Rarely have container shipping lines played for such high stakes as they are right now. Not only are they attempting to pass on higher IMO 2020 low sulfur fuel bills, they are also in the final stages of agreeing to Asia-Europe annual contracts for next year.

Their success in negotiating both with shippers will go a long way toward deciding industry profitability next year, not least because Asia-Europe contract settlements will also set the stage for trans-Pacific liner-shipper contract negotiations in the second quarter of 2020.

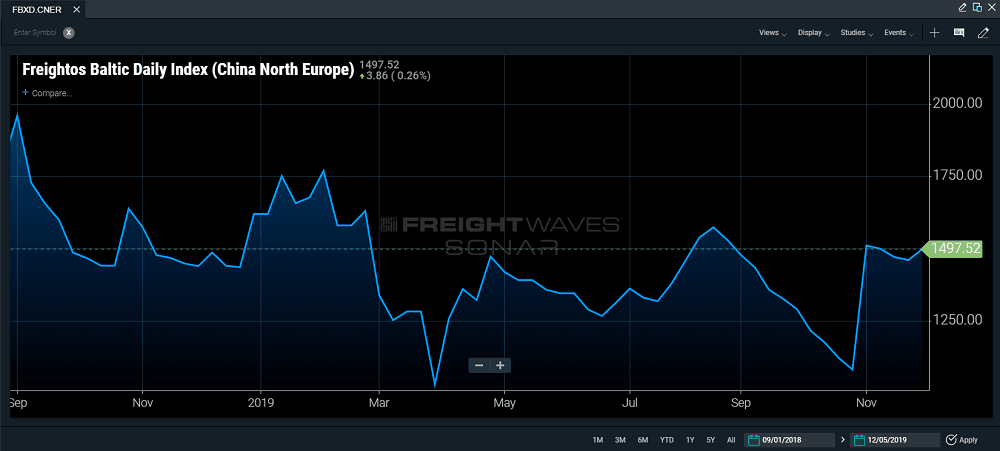

As previously detailed in FreightWaves, a key element of the strategy deployed by container lines has been to boost Asia-Europe spot freight rates to improve bargaining positions with shippers. This has proven a relative success in recent weeks (see the SONAR Freightos Baltic Daily China-North Europe Index below) , aided by the successful implementation of Nov. 1 General Rates Increases and the removal of capacity in the shape of multiple blanked sailings and scrubber retrofits.

“They’re jacking up the short-term rates to try and get in a better position before locking in long-term rates,” explained Patrik Berglund, CEO of Xeneta, an Oslo-based ocean freight rate benchmarking and market analytics platform.

“The next three to four months will see massive volumes settling long-term rates before we move into the second quarter when trans-Pacific/U.S. volumes also will be settled,” Berglund said.

Capacity removal

Reducing slot supply has been the ‘go to’ tactic for lines looking to boost spot rates this year, so it was no surprise when Alphaliner reported earlier this week (Dec. 3) that the inactive container ship fleet had increased sharply across all main size segments to reach 225 ships capable of transporting 1.32 million twenty-foot equivalent units (TEU). As of Nov. 25, the ships accounted for 5.7% of the total fleet.

Shanghai-Rotterdam and Shanghai-Genoa spot rates are now 4% and 3% higher than a year earlier, respectively, according to Drewry. Even so, Berglund said European shippers were currently negotiating their rates from a position of strength compared to this time last year, not least due to the implementation of IMO 2020.

IMO 2020 is the game-changer

“IMO 2020 is the big thing on everyone’s lips,” he told FreightWaves TV’s ‘Port Report’ on Dec. 5.

“We see a major push to have floating bunker mechanisms inserted into long-term contracts for 2020 because of the uncertainty around IMO 2020 [fuel prices].”

He added, “But we’ve already seen some of the carriers have started to offer 12- and 24-month rates with no bunker fluctuations. That means two things to me. Either that they’re satisfied with current rate levels so they’re willing to take the risk. Or they’re concerned the rate level might drop so they’re trying to secure rates at current levels under contracts.”

Shippers should pay more?

Peter Sand, Chief Shipping analyst at BIMCO, said that while he expected freight rates would be decided by fundamental market balance, the entire cost of IMO 2020 fuels really should be passed on to end consumers of products shipped.

“But,” he added, “we have still to see the day when shippers care about lines’ profitability. Operators have worked hard to let shippers know that this is a cost to pass on. Time will soon tell whether that point have fully hit home.”

Sand also said, “No line can afford to shoulder the extra cost fully without sinking into loss-making territory.”

Back-haul leverage

Berglund expects supply and demand to be the deciding factor in the ‘who pays what’ debate over IMO 2020 costs. He thinks shippers with sizable back-haul Europe to Asia cargoes are particularly well-placed when negotiating bunker charges and contract prices with carriers.

“One of the biggest questions we have is how the front-/back-haul imbalance will make it difficult to spread any increased costs across carrier customer bases in a fair manner,” he said. “The ones on the back-haul, and particularly the ones with substantial volumes, have severe leverage when negotiating with the carriers and little incentive to split the bill with front haul shippers.”

Can lines hold firm on IMO 2020?

Neil Dekker, a senior analyst at Infospectrum, also identifies the mandatory use of low-sulfur IMO 2020 fuels for ships not fitted with abatement technology as a game changer for container markets next year. Nonetheless, he expects lines to hold a firm line on the imposition of IMO 2020 bunker surcharges.

“Lines that are not utilizing scrubbers will typically be paying higher prices for low sulfur fuel and will be looking to claim the costs back from shippers – this strategy is not new and liner operators have been preparing for it for some time,” he said.

Carriers do not have a strong track record when it comes to recovering costs for bunker price increases due to ‘all-in’ rate strategies. Historically, these strategies have made it more difficult for them to seek increased bunker fuel costs. However, Dekker expects this to change in 2020 due to the introduction of separate bunker surcharges.

“Lines are expected to take a hard line in enforcing these new bunker surcharges across all trade routes,” he added.

More FreightWaves and American Shipper articles by Mike

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now