Global airfreight weakness has worsened to start 2023 in the face of a global economic slowdown and the lack of a typical bounce around the Chinese New Year holiday. But there is cautious optimism that cross-border trade and demand for freight transportation could pick up in the second half of the year.

The International Air Transport Association (IATA) said last week that air shipment traffic slid 8% last year from record highs in 2021 and was 1.6% less than in 2019, a relatively weak year for the cargo sector. It predicted air cargo volumes will fall further this year to 5.6% below 2019 levels.

Although the global economy is expected to be weaker this year, economists are increasingly confident that many countries can narrowly miss a recession or that any contraction will be short and mild.

Logistics companies say demand from China and other parts of Asia is particularly low, which is influencing the overall figures for global volumes and rates. Trans-atlantic demand, by contrast, is surprisingly robust compared to other trade lanes.

Since late January, global tonnage has declined nearly 10% on a sequential basis and is down 26% compared to the equivalent period a year ago, led by a 47% drop in volume out of Asia, according to WorldACD. Dampened consumer spending due to high inflation and interest rates, along with excess retail inventories, have resulted in export manufacturing contraction in many industrialized countries and slowed trade growth. Also reducing interest in airfreight is the fact that pandemic-induced supply chain disruptions and ocean freight congestion have receded, with ocean rates plunging to below 2019 levels on the trans-pacific westbound trade.

There is “less need for emergency ‘band-aid’ airfreight to make up for stock outs, supply critical process goods and generally compensate for misaligned or deficient inventories,” wrote Bruce Chan, senior logistics analyst at Stifel, in the monthly Baltic Air Freight Index newsletter. Ocean rates are now 10 to 13 times more expensive than air — back to the gap that existed prior to the pandemic — “which means that air cargo is also relatively less attractive,” he added.

Slack demand combined with increased capacity from restored passenger networks, particularly as Asian countries remove COVID travel restrictions, has pushed airfreight rates down by 9%, leaving them 30% lower than a year ago at about $2.90 per kilogram, the TAC Index said in its latest report.

Freight professionals say an earlier Lunar New Year and COVID outbreaks in China, along with consumer belt-tightening in North America and Europe, helped derail the typical rush in airfreight bookings to get goods moved before factories close for the holiday. The official holiday period is now over, but many factories are expected to be closed for weeks because sluggish orders and the infection wave make it unnecessary to reopen quickly.

Comparisons aren’t ideal because China’s Lunar New Year celebration started 10 days later a year ago.

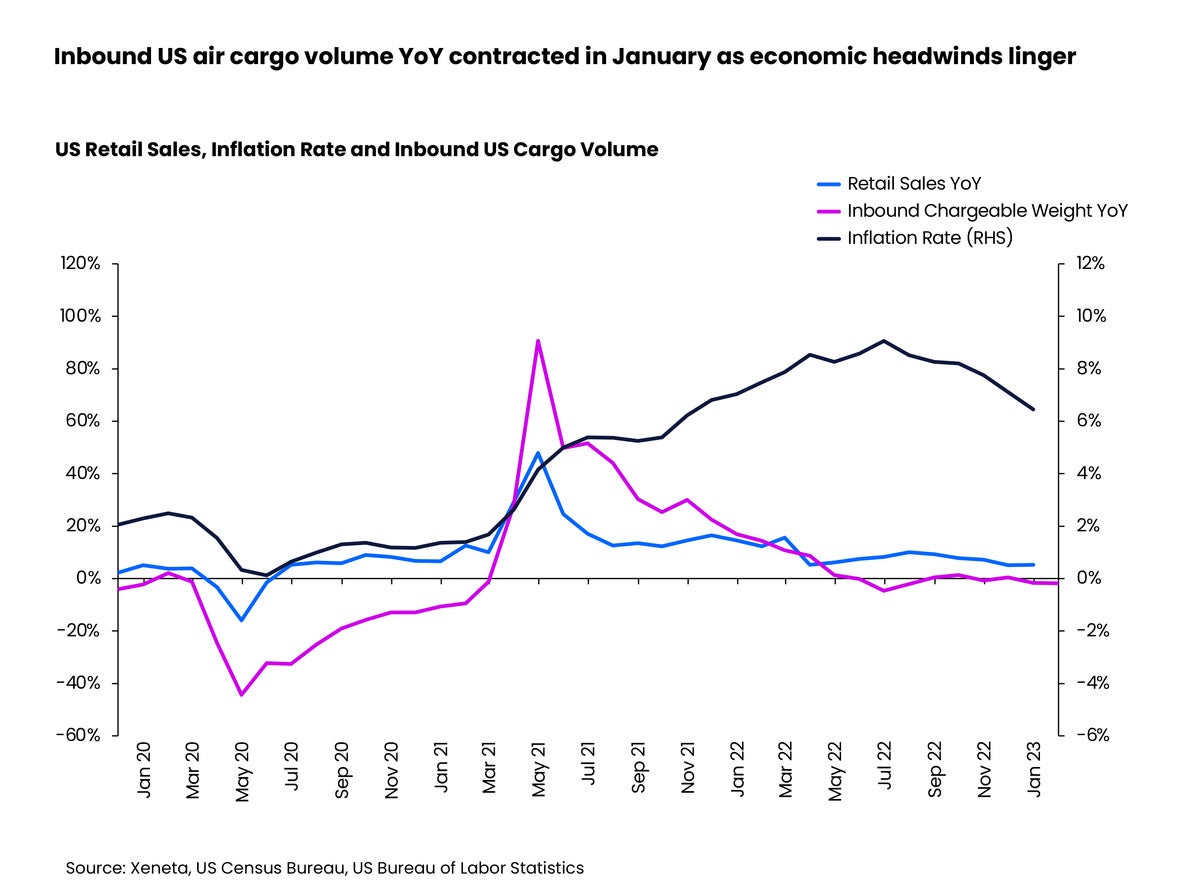

Xeneta, an ocean and air market intelligence firm that crowdsources data on freight transactions, reported that global volumes for the month of January declined 8% from 2022 and were down 10% from the 2019 pre-pandemic benchmark. The airfreight market went into decline following Russia’s invasion of Ukraine last year and hit a trough in the fall, with year-over-year demand contracting 8% for four consecutive months since October.

Global cargo capacity increased 11% last month from a year ago and is now only 2% below 2019 levels.

According to IATA, which has a slower data collection methodology that tends to buttress previous work by market research firms, December air cargo volume fell 15.3% year over year and 7.4% from 2019.

Cheaper shipping

The fall in rates is a two-edged sword for shippers that experienced price spikes during the past two years because of high demand for limited capacity. They are paying less to procure transportation, but likely would trade some higher costs for a better sales environment. Carriers and freight forwarders are still enjoying rates that are about 80% more than in 2019, partly to cover higher costs for jet fuel, labor and longer trips to avoid Russian airspace on Asia-Europe routes.

As in real estate, prices vary by market. In the bigger markets for air freight, such as China to the U.S. and Europe, average prices still remain well above pre-pandemic levels. But in some key markets – such as Vietnam to the U.S. and India to the U.S. – they have already retreated back, according to the latest price data from TAC Index. TAC Index Editor Neil Wilson explained that on major lanes many shippers are still paying higher contract rates from periods when they committed to long-term allocations to guarantee scarce capacity. But in India and Vietnam a much higher proportion of business is ad hoc and conducted at spot rates, which are often much more volatile.

“Indeed, according to the head of global air freight procurement at one major tech company, spot prices have already fallen much further than the indices would suggest out of all major locations in Asia, including Hong Kong and Shanghai,” he wrote.

Spot prices for airfreight could fall further in the spring when passenger airlines begin their summer flying season and add more aircraft to their schedules, further influencing contract rates that are already being renegotiated downward for this year, experts say.

In April 2019, global air cargo capacity increased by 7.1% from the winter, primarily due to more passenger belly space, Xeneta said in a recent blog. The extra capacity usually coincides with lower demand for airfreight during the summer season.

Virgin Atlantic, for example, recently announced it will restart flights between the U.K. and Shanghai, China on May 1, for the first time since 2020, using Boeing 787-9 widebody jets after China reopened its borders to foreign nationals. And Etihad said it will open new routes from Abu Dhabi to Copenhagen and to Düsseldorf, Germany (three times per week), in addition to adding four weekly flights to Frankfurt, Germany – all with 787 Dreamliners.

Brighter second half

One area where airfreight business is holding up is the Europe-North America corridor, where volumes increased 6% in January from the prior year, while overall air imports to the U.S. fell 2%, according to Xeneta.

The International Monetary Fund said the global economic outlook for 2023 is less bad than feared several months ago, with estimated growth of 2.7%. Inflation appears to have peaked in the U.S. and Europe and consumer spending is still relatively strong, with U.S. joblessness at historically low levels and natural gas prices in Europe falling 80% since August. The reopening of China after COVID isolation should also bolster the global economy.

The situation will likely get worse for international freight transportation before it gets better. The National Retail Federation last week said U.S. import volume at major container ports is expected to drop this month to its lowest level since the pandemic three years ago as retailers import less merchandise. The forecast projects a 19.4% drop in container traffic for the first half of the year. Using ocean trade as a proxy for air suggests the drop in air volume, at least to the U.S., could be as severe.

Many logistics executives say they expect a robust second half of the year as inflation eases and retailers finish flushing their old inventory.

Vaughn Moore, CEO of AIT Worldwide, said at the AirCargo 2023 conference in Nashville, Tennessee, on Monday that customers are preparing for increased sales in the third quarter and that there will be a strong peak shipping season in the final few months after the normal surge failed to materialize last year.

Click here for more FreightWaves/American Shipper stories by Eric Kulisch.

RECOMMENDED READING:

Airfreight industry watches for signs of midyear recovery