Air cargo freight rates have spiked in recent weeks as the traditional peak season approaches, but there is growing evidence that any rebound after a tough year for carriers will be fleeting.

The International Air Transport Association (IATA) reported last week that growth in industry-wide freight ton kilometers (FTK) remained negative in September, with volumes down a sizable 4.5% year-on-year following a 4.2% fall in FTKs in August.

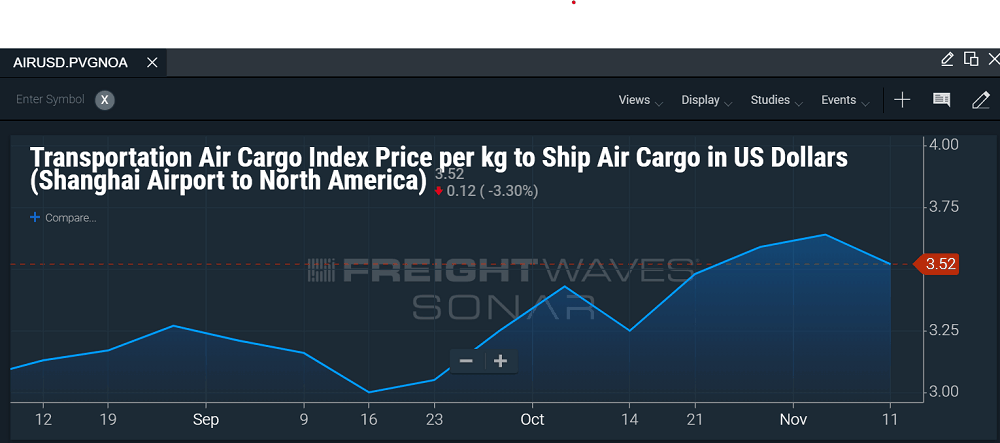

But since the end of September, there has been more life in airfreight markets. FreightWaves’ SONAR reveals that in the last six weeks airfreight pricing from China to North America has been volatile, but steadily rising (see below).

Hong Kong-to-North America prices, meanwhile, have been making gains since the start of September, albeit from a low base.

In Europe, anecdotal evidence suggest airfreight activity may have received a slight bump in demand ahead of the scheduled exit of the U.K. from the European Union on Oct. 31, a deadline that has now moved to Jan. 31. But air freight pricing from Asia to Europe in the last three months (see below) shows much the same trend as the trans-Pacific.

However, forwarders contacted by FreightWaves suggest the 2019 peak season could be short-lived. “The airfreight rates did increase during the last few weeks, but it looks like the situation will not last long and will likely end this week,” said Paul Tsui, managing director of Hong Kong-based forwarding and logistics operator Janel Group.

“The mini peak has passed already,” added Brian Wu, chairman of the Hong Kong Association of Freight Forwarding. “Starting this week it becomes slack again.”

Trans-Pacific might bust

Another forwarder, one with a strong presence on the trans-Pacific, has seen an increase in spot market rates in South and North China over the past four weeks of “between 10% and 15%”. But an executive at the company, speaking to FreightWaves on condition of anonymity, expects the market to come back to earth sooner rather than later.

“I think this is being driven by relatively strong U.S. consumer demand, traditional peak season increases and a bit of a push by shippers to beat the next round of tariffs,” he said.

He noted that charter markets had picked up recently but predicted the upturn would be short-lived. “We’ll take what we can get,” he added.

“I don’t think this has changed the structural situation and we are still headed for a tough first half of 2020.”

2019 vs 2018 vs 2017

As SONAR illustrates, the 2019 fourth quarter peak season both on Asia-Europe and trans-Pacific lanes looks very different to the 2018 and 2017 fourth quarters.

As the SONAR chart above makes clear, the air freight peaks of both 2017 and 2018 on Asia to Europe lanes saw rates climb far higher than at present. Inflated rates were also sustained for a lengthy period. The same trends were evident on the trans-Pacific trades (below).

Peter Stallion, an air cargo derivatives broker at Freight Investor Services (FIS), believes much of the 2019 end-of-year peak is due to the “collective will” of carriers to boost returns. He notes that “prices are still well below 2018 and volumes underlying the revenue are nowhere near the levels of 2017 and 2018.”

He added, “As such, less is actually coming in in terms of revenue, and thus company-wide margins are watered down.”

Volatility the new normal

Stallion said weak cargo volumes had led FIS to conclude that pricing momentum could not be maintained for long and more volatility was likely. “Spot market rates remain as volatile as they always are,” he added.

Moreover, with so much uncertainty surrounding global trade, not least due to the U.S.-China trade war and Brexit, forecasts are difficult.

“The outlook remains completely uncertain,” he added. “U.S.-China trade politics have been put under the threat of rollback, and whilst British trade has been given a stay of execution with the progress of a deal, the landscape of post-Brexit trade and European trade remains impossible to predict.”

This was a point also made by Steven Polmans, the new chairman of The International Air Cargo Association (TIACA) and director of cargo and logistics at Brussels Airport Company. He told FreightWaves last week that uncertainty around Brexit and the U.S.-China trade war was adding dark complexity to airfreight markets.

Uncertainty guaranteed

“The fact is that we do not know that if in two weeks from now China and America could suddenly become big friends or we could be back in the midst of an economic war,” he said. “These kinds of things make it so difficult. The volume changes we see at Brussels Airport, for example, on a weekly basis is the craziest thing I’ve seen in a long time. You go from plus 10% in one week to minus 10% the week after.

“So the unpredictability is really causing a lot of concerns to everybody,” Polmans said.

Brandon Fried, executive director at the Airforwarders Association, said the organization had just began its annual “How’s Business?” survey and so far “responses indicate flat volumes with optimism for the next six months and year.”

He added, “Comments received so far, although early into the survey, indicate frustration and concern with current global trade policy, including uncertainty created by the imposed tariffs, retaliation by U.S. trading partners and a challenging regulatory environment here in the U.S., especially in California.”

Stallion predicted that in the near term, carriers would do all they could to float the price of capacity for as long as possible, noting the words of Cathay Pacific’s Frank Yau, who said, “We anticipate the peak will last into early December.”

However, said Stallion, “temptation will loom for rates to be dumped in order to secure market volumes and revenue.”

He added, “Such an inflection point is notoriously difficult to forecast. November-December hedges will aim to strike through this inflection point, removing the risk of market spikes and dumps.”

More FreightWaves articles by Mike