Container lines have used general rate increases (GRIs) to forcibly push up Asia-U.S. spot rates, yet there’s widespread skepticism on rates’ staying power given the gravitational pull of weak demand.

Carriers introduced a round of GRIs on April 15 and are scheduled to implement the next round on May 1. But Linerlytica reported Monday that carriers are “already deferring the May 1 GRI” to mid-May because “cargo volumes are unable to support rate hikes despite the blank [canceled] sailings planned in early May.”

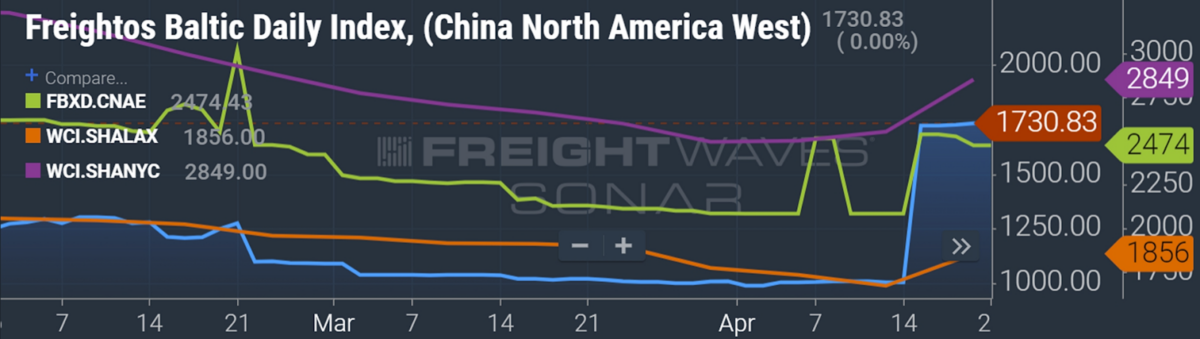

Spot indexes show double-digit gains

Spot rates have gone from highly loss-making to less loss-making. Jefferies shipping analyst Omar Nokta told FreightWaves that carrier breakeven rates on the trans-Pacific are “at least $2,000 [per forty-foot equivalent unit], likely in the $2,500 range” as a result of higher costs — above recently increased spot rates.

The Freightos Baltic Daily Index (FBX) China-West Coast index closed at $1,731 per FEU on Friday. That’s up 72% week on week (w/w). The FBX China-East Coast index was at $2,474 per FEU on Friday, up 19% w/w. FBX trans-Pacific indexes showed further gains on Monday. China-West Coast rates inched up to $1,737 per FEU. China-East Coast rates rose 4% versus Friday, to $2,564 per FEU.

The Drewry World Container Index (WCI) for Shanghai to Los Angeles rose 11% w/w to $1,856 per FEU for the week ending Thursday. The WCI Shanghai-to-New York index gained 12% to $2,849 per FEU.

Platts’ North Asia-to-West Coast spot assessment jumped 28% w/w to $1,600 per FEU, its highest level since Nov. 1. Platts’ North Asia-East Coast assessment rose 21.5% w/w to $2,400 per FEU.

Xeneta’s XSI-C short-term index showed a big jump, as well. As of Friday, the XSI-C put Far East-West Coast spot rates at $1,612 per FEU, up 40% w/w.

‘GRIs are unsustainable’

These big double-digit gains sound impressive, but they’re off a very low base. Furthermore, cracks are already starting to appear in another indicator: the Shanghai Containerized Freight Index (SCFI).

SCFI’s latest trans-Pacific assessments fell 2% w/w, to $1,633 per FEU on the Asia-West Coast route and $2,510 per FEU on Asia-East Coast.

“No sooner had the trans-Pacific rates rebounded than the carriers started to cut rates again, in a pattern that will likely be repeated over the coming months,” said Linerlytica.

According to Jefferies’ analyst of Asian shipping, Andrew Lee, “Our view is that GRIs are unsustainable.” He expects GRIs will only be “partially successful … before the gains erode in the subsequent weeks.”

Platts said in its weekly freight report that “many market participants were skeptical that the increase would continue through the month due to lower consumer demand and weak economic sentiment.”

Carriers will come out looking even weaker if the GRIs don’t hold, one freight forwarder told Platts. It would “effectively prove that they won’t be able to push rates up.”

Higher spot rates not driven by higher demand

There’s no evidence yet that trans-Pacific rate increases are being supported by higher import demand or improved bookings.

2M Alliance partner MSC announced three more blanked sailings on Friday due to “lower demand on its Asia-US trade.” A sailing was canceled for the Good Prospect (capacity: 6,350 twenty-foot equivalent units) during the first week of May. Another was canceled for the 13,092-TEU Maersk Esmeraldas the following week and the 14,000-TEU MSC Livorno the week after that.

Matson (NYSE: MATX) said Wednesday that it expects second-quarter volumes and rates “to reflect freight demand levels below normalized conditions.”

According to Henry Byers, head of ocean intelligence at FreightWaves, “Our container volume indices based on bookings at origin do not reflect any significant increases in demand. For container volumes set to depart origin in the next seven to 14 days, the data actually points toward a further decline in demand.”

Timing coincides with contract negotiations

The April 15 GRIs and planned May GRIs coincide with the tail end of talks between ocean carriers and shippers on annual contracts that run from May 2023 through April 2024.

Analysts overwhelmingly believe the timing is not coincidental, although they diverge on the rationale. Some theorize the GRIs came after contracts were signed, others that GRIs are a negotiating tactic.

Xeneta market analyst Emily Stausbell said during a presentation Tuesday, “Maybe carriers have reached a decision that they’re comfortable with the long-term contracts they’ve signed and they’re willing to play a little bit more in the spot market to try and push those rates up.”

In contrast, Linerlytica maintained that “a large number of trans-Pacific contracts have yet to be concluded. Negotiations with NVOCCs [non-vessel-operating common carriers] are particularly problematic for carriers given current rate volatility.

“Some carriers have extended preferential NVOCC rates to the end of June as the share of contract volumes has shrunk to less than 30%,” said Linerlytica.

According to Frode Mørkedal, shipping analyst at Clarksons Securities, “Shipping lines may try to strengthen the spot market in order to secure higher contract rates. However, their ability to keep rates high will be tested in the coming weeks. Current GRIs may be unsustainable and driven primarily by contract negotiations. Liner companies are navigating a delicate balance as demand remains tepid.

“Even if recent spot rate increases succeed in raising contract rates above recent spot levels, new contract terms will be significantly lower than last year, implying that liner earnings will drop substantially in the second half. Overall, we believe the deck is stacked against liner companies, implying that the recent rate increase may only be a temporary reprieve,” wrote Mørkedal in a client note on Monday.

2024-25 FFAs below breakeven

There has been increasing talk of container rates finding a bottom over recent weeks as trans-Pacific spot rates have risen. The counterargument is that the historically large wave of newbuild tonnage only began hitting the water in March and will continue to flow unabated through at least 2025.

One prism on future sentiment is the derivatives market. Container shipping forward freight agreements (FFAs) are settled against the FBX, with Freight Investor Services (FIS) serving as a lead broker.

FFA prices reported by FIS Monday show near-term strength and long-term weakness. And even in the near term, contracts are priced below the trans-Pacific breakeven level cited by Nokta.

The April FFA contract for China-West Coast is at $1,775 per FEU, May at $1,825 and June at $1,875. The Q2 2023 contract is at $1,825 per FEU and Q3 2023 is at $2,075. The Q4 2022 contract is lower, at $1,900.

FFA contracts for next year are priced lower still. The Q1 2024 contract is at a mere $1,550 per FEU — 16% below Monday’s FBX rate. Q2 2024 and calendar-year 2024 contracts are both at $1,800 per FEU, just a few dollars above Monday’s rate. The calendar-year 2024 contract has declined around 10% since the end of last month. The 2025 contract is at $1,975 per FEU, still below breakeven.

FIS said in a client note on Monday morning: “Transpacific GRIs … might be more bark than bite, coinciding with tendering of new contracts. [The] 2024 fundamentals remain little changed, with the bulk of the newbuild deliveries happening in 2024, proving a strong case to sell into fresh bid interest.”

Click for more articles by Greg Miller

Related articles:

- Container shipping sees signs of a bottom (at least, for now)

- Container lines still up vs. pre-COVID despite fall from peak

- Mixed signals: Container shipping downturn not following the script

- Crunch time for trans-Pacific container shipping contract talks

- How much will container lines ‘earn’ in 2023? It depends on the metric

- ‘Colossal’ tidal wave of new container ships about to strike

- Back to the futures: New era of container freight hedging begins