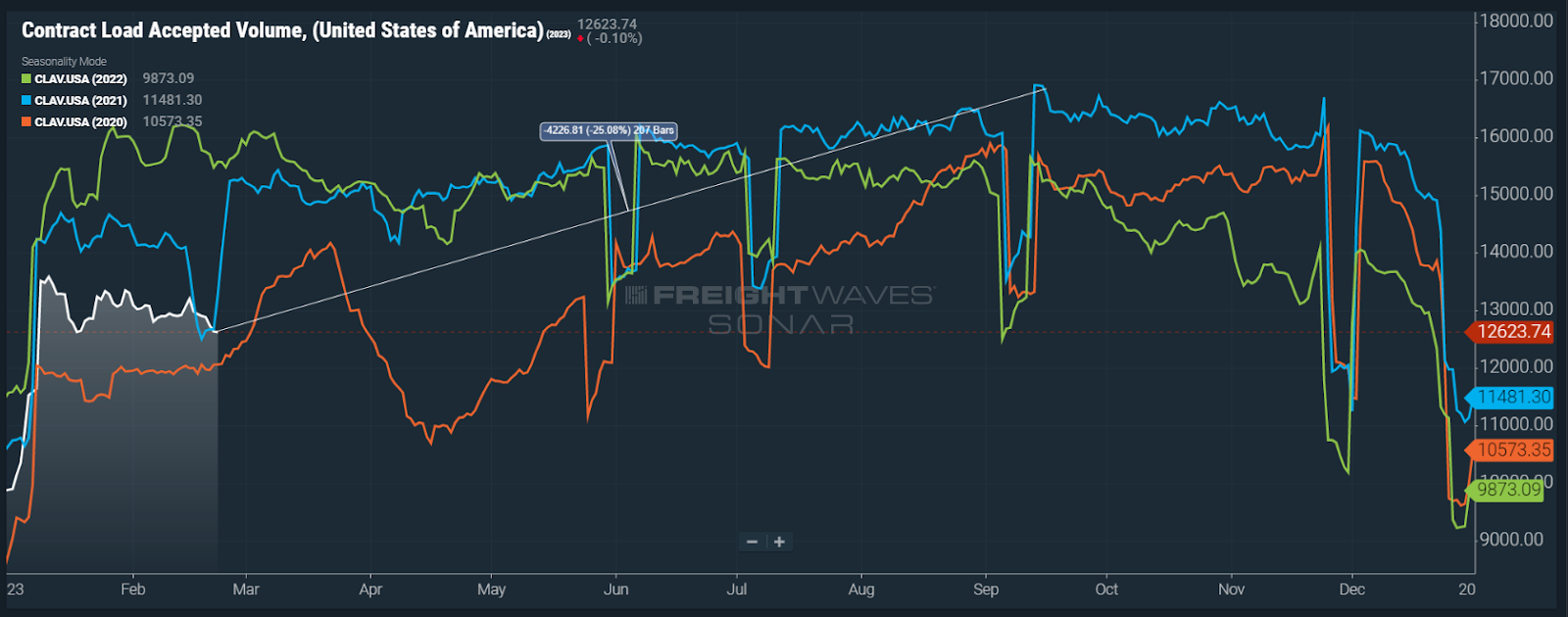

Chart of the Week: Contract Load Accepted Volume Index – USA SONAR: CLAV.USA

The Contract Load Accepted Volume Index (CLAV), which measures accepted truckload tender volumes, is 25% lower than the peak values in 2021. With rejected tenders being near historic highs at that point, we can assume this was the limit to the amount of volume carriers could handle.

Considering exits are just now starting to outpace entrants, according to recent Federal Motor Carrier Safety Administration data, 25% may be a smidge low after a year of new authorizations. How long will capacity take to be more in line with demand?

No demand

Even with demand remaining relatively unpredictable, there are no reasons to expect a significant stimulus event in the near future. The Fed is still fighting inflation with interest rate increases and has signaled that it has no reason to think its job is done.

The only macroeconomic indicators with any real strength in them have been the jobs market and revolving credit (credit card debt) dollar amounts, the latter of which being a negative sign for future consumption.

There are far more reasons to expect weakening demand rather than strengthening in 2023, which means trucking operators have to play a waiting game as to when some form of pricing leverage will return. That being said, freight demand is far more fickle than capacity shifts and needs to be monitored more closely even though there appears to be a significant buffer.

Capacity changes slowly

The supply side of the trucking transportation market is very slow to move, historically only changing around 1% per month. If we apply that rate forward, it will be 2025 before capacity and demand are in alignment.

The decision process to enter the market is a long one for an owner-operator. Many contemplate the move for years before pulling the trigger on purchasing a truck. Large fleets deliberate for months whether to expand their operations. Then it takes another nine months (longer during COVID) to receive the truck.

Because of the lengthy and costly process to expand capacity, the decision to exit or park trucks is also extended. This is a life-altering decision for an owner-operator and deliberation should not be quick. From a large fleet perspective, it is potentially missing growth opportunities if it misjudges the market — this is possibly worse than having too many trucks available for long-term viability.

Capacity does not have to contract completely for rates to rise

Consumption and demand do not have the same constraints. Truckload demand flexes up and down 5% regularly from month to month, even before COVID. From April to September 2020, the CLAV increased 48% out of the economy’s initial lockdown period.

Accepted tenders were up 15% year over year (y/y) by the end of August. This suggests the for-hire truckload market had about 15% excess capacity available at the beginning of the pandemic in what was a relatively soft environment for trucking.

Even with the decent capacity buffer, seasonal price fluctuations on the spot market and rejection rates were present in 2019 and early 2020. By these standards, we can estimate it will take approximately 10 months before the market has some seasonal behavior if capacity contraction is consistent (it won’t be). But this gives us a decent starting point.

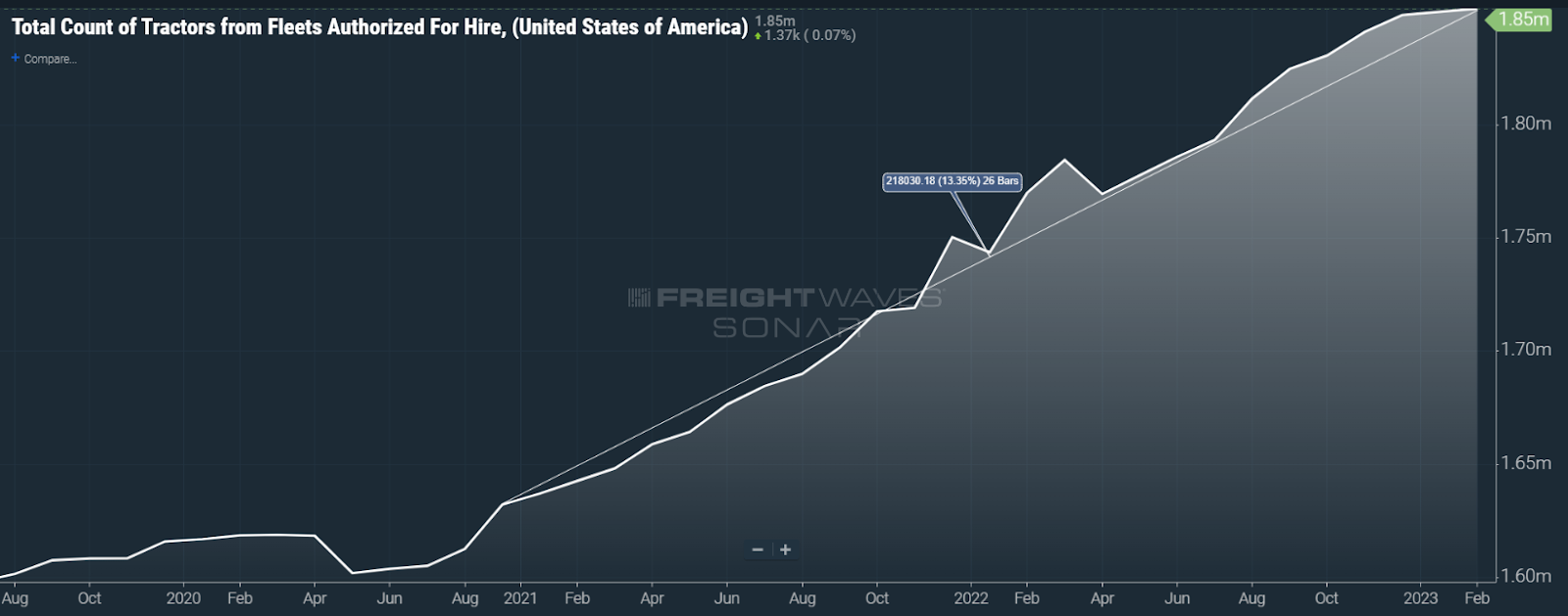

According to the FMCSA, active tractor count growth stalled last month and revocations are now outpacing new authorizations. This data is lagging and it is most likely safe to assume exits are outpacing the new entrants.

Large fleets are handling things differently. Covenant Transport decided to park 600 tractors in Q4 of 2022, leading to a rare y/y operating margin improvement for the sector in the quarter.

Many of the other publicly traded truckload companies posted equipment growth in 2022, but much of that came in the form of acquisitions. Werner added 200 trucks it acquired from the purchase of Baylor Trucking.

Consolidation is a form of capacity reduction in the way it diminishes competition.

How will we know?

Trucking capacity is extremely opaque and difficult to measure. It is also irrelevant without understanding demand. Just because there are enough trucks does not mean they are in the right place at the right time. Capacity needs to exceed demand for this reason.

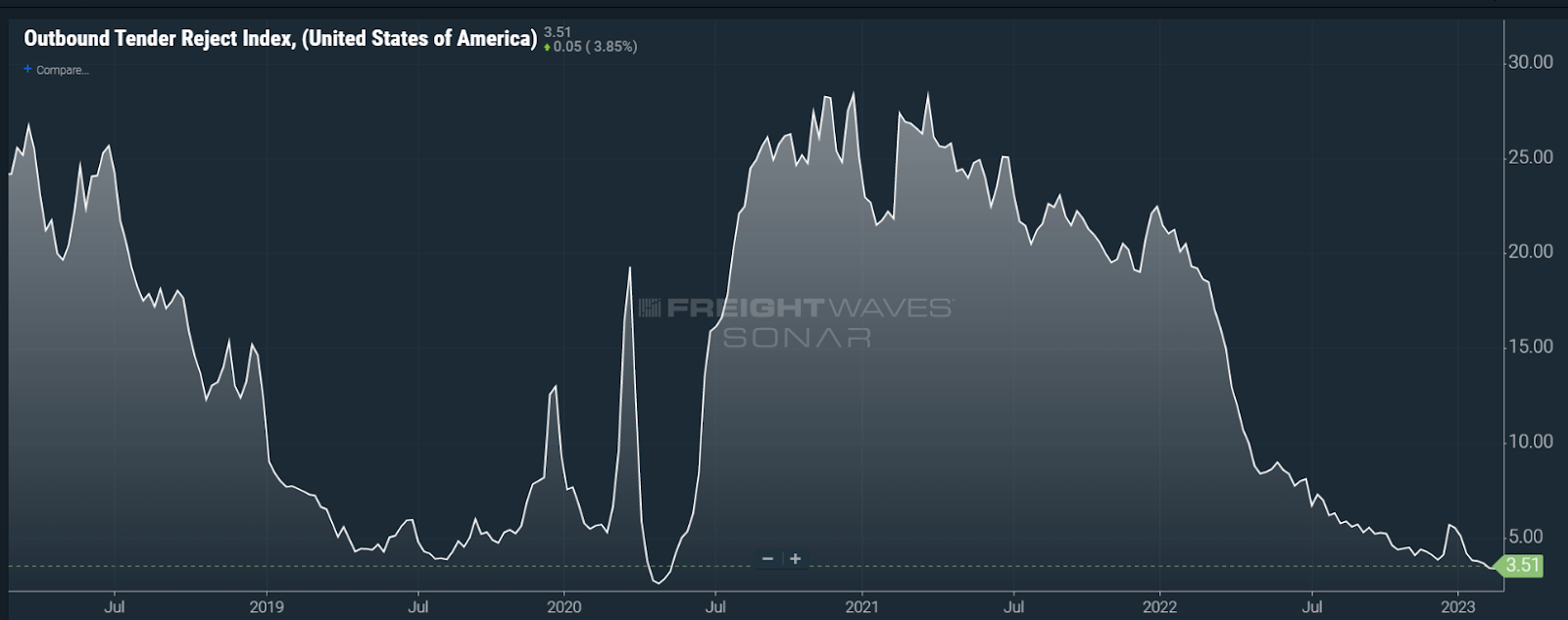

The first sign of capacity correction will be when tender rejections start to climb. Carriers rejecting capacity requests from contracted shippers is a measure of optionality or load availability. Rejection rates above 6% tend to be inflationary, while sub-6% rates correlate with static or deflationary rate conditions. As of now, the national Outbound Tender Rejection Index (OTRI) is hovering around 3.5%, indicating capacity is readily available in aggregate.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

Freight Fraud Symposium

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Supply Chain AI Symposium

Past the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

Future of Rail Symposium

Reshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

Double brokering. AI deepfakes. Identity theft. Freight fraud is an existential threat to the industry. Get ahead of it.

Rock & Roll Hall of Fame • Cleveland, OH Register NowPast the hype. Join operators, founders, and enterprise leaders figuring out how to deploy AI in supply chain.

The Old Post Office • Chicago, IL Register NowReshoring is rewriting freight demand. Join shippers, rail executives, and government officials to shape the next decade.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now

Steve Webster

8 months ago we said we need to limit the number of foreign drivers and set min rates now many companies are going broke in ont canada

Carlos Torres

Completely agree with Dan Chidester’s posting, Latinos are not the biggest problem, because other groups do it as well, but they do add significantly to the problem far more than others I say this as a Latino that I am and I hear and see this every day. Latinos are one of the fastest-growing populations in this industry because they are led to believe this is the fastest and easiest way to make a lot of money until reality hits. I run the northeast and all you see are OOs from the south for weeks on end, especially from Florida the majority running loads for pennies like you mentioned destroying rates and themselves to the point where I can’t negotiate a rate on a load because the brokers well just outright tell you they are firm on their rate and they will find someone that will move that cheap load within minutes, and they are right!

That’s why exits are outpacing new entrants.

What FMCSA should do is control how many new authorities they give out per year, not just give them out as they, please. Or give new applications based on how many exits or revocations there are per year, or Have a waiting period of about a year after you take training or obtain an additional certification on a general knowledge CDL and transportation before getting an authority. Or have a waiting period of at least 3 years before you can apply for an Authority after just obtaining a brand New CDL. An exception would be for a business that manufactures their products and needs transportation to move their own so long they have a transportation safety and compliance department and submit a certification of training. I could keep going, but whos going to listen?

Rich Witzel

Been saying this for over a year. Just because every trucking company wants more drivers, does not mean that there is a driver shortage. The market has too many drivers.

I seen

They drive Fake company trucks too

Dan Chidester

As long as the Govt keeps giving out authority, this is where you get over supply. Latinos know are the biggest problem when it comes to cheap freight. Florida is a great example of cheap trucks. When produce ends in fla, they will destroy the rates all the way north. Its sad because they work so hard, and the TRUCK BROKERS EAT THEM ALIVE.

Jonathan Elliot

Mega carriers and brokers are just being greedy pigs.