After several quarters of record financial performances, analysts believe the end of the upcycle for transportation providers is in sight. While carriers may post one more record or near-record result in the 2022 third quarter, the freight cycle is on the downside, meaning earnings results are poised to move lower.

“We are incrementally cautious. Our checks indicate freight activity was seasonally weak through late-September, with limited indication of holiday demand to-date,” said Todd Fowler, transportation equity research analyst at KeyBanc (NYSE: KEY), in a recent note to clients. “Further, with imports decelerating, inventories normalizing and spot below contract rates, we now see volume and pricing weakness into 2023.”

He reeled in earnings-per-share estimates for the truckload and multimodal (including intermodal) providers he follows. Third-quarter estimates were reduced slightly with fourth-quarter and full-year 2023 numbers being cut by mid-single-digit percentages on average. He also downgraded ratings on J.B. Hunt (NASDAQ: JBHT) and Schneider National (NYSE: SNDR) to “sector weight” to “reflect lower intermodal volume and pricing assumptions.”

Fundamentals weaken to close Q3

Container imports to the nation’s 10 biggest ports were flat year over year (y/y) in August, the fifth-highest month all time for loaded inbound twenty-foot equivalent units, according to The McCown Report. Inbound TEUs remained at high levels throughout the summer, up 1.5% y/y on tough comps in the three-month period ended in August. Many shippers reportedly pulled forward merchandise earlier in the calendar to avoid the potential pitfalls that were commonplace in the supply chain during the 2021 peak season.

This could mean that trucking will still see a modest peak season as an abundance of merchandise is in domestic warehouses already and will still be moved throughout the holiday season, assuming interest rate hikes and inflation don’t dent consumer spend. However, the outlook beyond 2022 looks less promising.

Container shipping lines have canceled roughly 60 sailings from Asia to the U.S. for October and spot rates from Asia to the West Coast have fallen by more than 50% since early August (down roughly 30% from Shanghai to New York). The National Retail Federation’s latest forecast called for inbound TEUs to decline by 3% y/y in September, 9.4% y/y in October, 4.9% y/y in November and 6.1% y/y in December. The declines are expected to extend into 2023 as well.

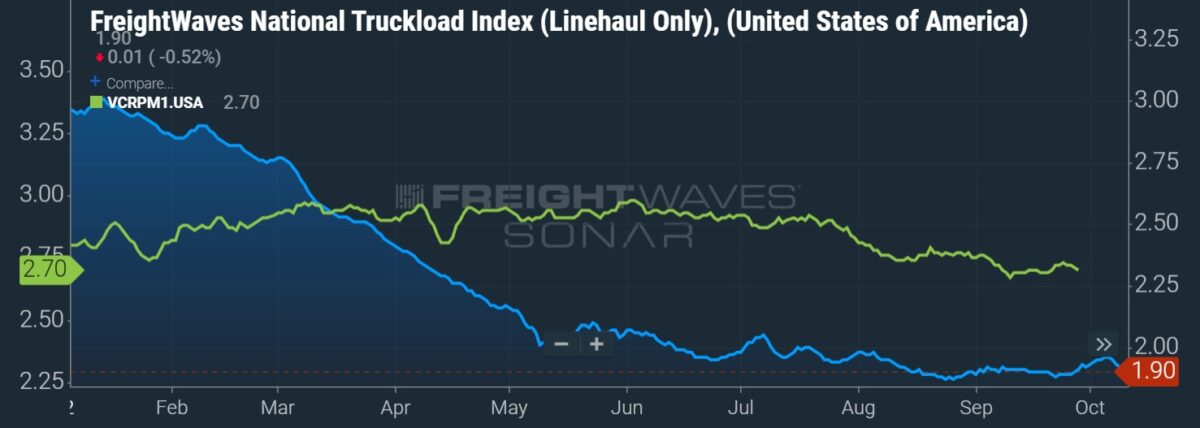

Late-September deceleration was notable in responses compiled from a supply chain survey.

The Logistics Managers’ Index showed sentiment from respondents around transportation metrics was much weaker in the last 15 days of the month. The view on capacity was 9.2 percentage points higher at 76.9 and 14 points weaker on pricing at 36.8. A reading above 50 indicates expansion while one below 50 indicates contraction.

Morgan Stanley shakes up estimates, remains below consensus

Morgan Stanley (NYSE: MS) analyst Ravi Shanker’s estimate changes heading into earnings season were more mixed, noting volumes declined sequentially from the second to third quarters but “pricing looks safe and cost inflation is mostly manageable.”

He slightly raised estimates for the railroads he follows given decent volumes and a modest sequential uptick in service metrics. He took up numbers for J.B. Hunt and C.H. Robinson (NASDAQ: CHRW) by nearly 10% in the third quarter.

He said brokerages should see another quarter of decent results as they have been buying capacity at lower spot rates and selling it at higher, previously negotiated contractual rates. He did caution that gross revenue could be constrained by spot market weakness, which likely weighed on volumes and rates not tied to contracts. Also, he sees brokers with forwarding operations, like C.H. Robinson, beginning to struggle as air and ocean rates fall from record levels established during the pandemic.

Estimate revisions for the TL and less-than-truckload carriers were mixed, with nearly every change amounting to less than 1% for full-year 2022.

“Risks to 3Q earnings are not as high as we thought three months ago but sentiment will remain muted as 2023 headwinds seem clearer than tailwinds,” Shanker advised clients. Overall, his estimates for the 20-plus companies he follows are at or below consensus for 2022.

Inventory overhang to carry into 2023

Separate research reports published Monday by Morgan Stanley showed high inventories across multiple sectors continue to be a headwind to freight demand. A quarterly survey of shippers showed net ordering dropped 40% y/y to the lowest level ever recorded in the survey’s 12-year history. The rate of decline was also faster than in the downturns of 2019 and 2016.

The firm said the median goods-producing company saw inventory growth outpace sales growth by 1,900 basis points in the recent quarter. The metric was wider at 2,600 bps when measuring changes in the retail sectors (hard line, broad line and food).

“Almost half of respondents say that their inventory is higher and ordering is lower going forward — which firmly indicated an over-inventoried/de-stocking condition,” the report read.

Only 23% of shippers indicated a desire to increase inventories, which was “not too far off long-term levels,” and 75% said they expect their inventory to normalize between now and the first half of next year.

Fowler’s timeline for inventory destocking is potentially a little longer. “The current destocking cycle began after the March 2022 inflection (total inventory growth outpaced total sales growth) and is currently 5 months compared to the average destocking cycle of 17 months.”

Morgan Stanley believes the excess inventory taken in by the retail sector during the later stages of the pandemic will be a catalyst for lower inflation throughout 2023. Large big-box retailers have already signaled intentions to be aggressive with holiday promotions, and Amazon (NASDAQ: AMZN) just held another Prime Day-like event.

Susquehanna reins in expectations, TLs to see 20% y/y EPS dip next year

Susquehanna Financial Group analyst Bascome Majors lowered estimates at the end of September for the transportation and logistics companies he covers. He made minor revisions lower for 2022 and took 2023 numbers down by mid-single-digit percentages.

“As 3Q draws to a close and earnings season approaches, we’re nearing the point where the proverbial rubber meets the road, connecting freight market indicators that peaked in 1H and deteriorated broadly through 3Q with bottom-line results from the trucking and logistics companies levered to those real-time metrics,” Majors told investors.

He said “sub-seasonal deterioration” in TL volumes during the third quarter provided a catalyst to reduce expectations for the rest of the year. He believes pure-play asset-based TL carriers will see earnings per share fall 20% y/y during 2023.

Majors said declining fuel prices and tonnage will present headwinds to LTL earnings next year. Fuel surcharges are applied to LTL base rates on a sliding scale, allowing carriers to see outsize EPS growth in periods of high diesel prices. However, he’s forecasting EPS to decline by only single-digit percentages for the group next year on the expectation that carriers will be able to retain recent pricing gains, benefit from a stable industrial economy and see incremental improvements from ongoing network efficiency initiatives.

He also took down expectations for intermodal providers in 2023 by high-single digits. Majors said service improvements have yet to materialize even as the railroads continue to add headcount. He believes elevated fuel prices will keep pricing at “inflation-plus” levels but noted the opportunity for modal conversion and higher volumes “narrows against a weakening consumer and lurking recession.”

“Net-net, our view toward the sector is unchanged,” Majors said. “We expect a freight recession to drive earnings declines for most companies we cover in 2023.”

More FreightWaves articles by Todd Maiden

- KAG Logistics expands 3PL platform through Connectrans deal

- Bison Transport acquires 2nd Maine-based carrier

- LTL survey ranks Peninsula No. 1 overall, Old Dominion top national carrier

Container bookings peak one last time before the holiday season

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now