spot rates including fuel fell 15% from early March to early May while retail diesel prices (DTS) increased 40%. This movement suggests two things:

- There was a lot of room on carrier operating margins.

- The balance between capacity supply and demand was shifting dramatically from an undersupplied market to an oversupplied one.

Since early May, the average fuel price has fluctuated but is currently about 2% higher than it was at that point. All-inclusive spot rates have fallen another 11% but at a much slower pace. In October, fuel price fluctuation appeared to be having a stronger influence on all-inclusive spot rates.

Demand eroding

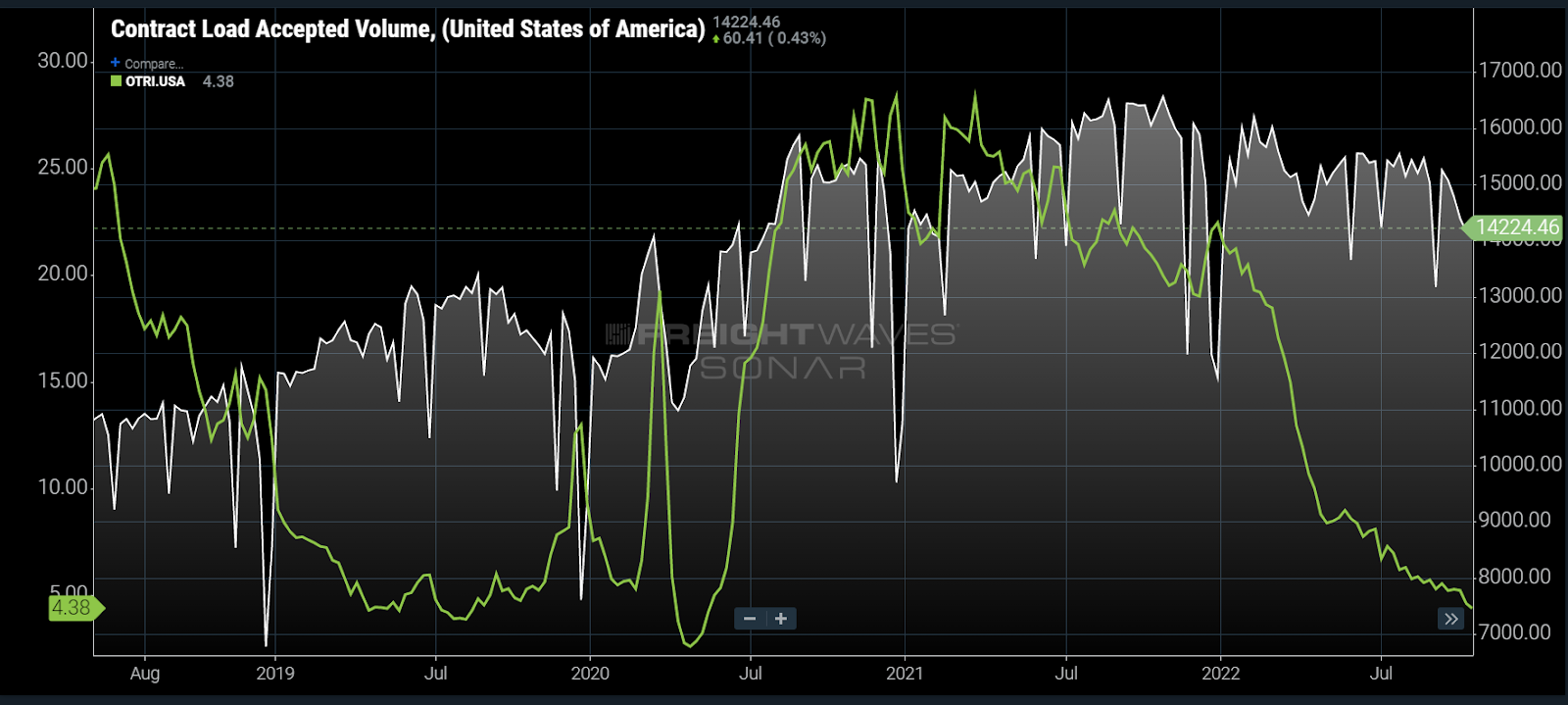

Switching over to the demand side of the equation, accepted tender volumes are about 11% lower than this time last year. Accepted tender volumes, measured by the Contract Load Accepted Volume Index (CLAV), are representative of load volumes being moved under contracted rates.

In an easing environment, carriers accept more loads under contract rates because they have less optionality and network disruption. In 2019 CLAV increased as loads moved from the spot market back under contract and rejection rates fell, suggesting capacity increased to meet demand.

A decline in the CLAV at this point suggests that aggregate demand is falling versus carriers choosing to divert capacity to the spot market. Considering spot rates are offering a significant discount to contract rates, this makes sense.

The CLAV dropped about 5% since Sept. 26, suggesting that demand still has room to fall. In a recent survey by FreightWaves Research, carriers all seem to agree that the worst is yet to come. Q4, normally a strong period for high margin freight, is projected to be muted.

Large carriers taking a hit

Knight-Swift (NYSE:KNX), the nation’s largest for-hire carrier, missed expectations in Q3 and provided weaker near-term guidance for the truckload segment, with CEO Dave Jackson suggesting “meaningful, attractive acquisition opportunities over the next few quarters.” This implies Jackson expects many smaller fleets to be struggling over the next six months.

The 2019 market is a baseline for many in terms of establishing a low-end environment for freight. Demand was flat and spot rates were deflationary. CLAV is about 14% higher and NTIL about 22% higher in relation to October values that year.

Considering costs have inflated for carriers since that time, we can assume the theoretical floor for spot rates to be some percentage above the 2019 level. If spot rates were to fall to or below this level, it will be safe to assume carriers are operating at a loss.

The reality is that spot rates for many carriers are probably already at or below their break-even point. The massive deceleration in decline suggests margins have already eroded to the single digits.

The 10% fuel cost increase in October appears to be having an influence on spot rates, unlike earlier in the year. This is further evidence that margins are already thin to nonexistent.

Diluting the spot market

The CLAV suggests larger contract-heavy fleets are going to need the spot market to fill increasing gaps in their networks, further diluting the pool of available freight for small carriers and owner-operators.

Large, contract-heavy carriers still have some buffer as long-term rates are still providing strong returns, evidenced by Knight Swift’s 81% operating ratio (19% operating margin) in Q3. This gives the company room to handle more losses on the spot market, which could accelerate the spot rate decline.

While the break-even point for many carriers has potentially already been reached, the market is still a great distance from hitting its lower limit. All eyes will be on January as seasonal pressures may return to truly test carrier resolve.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

Steven manson

Also what really pisses me off…..JBHunt bids on a reefer contract from Amazon then contracts us out to do the run with our reefers……so instead of giving us the contract outright they let a mega take the contract WHO DOESNT HAVE REEFERS (they have inttermodel reefer but not dry van style reeferss) and keep a percentage thus depriving our company the true profit

Steven manson

I will work 2 fast food jobs before I ever work for a mega carrier like swift and I know a LOT of truckers feel the same way. The place I’m at now is small but they really do take care of us and I’ve been here 2 years. If mega buys us I’m isubmitting 2 week notice the day it’s mentioned. Did it before when swift bought dick Simon, back on 2000. I’ll do it again

TODD Reeves

Be truthful for once. How many carriers have been forced out of business due to fed regulations? Print those numbers to save credibility to your website. We have been at the bottom for some time now. At least once a week another trucking company closes the doors and lays off drivers and mechanics, administrative personnel. Another crushing blow to that local economy.

Colby

Good Information. Preparing for this.