Chart of the Week: Van Outbound Tender Reject Index, Truckstop.com top 100 all-in van rate per mile – USA SONAR: VOTRI.USA, TSTOPVRPM.USA

Tender rejection rate changes typically lead spot rates by several days as the underlying contract market destabilizes in front of the spot market. Currently they are moving in different directions. Why is this happening?

The freight market is going through a lot of changes. The pandemic year capacity crunch has motivated shippers to change their behaviors and find new ways to move goods through their supply chains. The numerous changes have made it increasingly difficult to look at historical patterns and draw actionable conclusions. The most recent casualty of this dynamic shift is the relationship between aggregate tender rejection rates and spot rates. Will this divergence last forever?

The short answer is probably not, but this temporary break in their relationship can also lead to more detailed insight with a little digging. First, a basic understanding of tender data and spot rates is necessary to make any significant conclusions.

Defining tender data and spot rates

Load tenders are electronic requests for capacity submitted by a shipper to a carrier. They are sending a message to a carrier asking for a truck to show up at a given time at a predetermined (contracted) rate. Tender data is based heavily on contracted rate agreements between shippers and carriers, meaning it measures how effective the current contracted pricing is in guaranteeing capacity.

Increasing tender rejections is a sign that carriers either have better (often-meaning better-paying) options or they simply cannot supply a truck at that time because they are in use or too far away. This is an early warning sign for increasing spot market activity and subsequently prices.

Tender rejection rates have been above 20% for over a year now, meaning shippers have grown accustomed to one out of every five load requests being rejected. This is the longest period of time for tender rejection rates being this elevated over the past three years.

The average van spot rates reported by Truckstop.com are a weighted average of their top 100 lanes. This list of lanes is static and does not change over time for the purpose of comparing historical values. Spot rates only measure about 15%-20% of the market in the most volatile lanes.

How the relationship has changed

The primary reasons for the divergence are:

- Increasing contract rates leading to higher rates and more compliance.

- Growth in short haul (loads moving less than 250 miles) as long haul declines.

- Spot freight’s bias toward longer lengths of haul and headhaul lanes.

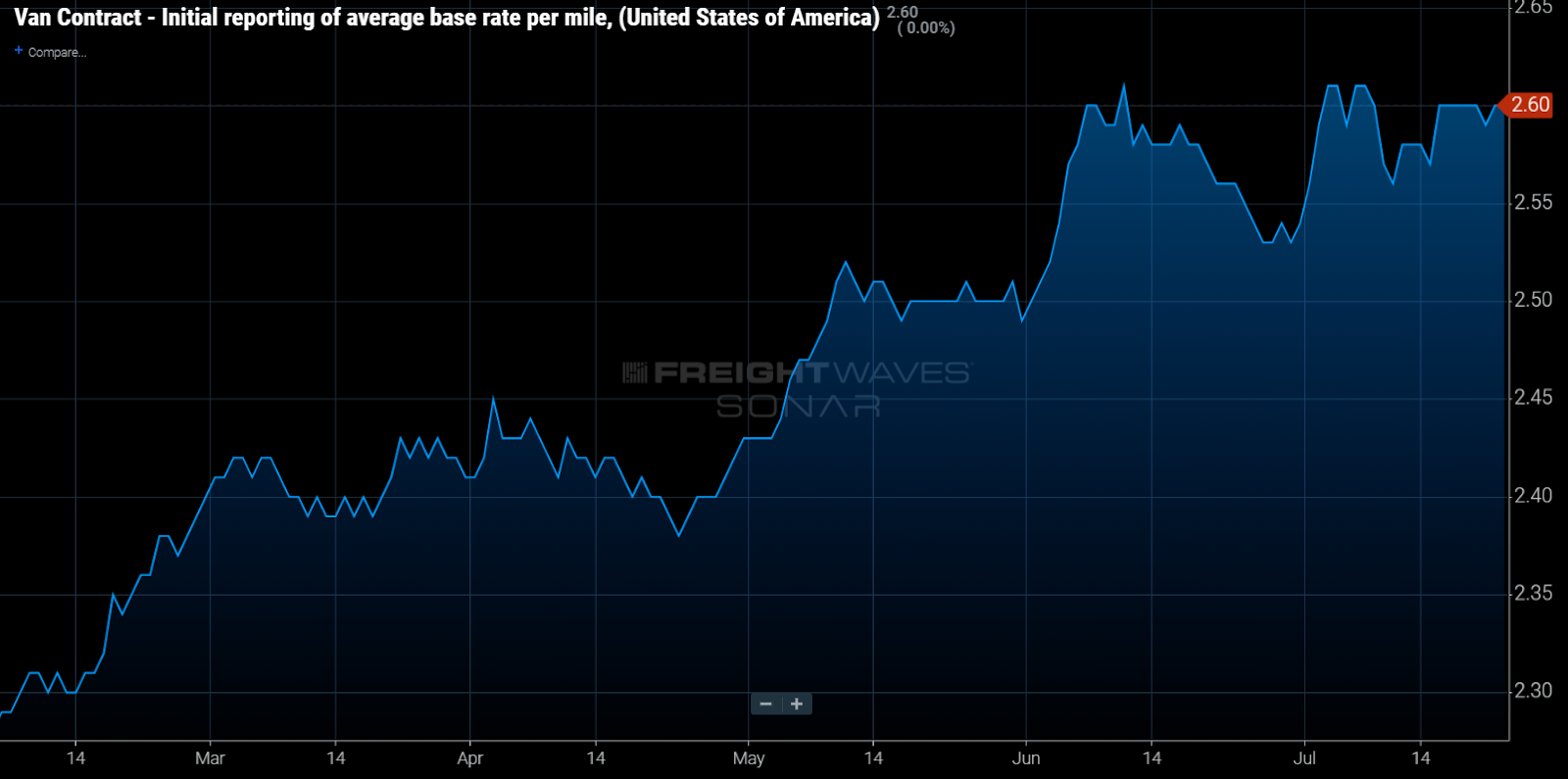

Contract rates on the rise

Typically spot rates increase after tender rejections then contract rates follow as they are normally adjusted on an annual basis. Many shippers are now instituting mini-bids or interim adjustments to contract rates that are set for shorter periods of time such as three months. This means contract rates can move higher faster, providing a new elevated floor for spot rates. So even though the average spot rate has increased, the spread between the contract and spot rate has shrunk.

Increasing contract rates keeps upward pressure on spot rates while also increasing load acceptances. Contract rate growth has stalled over the past two months, but at a much higher level than where they started the year.

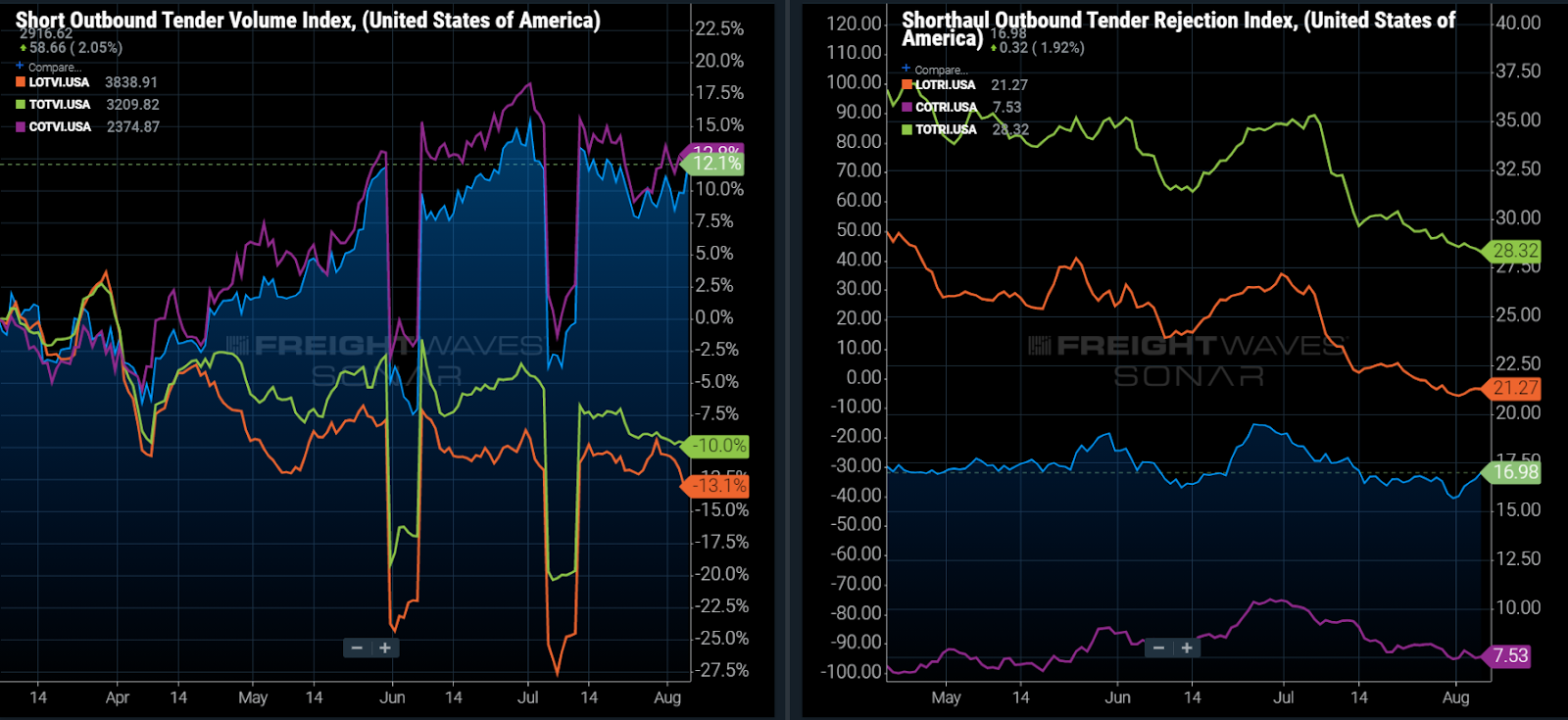

Short haul growth

Possibly the most significant pattern change has been the changing mix in long and short haul freight demand. Shippers have pushed more freight moving less than 250 miles over the past few months while shipping less longer haul freight, an area that the spot market is largely blind to.

Loads moving less than 250 miles are rejected at a much lower rate than loads that move more than a day’s travel away from the origin — the Shorthaul Outbound Tender Rejection Index (SOTRI) was at 17% last week while the Tweener Outbound Tender Rejection Index (TOTRI) was at 28%.

The Short and Local Outbound Tender Volume indices (SOTVI and COTVI) show 12% growth since March, while the Tweener and Long Outbound Tender Volume indices (TOTVI and LOTVI) show over a 10% contraction.

Shorter-length-of-haul loads command a higher rate per mile due to the increased fixed-cost burden on short haul freight. Carriers have a minimum threshold for turning on the truck, and time spent at pickup and delivery has to be accounted for in the rate when the driver is not driving.

Spot freight dichotomy

Most spot freight travels at longer lengths of haul or more than 250 miles from origin to destination but the top 100 lanes for Truckstop.com average around 600 miles with a range between 255 and 2,000 miles. Note the shortest-length-of-haul lane is above what we define as short haul freight, the sector that has been growing for the contracted tenders.

Spot freight is also heavy in headhaul lanes, or lanes that move carriers from heavy outbound markets like Los Angeles into heavily oversupplied markets like Phoenix. As the disparity in volume of headhaul versus backhaul lanes grows, so does the aggregate rate.

Some of the largest volume growth has occurred in headhaul lanes since the end of March while freight moving back into Los Angeles, an extremely active outbound market thanks to surging imports, is showing up on fewer spot boards.

| Lane | Current RPM | 4-month % change in volume |

| Buffalo, NY, to Elizabeth, NJ | $4.10 | 444% |

| Louisville, KY, to Baltimore | $3.79 | 332% |

| Baltimore to Boston | $4.69 | 213% |

| Portland, OR to Los Angeles | $1.15 | -30% |

| Dallas to Los Angeles | $1.56 | -17% |

There are certainly other factors like service and rising fuel costs that also help keep spot prices elevated in extended periods of low capacity. Eventually, rates and volumes will stabilize and the relationship between tender rejections and spot rates will resume. The divergence of the two may be a more interesting signal than when they follow each other. For now, it appears the market is stabilizing from the ground up.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new data sets each week and enhancing the client experience.

To request a SONAR demo, click here.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post • Chicago, IL Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now

Anna

I am now making more than 350 dollars per day by working online from home without investing any money.

Join this link posting job now and start earning without investing or selling anything.

visit here………… www.jobs70.com

Stephen Webster

The higher freight rates mean that companies and owner ops can afford to spend more money to keep trucks and trailers well maintained. Also drivers are refusing to push the rules as wage rates are up 20 percent with many companies compared to 2 years ago. This means truck drivers can make a living running legal or close to legal. The only other thing is we need more room to extend our day for transport drivers that are getting at least 22 op U a per hour plus overtime after 10 hours or 8 hours driving per day to a 16 hour window providing the trucking company agrees to supply a break of 10, hours off next day. The so called truck shortage means that trucking companies are willing to work with sick truck drivers like me and provide part-time work as my health allows.