One financial metric in the CPG world that stands out to me is AB InBev’s net debt-to-EBITDA ratio: 4.8x. The company has been highly leveraged since its acquisition of SABMiller in 2016 when its debt topped $100 billion (net debt was $82.7 billion at the end of 2020) and the pandemic hurt the company’s profitability metrics that are usually compared to debt load. In this edition of The Stockout, CPG-focused newsletter, I discuss the implications for other CPG companies.

Bud does better when consumers are out and about.

A 4.8x net debt-to-EBITDA ratio at the end of last year is a heavy debt load even for a company that produces fairly noncyclical consumer products. The pandemic helped the results of some CPG companies and hurt the results of others. Similar to Coca-Cola, the company’s sales of packaged beverages for in-home consumption (a segment that is more competitive with smaller companies) didn’t make up for the loss of more desirable on-premises revenue. As a result, the company’s 2020 EBITDA declined 12.9% y/y amid a 3.7% y/y total revenue decline and a 382 basis-point margin contraction to a still-strong 36.9%. It’s worth noting that EBITDA declined only 1.1% y/y in the 2H20, a stark contrast to the 24.7% y/y decline in EBITDA in 1H20. That suggests that EBITDA will be up nicely in the first half of this year amid less severe restrictions.

AB InBev has lots of debt, but very little of it matures the next three years.

(Source: AB InBev Investor Relations)

The company’s debt load could have implications for its own corporate strategy and also impact other CPG companies.

I highlight the company’s debt load not because I am concerned about the company’s ability to service its debt — in fact, it has made progress on reducing its near-term maturities as shown above and has $24 billion in total liquidity, including $15.3 billion in cash. Rather, I think the company’s debt balance has implications for other CPG companies and its strategy. The company has made paying down debt a key objective (although it declined to say how quickly it would de-lever to 3.0x). Many of the questions on its latest analyst call focused on debt, including one analyst question about whether the company is considering cutting its dividend. In response to the dividend question, management said that it wouldn’t give any guidance on future dividends beyond the current fiscal year given the fluidity of the current situation. I thought that was a weak response since managements typically like to be emphatic that they will not cut their dividend in the future. With those thoughts in mind, it stands to reason that it is less likely that the company will be as acquisitive as it has been in the past and may divest underperforming brands, which the company says is always on the table. The company may find other cash-generation steps that it can take, such as licensing brands that it owns. Another example of a cash-raising action has been the recent divestiture of a 49.9% minority interest in the U.S. packaging operations in a partnership with Apollo Global Management.

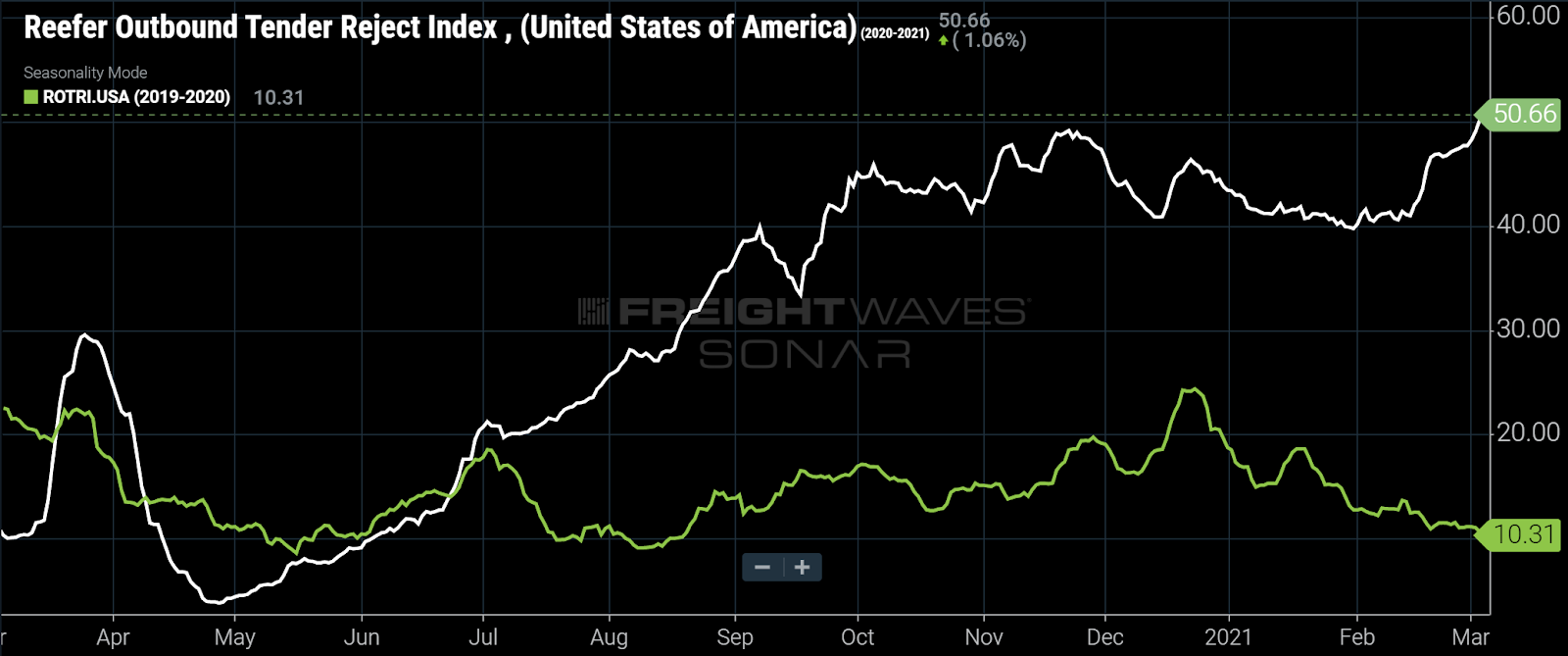

What a difference a year makes. Reefer carriers are able to be far more selective than they had been one year ago. They are now rejecting 50% of tendered loads; last year at this time it was 10%. Every brewer has different service requirements but in general, the temperature requirements for long-haul beer loads need to be kept to about 50-60 degrees. There may be no temperature requirements for short-haul or overnight loads.

(Chart: FreightWaves SONAR. The white line shows reefer tender rejections during the past year (2020-2021), compared to the green line which shows the year prior(2019-2020)).

AB InBev’s comments highlight rising input costs that it is facing as well.

Like most other CPG companies, AB InBev will be facing higher costs for several items in 2021. The company called out corn and barley as the crops having the biggest impact on costs this year. In addition, the company expects to face rising highway costs despite being able to mitigate a portion of that impact by running about 40%-50% of its loads on a dedicated company-owned truck fleet. It has also incurred unusual costs associated with the aluminum can shortage, which required the company to import cans from Mexico to the U.S. That comes in contrast to the company’s typical supply chains that involve production in locations near the locations where products are consumed.

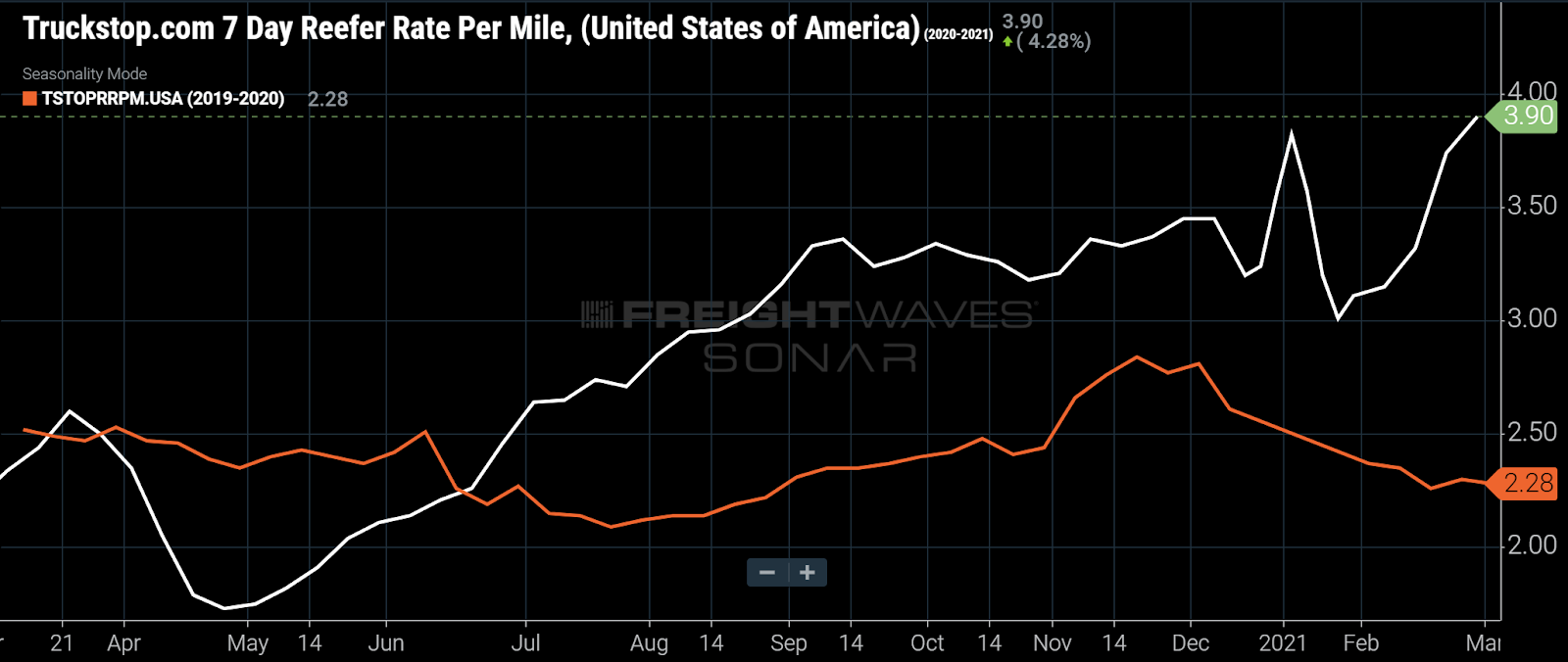

With a tighter market comes higher rates. AB InBev told investors last week to expect pressure from rising transportation costs in addition to rising costs for agricultural inputs. That seems like a certainty. Reefer spot rates from Truckstop.com are up 71% y/y, which should translate to higher contractual transportation rates when annual contracts renew.

(Chart: FreightWaves SONAR. The white line shows reefer spot rates during the past year (2020-2021), compared to the orange line which shows the year prior(2019-2020)).

A Corona controversy that doesn’t involve masks or social distancing.

While I’m on the topic of ABInbev, one of the most interesting topics that has arisen lately is the lawsuit over Corona Hard Seltzer. At dispute is whether Constellation Brands violated a brand licensing agreement with AB InBev (which owns Grupo Modelo) when it launched Corona Hard Seltzer. Constellation has a perpetual license to produce Corona beer in Mexico and market it to U.S. consumers. However, AB InBev says the licensing agreement only allows Constellation to market Corona beer and Corona Hard Seltzer is not beer. Of course, AB InBev doesn’t want Constellation to do that because it directly competes with its own products like Bud Light Seltzer and could be a big deal because seltzer is among the fastest-growing categories of alcoholic beverages. I’m not sure what the relevant precedent is, but if it hinges on whether hard seltzer is beer — I agree with AB InBev/Grupo Modelo that it’s not beer if it’s not made with barley, malt and hops. In any event, I think this is an important heads-up to other CPG companies to spell out agreements clearly for the usage of brands in future licensing agreements.

What do you think Bud will do to reduce its debt? What’s your take on whether Constellation has the right to market Corona Hard Seltzer? Let me know at mbaudendistel@freightwaves.com.

If this was forwarded to you and would like to receive this newsletter, please join us here: https://web.freightwaves.com/thestockout

Happy consuming,

Mike