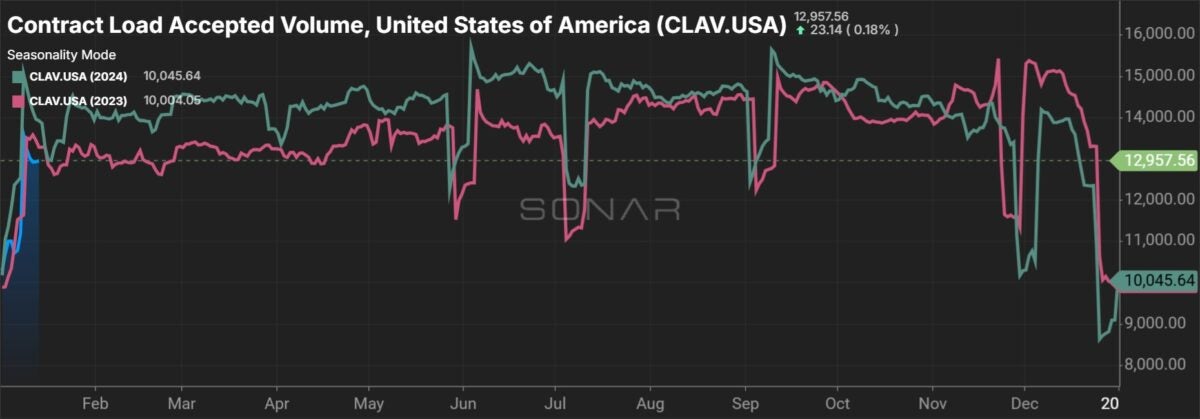

December data from Cass Information Systems showed a significant drop in freight shipments as expenditures were off by a lesser amount, implying freight rates moved higher during the month. Truckload linehaul rates continued to improve from August’s cycle low, a Tuesday report revealed.

Freight volumes captured by the Cass Freight Index fell 7.3% from November and were off 6.5% year over year. Even excluding the typical November-to-December seasonal dip, the index was off 3.1%, which wiped away November’s 2.8% sequential gain.

This was the largest y/y decline for the shipments index since January 2024 and the lowest index reading since June 2020. However, there was some noise during the month. Midweek holidays may have exacerbated the seasonal slowdown. Also, some shippers pulled forward freight deliveries throughout the fall to avoid a potential dockworker strike on Jan. 15.

| December 2024 | y/y | 2-year | m/m | m/m (SA) |

| Shipments | -6.5% | -13.3% | -7.3% | -3.1% |

| Expenditures | -3.4% | -26.3% | -2.6% | 0.5% |

| TL Linehaul Index | -0.4% | -6.5% | 1.2% | NM |

Volumes are off to a slow start in January as well, but winter storms have been widespread and some indecision over trade policy lingers ahead of Monday’s inauguration of President-elect Donald Trump.

The Cass Freight Index is a trucking-centric dataset with more than half of the spend captured tied to truckload shipments. Less-than-truckload, railroad and parcel shipments largely make up the rest.

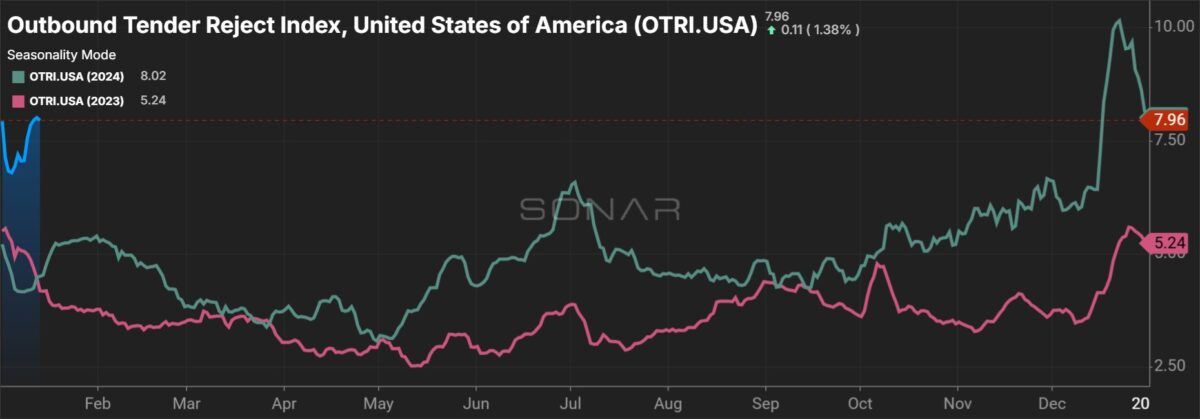

The report said that “ongoing capacity additions are keeping pressure on the for-hire market.” Cass’ January forecast calls for volumes to be down 6% y/y, assuming normal seasonal trends.

The index finished 2024 down 4.1% y/y after falling 5.5% in 2023.

The freight expenditures index, which captures total freight spend including fuel, fell 2.6% sequentially (up 0.5% seasonally adjusted) in December and was down 3.4% y/y. Diesel prices during the month were down approximately 12% y/y (off approximately 1% sequentially).

Netting the change in shipments from the change in expenditures implies actual freight rates were likely up 3.3% y/y during the month. That was the first implied y/y rate increase since November 2022.

The inferred rate index is expected to be positive y/y in January and throughout 2025.

The expenditures index closed 2024 off 11% y/y following a 19% decline in 2023. The index was up 38% and 23% in 2021 and 2022, respectively.

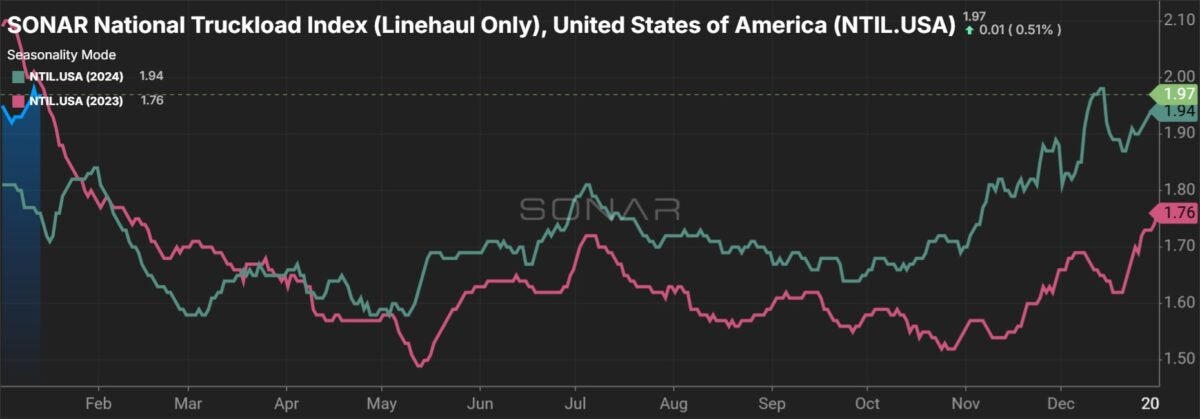

The Truckload Linehaul Index, which excludes fuel and accessorial surcharges, increased for a fourth consecutive month in December, up 1.2% sequentially. A 0.4% y/y decline was the smallest since the end of 2022.

The index includes changes to both spot and contract freight and “is now on the verge of turning positive y/y for the first time in two years, possibly in January,” the report said.

The index fell 10% y/y in 2023 and was down 3% last year.

“Winter weather is driving significant spot activity in January, but the supply response in the past couple of months has been interesting,” the report concluded. “While lower Class 8 supply over the past several months supports a return to rate increases in 2025, the capacity additions to come will be considerable.”

Data used in the indexes comes from freight bills paid by Cass (NASDAQ: CASS), a provider of payment management solutions. Cass processes $38 billion in freight payables annually on behalf of customers.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now