“The market is shit. Sorry for my French,” said Hugo De Stoop, CEO of Euronav (NYSE: EURN), the world’s largest listed crude-tanker owner.

Speaking on Thursday’s call with analysts, De Stoop was explaining why Euronav is pulling forward required drydockings from H1 2021 and will drydock nine of its tankers — 15% of its fleet — this month and December.

“When you’re in the drydock, you’re not earning money,” he said. “It’s like those guys retrofitting scrubbers in a market that was absolutely fantastic [in H2 2019]. This is the opposite. This is a good moment, from a market perspective, to not be out there in the market.

“Two months down the road, you could have some event that is not foreseen and the market could be ripping. So, you want to do [drydockings] when you know the market is not very good, and you want to do as many ships as possible.”

Euronav seems to be effectively throwing in the towel on hopes for a strong fourth quarter, even though this period usually enjoys a big seasonal boost.

According to De Stoop, “The usual seasonal backing of improving demand for oil into the key winter period has not gained traction.

“Vessel supply remains elevated. Cargoes are limited with low visibility on cargo programs. Sentiment among owners remains weak when setting freight rates.”

Floating-storage disparity

Crude and refined product tankers are two different markets but they’re correlated over time.

During a conference call Thursday, Robert Bugbee, president of product-carrier owner Scorpio Tankers (NYSE: STNG), argued that the two markets are diverging.

“For too long we’ve just talked about ‘tankers,’ he said. “We need to really divide product tankers away from crude-oil tankers. There is a difference between the crude-oil market and the product market. In the crude-oil market, there is a high degree of storage left on the ships.”

James Doyle, Scorpio Tankers’ senior financial and research analyst, said that refined-product floating storage peaked at 107 million barrels in May and was down to an average of 36 million barrels in October. “We’ve seen a continued decline,” said Doyle, noting that the normal average is around 10 million barrels.

In contrast, he said, crude-oil floating storage peaked at 290 million barrels, is still at 250 million barrels and is normally around 150 million barrels. “It’s certainly slower [the drawdown] and it’s hard to say how long it will take on the crude side,” said Doyle.

Ton-mile growth disparity

The other argument for product tankers over crude tankers is that large new refineries are ramping up in the Middle East and old refineries are shutting down in Europe and Australia. As a result, refinery capacity is getting closer to crude production and further from end consumers.

This means that refined products should travel longer distances by ship, and conversely, crude oil could travel shorter distances. Shipping demand is measured in “ton-miles”: volume multiplied by distance.

“The crude-oil market does not have the same dynamics of inherent ton-mile demand growth that the product market does,” said Bugbee. “The opening of these Middle East refineries is positive for products. It’s at best neutral and at worst detrimental for crude-oil ton-miles.”

Scorpio Tankers Commercial Director Lars Denker Nielsen cited estimates that 2020 product-tanker demand will end up at 225 billion ton-miles. That would be unchanged from 2019. But ton-mile demand for 2021 is estimated to be 236-237 billion, up 5%. “If true, that is a lot more ships that have to move in addition to where we are now,” said Nielsen.

Rates and share pricing

Bugbee maintained that product tankers are outperforming crude tankers on a deadweight ton (DWT)-weighted basis. He also sounded more confident than De Stoop on seasonal upside, despite European COVID lockdowns.

“I’m going to go out on a limb and say there will still be a winter in the Northern Hemisphere,” said Bugbee.

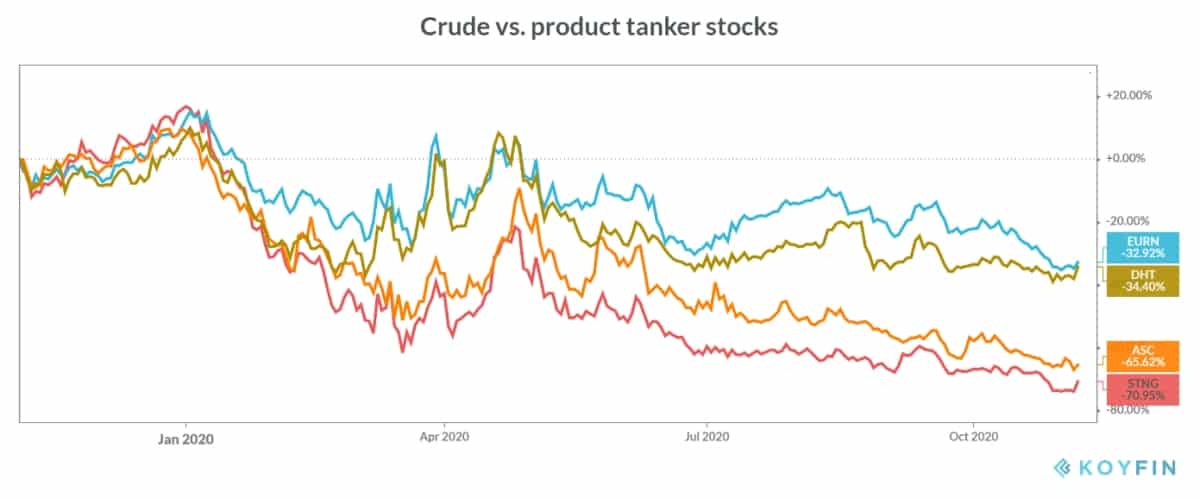

But to take the other side of the crude-versus-product-tanker debate: First, rates for both types of ship are very low for this time of year. Second, new refinery capacity is also surging in China, close to end consumers. And third, shares of product-tanker owners have significantly underperformed shares of crude-tanker owners.

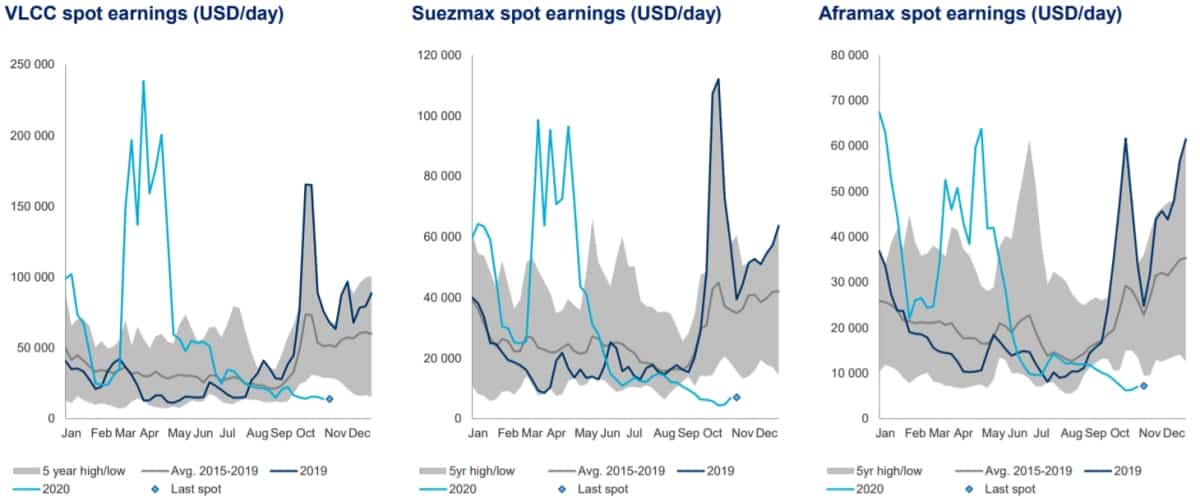

Clarksons Platou Securities estimated rates on Thursday at $13,400 per day for very large crude carriers (tankers that carry 2 million barrels of crude oil) and $7,300 per day for Suezmaxes (tankers that carry 1 million barrels of crude).

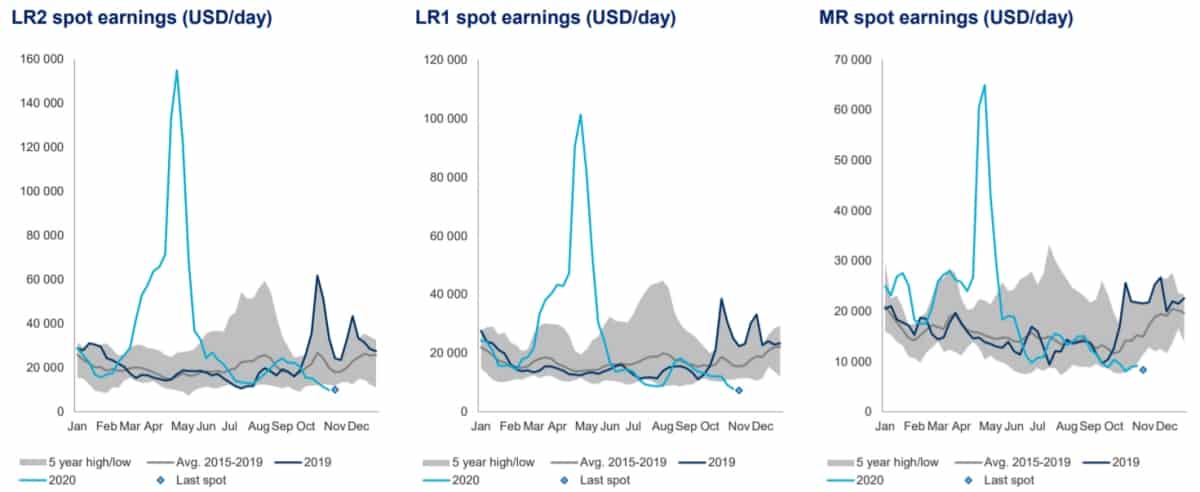

On the product-tanker side, Clarksons put rates for LR2s (80,000-119,000 DWT) at $10,700 per day. It assessed rates for MRs (25,000-54,999 DWT DWT) at $6,900 per day.

Regardless of ship category, the Clarksons data shows a significant drop versus the 2015-2019 average.

Meanwhile, year-over-year share trends have clearly diverged. Among the larger pure crude-tanker owners, Euronav is down 33% and DHT (NYSE: DHT) is down 34%. The product-tanker shares are also clustered — at a much weaker level. Ardmore Shipping (NYSE: ASC) is down 66%, while Scorpio Tankers is down 70%.

Q3 2020 results roundup

After the closing bell on Wednesday, Scorpio Tankers reported a net loss of $20.2 million for Q3 2020. That compared to a net loss of $45.3 million in the same period last year, while adjusted losses per share came in at 37 cents, better than consensus expectations for a loss of 42 cents per share.

Before the opening bell on Thursday, Euronav reported net income of $46.2 million for Q3 2020 versus a net loss of $22.9 million in Q3 2019. Earnings per share came in at 22 cents, just below the consensus forecast for 23 cents.

“Euronav is without question the bellwether of the crude tanker market,” said Stifel analyst Ben Nolan. “Unfortunately, right now that makes them the best house in a bad neighborhood.”

Or, as Evercore ISI analyst Jon Chappell more colorfully put it, Euronav is like “a mint mansion in 1980s Detroit.” Click for more FreightWaves/American Shipper articles by Greg Miller

MORE ON TANKERS: Why crude tanker collapse could be long and painful: see story here. How are tanker owners coping with the floating-storage hangover? See story here. Tanker rate puzzle gets even harder to solve: see story here.

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now