Your cash will pile up as the year goes on. More cash is coming next year. Your debt is already low. What will you do with all of this money you’re raking in?

That question is music to the ears of any public company executive, and was the central focus of Tuesday’s conference call of container-ship lessor Danaos Corp (NYSE: DAC).

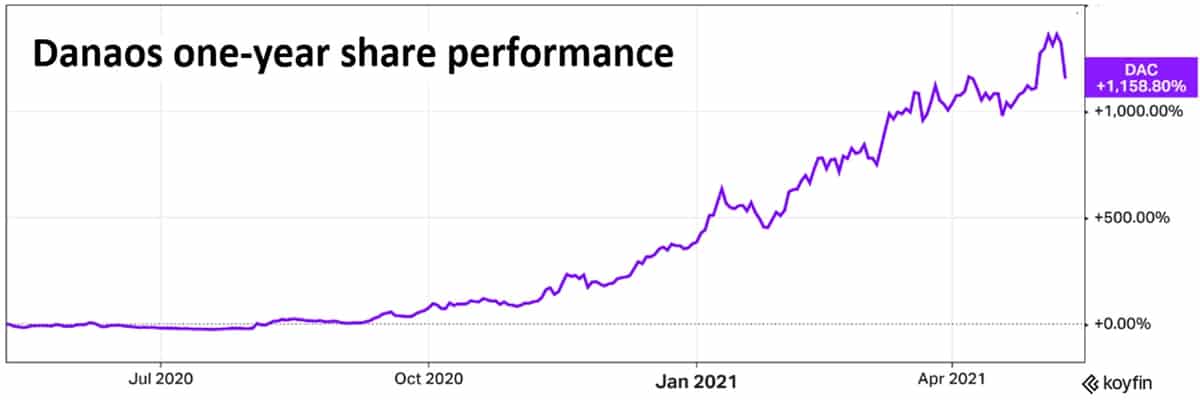

Danaos earns money by leasing ships to liner companies, which are now desperate for any vessel they can get their hands on. Charter rates continue to reach new heights. Even after Tuesday’s broader market plunge, Danaos’ stock is up 1,159% year-on-year — well beyond annual stock gains of any other U.S.-listed shipowner.

The tighter vessel supply is versus demand, the better companies like Danaos do and the worse the freight pricing is for U.S. importers and exporters of containerized goods. Unfortunately for cargo shippers, the market tide continues to turn against them and in favor of companies like Danaos.

As for all the cash coming in, Danaos CEO John Coustas said, “We are building a war chest.”

Ship shortage through 2022

“The dramatic turnaround and strength of the market that we experienced in the beginning of the year continues unabated, if not stronger,” said Coustas. “Disruptions in the supply chain will likely not normalize before the end of the year,” he added.

“On the chartering front, every fixture we concluded was done at a new record level,” he said. And it’s not just pricing that’s soaring, it’s the duration of the leases. “For vessels above 4,000 TEU [twenty-foot equivalent units], we are discussing four-year-plus durations. For smaller vessels, two to three years.”

Cargo shippers should not expect newly built capacity to help the supply-demand balance in 2022. In fact, just the opposite, said Coustas. There has been heavy ordering of new container ships in recent months, but these won’t deliver until 2023-2024.

Next year “will be very lean in terms of deliveries,” said Coustas. “Actually, [there will be] considerably less [deliveries] than in 2021. So, the shortage in the charter market is going to continue for some time.”

Furthermore, the fleet growth dilemma faced by Danaos confirms that there are not as many orders for 2023-24 delivery as there could have been. Orders are being held back by uncertainty over future environmental rules — yet another negative for cargo shippers hoping for more future vessel capacity.

Regulatory uncertainty curbs orders

“Our strategy relies on the growth of the company, and we believe there are going to be significant investments in the future,” affirmed Coustas.

“We are going to have much more clarity on the actual environmental direction of shipping towards the end of this year, and this is really going to drive the investment. When there is no clarity, the best strategy is to make a war chest and be ready to fight and face whatever situation arises.

“We have two fronts. One is the IMO [International Maritime Organization] with the EEXI [ship efficiency regulations] discussion. The other is the European Community, which wants to impose the ETS [emissions trading system] on shipping. We have no clue what that is going to look like.”

There are also major questions on the use of liquefied natural gas (LNG) for container-ship fuel. “The European Union is not considering LNG as a transitory fuel and has stopped funding LNG-related projects. And the World Bank has said that LNG is a carbon-based fuel and we should try to concentrate on fully decarbonized solutions,” said Coustas.

“Today, the company is having and will continue to have significant growth in income purely by exploiting the market and the vessels in the best possible manner. When the time is right we will try to exploit new technology to put the company in a growth era on the basis of a decarbonized future,” he said.

Danaos CFO Evangelos Chatzis added, “The priority is going to be growth with assets that are at the forefront of the environmental new vessels of the future.”

No special dividend

It may seem odd that investors would want even more from a company whose stock appreciated 1,159% over the past year, but of course they do, whether via share buybacks or dividends.

While management maintained that the current net asset value of its stock is $90.90 per share (compared to the Tuesday closing price of $56.52), buybacks were not discussed on the call.

Danaos did initiate a 50-cent-per-share quarterly dividend, but tempered any expectations that dividends would ratchet up with earnings. “We don’t want to position Danaos as a yield company,” said Coustas. “What we have delivered to our shareholders is growth in profits.

“To be honest, we are giving a dividend purely because we want to enlarge our shareholder base to investors who require a dividend to own the shares. We believe we are very well positioned to invest this war chest and that’s the reason we are building it. We have no intention of just distributing the money [via dividends].”

In some cases, during extremely frothy shipping markets, shipowners distribute a one-time so-called “special dividend.” Asked about this, Coustas firmly stated, “There is no special dividend.”

Cyclicality risk

One argument against paying out big dividends during market peaks is that it often comes back to haunt shipping companies when markets inevitably turn south. As Evercore Senior Managing Director Mark Freidman said during a ship finance conference in 2015: “Why am I skeptical about high dividends? Because I’ve seen a good chunk of the industry go bankrupt through the cycles.”

Danaos itself paid out prodigious dividends during the mid-2000s super cycle. In 2005, when it was private, it paid $244.6 million in dividends (199% of net income). After going public in late 2006, it paid out $97.4 million in 2007 (45% of net income) and $101.5 million in 2008 (88% of net income) before halting payouts due to deteriorating market conditions.

In the wake of the global financial crisis, Danaos had to start laying up ships beginning in 2011. The declining value of its vessels left it unable to meet collateral ratios on its loans, requiring banks to waive covenants. Its charterer ZIM (NYSE: ZIM) restructured in 2014, with Danaos taking notes and equity as part of the deal. Charterer HMM restructured in 2016, also giving Danaos notes in return for lease restructuring. Hanjin collapsed that year, defaulting on its charters to Danaos.

Danaos finally concluded a comprehensive out-of-court restructuring of its debt in 2018, with certain lenders receiving 47.5% of the company’s equity.

The company’s troubles over the past decade highlight the extent of the company’s turnaround — and of management’s personal experience with shipping cyclicality.

As Coustas said in response to a question on charter-backed newbuilding negotiations, “I’m not here to commit to single-digit equity returns for 10 years. In 10 years, if you think about where we were in 2010 and where we are in 2020, a hell of a lot of things can happen in between.”

More to come after Q1

Danaos reported net income of $296.8 million for Q1 2021 compared to $29.1 million in Q1 2020. Adjusted net income increased 74% year on year, to $58 million.

Chatzis emphasized, “The results for the first quarter do not fully capture the significant improvement of market fundamentals.” Many of the recently chartered ships won’t begin their new, much-higher-priced employment until the second and third quarters.

In addition, the notes from the ZIM and HMM restructurings are about to be redeemed early and converted to cash, with $76.2 million expected from these sources in Q2 2021.

Danaos’ equity stake in ZIM is now valued at around $400 million. Danaos will ultimately sell its ZIM stake after the lockup expires. “We are looking to monetize our nonoperating assets,” said Coustas. “The ZIM shares, at some stage, will form part of our war chest.”

Click for more articles by Greg Miller

Related articles:

Freight Fraud Symposium

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Rock & Roll Hall of Fame • Cleveland, OH Register NowPast the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post Office • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now

Brandon Musler

Re: “Buybacks were not discussed on the call, but management estimated the current net asset value of their stock was $90.90 per share. Given that the stock is currently trading at $56.52 per share, that implicitly answers the buyback question (i.e., no).” I must be missing something here. If I go to a store and see something I want that is worth over $90 but priced at $56.52…or for a 38% discount…that increases the chance I will buy it. So, war chest aside, why would management’s answer to the question a flat “no?”

Greg Miller, Senior Editor

You’re absolutely right. Mental lapse on my part. That section has been changed. Much appreciated for pointing out.