OPEC+ shocked the market in early March by keeping production cuts in place. Definitely not what the tanker industry wanted to hear. In typical fashion, it was spun as good news for shipping: Spot-rate pressure would be even worse in the near term, but the pain would end quicker as oil inventories drew down faster.

OPEC+ surprised the market yet again in early April — this time by finally agreeing to increase production. This is what tanker owners had been hoping and expecting to hear four weeks earlier.

According to Clarkson Platou Securities analysts Frode Mørkedal, the OPEC+ agreement “positions tankers for an earlier recovery than expected” and is “a significant positive for the tanker sector.”

Jefferies analyst Randy Giveans believes that “with oil inventories now in line with the five-year average and demand on the rise … crude tanker rates will improve.” Deutsche Bank analyst Amit Mehrotra predicted “larger and more frequent [production] increases to come.”

OPEC+ production strategy is just one piece of a very complicated puzzle. Another piece is non-OPEC exports. Particularly long-haul U.S. crude exports to India, as revealed by new data from Kpler provided to American Shipper.

OPEC+ re-opens the spigot

Between OPEC+ and Saudi Arabia individually, production will increase by 600,000 barrels per day (b/d) in May, 700,000 b/d in June and 841,000 b/d in July.

The combined 2.14 million b/d increase will come in the wake of 8 million b/d in cuts. Of that, around 7 million b/d has been cut by OPEC+ since last year and 1 million b/d by Saudi Arabia since the beginning of this year.

The big question is: How much of the May-July increase will actually flow into tankers? The bump-up in production coincides with a time of year when the Middle East consumes more domestically for air conditioning.

According to Fearnleys Securities, “While increased production, on paper, will lend support to tanker rates, increased domestic demand in the Middle East is likely to cap the seaborne exports somewhat. We maintain our view that the staggered 2 million b/d return is unlikely to shift crude meaningfully near term.”

Clarksons Platou expects the vast majority of the 2.14 million b/d May-July increase — 1.914 million b/d — will come from OPEC. Of that, it said, 1.376 million b/d will come from Saudi Arabia.

Mørkedal acknowledged in a research note that “some of the additional Saudi production will likely go towards domestic power generation” as well as to domestic refineries, such as the new Jizan facility, for products exports.

Nevertheless, Mørkedal maintained, “The increase in domestic power generation and refinery use seems very unlikely to absorb the full 1.376 million b/d restoration of Saudi volumes.”

Clarksons sees rate upside from the OPEC+ decision for both very large crude carriers (VLCCs, tankers that carry 2 million barrels of crude oil) as well as LR2s (larger refined product tankers with capacity of 80,000-119,999 deadweight tons or DWT).

The first test for VLCCs will come in the next few days, when May cargoes go on the market.

US crude exports resilient

Meanwhile, the U.S. crude export trade — a pivotal route for VLCCs — is holding up extremely well amid the pandemic.

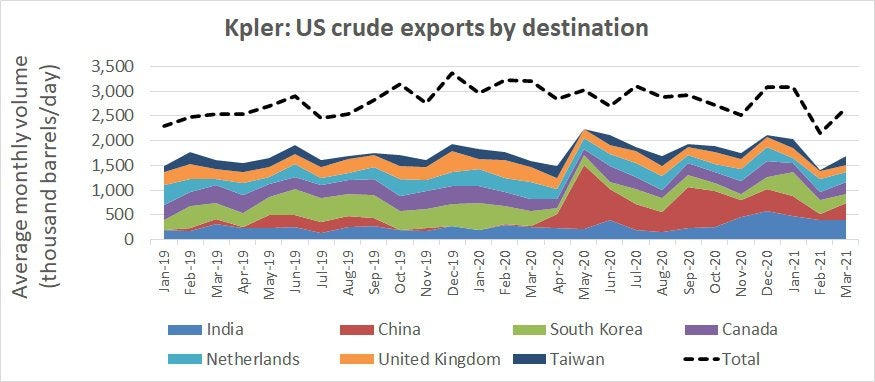

Export volumes averaged 2.9 million b/d in 2020, up 8% year-on-year, according to data from commodity intelligence company Kpler.

Shipments of U.S. crude to Asia are particularly important to VLCCs due to voyage length. It is more than twice as far to China or South Korea from the U.S. Gulf as it is from the Middle East. It is more than eight times as far from the U.S. Gulf to India as it is from the Middle East.

Shipping demand is measured in ton-miles: volume multiplied by distance. The longer the average voyage length, the fewer vessels are free to bid on spot contracts, a plus for rates.

The Kpler data shows that shipments to China were the biggest driver of 2020 U.S. crude exports. Volumes to China quadrupled versus 2019 to a full-year average of 461,000 b/d, around one-sixth of all U.S. crude exports. Cargoes to China spiked in April and May, then pulled back more recently.

The India factor

Shipments to India were the second-most important driver of U.S. crude exports in 2020. These volumes were up 26% year-on-year to 287,000 b/d, representing just under a tenth of the total.

This year, India has emerged as the No. 1 destination for U.S. crude exports, according to Kpler data. India imported an average of 421,000 b/d of U.S. crude in Q1 2021, well above volumes to South Korea — 313,000 b/d — and China, which is down to 295,000 b/d.

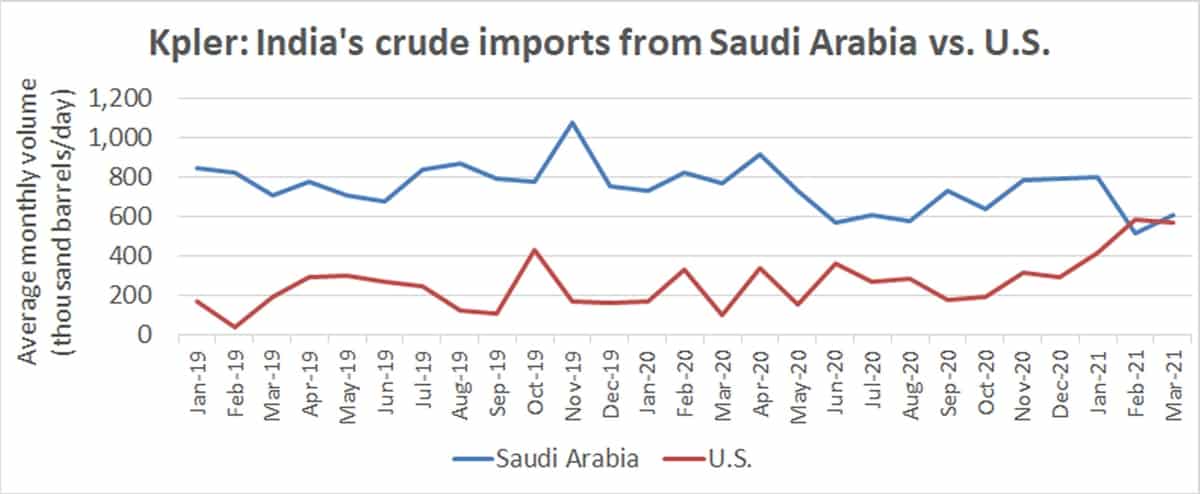

The Kpler data reveals that India has made a dramatic change in its crude sourcing, at least temporarily replacing Saudi volumes with U.S. cargoes. That change is particularly positive for VLCC demand due to the much longer voyage length from the U.S.

Over the two-year period covering 2019 and 2020, India imported 3.3 times more crude oil from Saudi Arabia than from the U.S. But over February and March 2021, India has imported slightly more crude from America than from Saudi Arabia.

Erik Broekhuizen, manager of marine research at Poten & Partners, highlighted the India factor in a research note last month.

He pointed out that India’s population could surpass China’s as soon as next year, and “even a small change in preferences away from the Middle East towards long-haul suppliers such as the U.S., Brazil or Guyana can have a disproportionate impact on tanker markets because of the ton-mile effect.”

In Q1 2021, Atlantic Basin crude sources represented over 50% of Indian crude imports measured in ton-miles, said Broekhuizen, whereas the Middle East represented just 16%.

Crude tankers still well below breakeven

The first quarter of 2021 has been historically bad for the tanker sector. During the past month, some day rates for VLCCs have been assessed in negative numbers, implying that some ship owners may have paid more for a voyage’s fuel than they received to transport the cargo.

This month, rates are up off their lows but still weak — in some cases, extremely weak.

Clarksons estimated Friday that spot rates for eco-design VLCCs averaged $11,500 per day. Of all the tanker segments, VLCCs have risen the least off their Q1 nadirs and are down the most compared to the 2016-2020 average for this time of year, in the case of VLCCs, of over $60,000 per day.

VLCC owners are still bleeding money. Current rates are about half of all-in cash breakeven, which includes financing costs as well as operating expenses.

Eco-design Suezmaxes (tankers that carry 1 million barrels of crude) and Aframaxes (750,000 barrels) are both earning more than VLCCs, at $12,600 and $12,900 per day, respectively. These rates are also well below cash breakeven.

Some product tankers back in black

Product tankers are faring better than crude tankers. Particularly LR2s, which are doing better than any other tanker category despite the global shortfall in jet-fuel cargoes. In fact, some LR2 owners may have actually booked recent voyage deals at a profit.

Clarksons assessed eco-design LR2 spot rates on Friday at $22,800 per day, close to the 2016-20 average. It assessed non-eco LR2s at $19,300 per day. Giveans at Jefferies estimated that an LR2’s cash breakeven is around $16,000-$19,000 per day, depending on debt costs — below current spot rates.

Clarksons assessed rates for eco-design LR1 product tankers (55,000-79,999 DWT) at $16,400 per day and for MRs (25,000-54,999 DWT) at $12,200 per day. LR1 rates are near breakeven; MR rates are getting closer.

Tanker stocks up: More room to run?

Sentiment toward the second-half tanker rates is strong, convincing some investors to buy tanker stocks early when shares are trading at a discount to net asset value (NAV).

While the OPEC+ decision didn’t move the stocks, Giveans predicts it eventually will.

He told American Shipper, “Tanker equities haven’t yet rallied on the recent OPEC+ news as investors want to see the increased production quotas actually get produced and exported before they pile into the tanker names.

“Also, tankers have already had a strong bounce, with an average gain of 29% during Q1 2021. But even now, our top picks still trade at an average 19% discount to NAV. With asset values, rates and investor sentiment all on the rise, we expect tankers to continue to outperform throughout 2021.”

The tanker stock with the most exposure to the best-performing sector — LR2s — is Scorpio Tankers (NYSE: STNG). Scorpio is outperforming the rest of the pack: up 62% year-to-date.

Some investors may be ‘vastly disappointed’

Not all analysts are as bullish as Giveans.

Remember how the March OPEC+ decision to keep cuts in place was dubbed good news because inventories would fall faster? Some believe OPEC+ should have kept cuts in place this month, too.

According to Alphatanker, “Although there may be some upside to tanker rates over the coming months … the anticipated sustainable, strong recovery in hire rates in Q4 2021 may be clipped or delayed, as there will remain a significant oil inventory overhang to be cleared. This overhang would have been significantly smaller had [OPEC+] decided not to hike production.

“Furthermore, the specter of increasing tanker demand in Q2 2021 may see less tankers scrapped than would otherwise have been the case.”

Evercore ISI analyst told American Shipper, “I’m in agreement with consensus that the worst of the downturn is over. But I just don’t subscribe to this ‘super-cycle with container ships and dry bulk markets and stocks on fire so tankers have to follow’ thesis. Tankers don’t have to follow to the same magnitude. The fundamentals are vastly different.”

Chappell continued, “Even though OPEC is adding more barrels back, it is happening at a much more measured pace than anyone could have imagined even three months ago. And global oil demand will not return to 2019 levels until the second half of 2022 at the earliest.

“In the meantime, though the orderbook remains incredibly low, the fleet has still expanded at about 3% annually into this demand collapse, and it will take time for utilization to return to late-2019 levels.

“So, the market is definitely on the verge of meaningful improvement. But if investors are expecting container-ship or dry bulk cyclical peaks, they’re going to be vastly disappointed,” Chappell warned. Click for more articles by Greg Miller

Related articles:

Another shipping stock bites the dust as big tanker fleets merge

Brokerage Compliance Symposium

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

F3 Awards Dinner

The night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

F3: Future of Freight Festival

Industry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The day before F3. Every compliance issue you face - fraud exposure, carrier liability, FMCSA rules, cargo theft, insurance gaps - navigated by attorneys and operators defining best practices in a changing industry.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowThe night before F3. FreightTech100 companies honored. FreightTech 25 and Shipper of Choice winners revealed live. Cocktail reception into dinner and live music - 300 industry leaders in one purpose-built room.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register NowIndustry-defining keynotes, rapid-fire technology demos, and industry leaders networking in experiences across Chattanooga - plus the inaugural F3 Awards Dinner featuring the FreightTech and Shipper of Choice reveals.

The Signal at Chattanooga Choo Choo • Chattanooga, TN Register Now