Transportation and supply chain provider Universal Logistics Holdings said lagging demand for auto parts contributed to a sluggish first quarter.

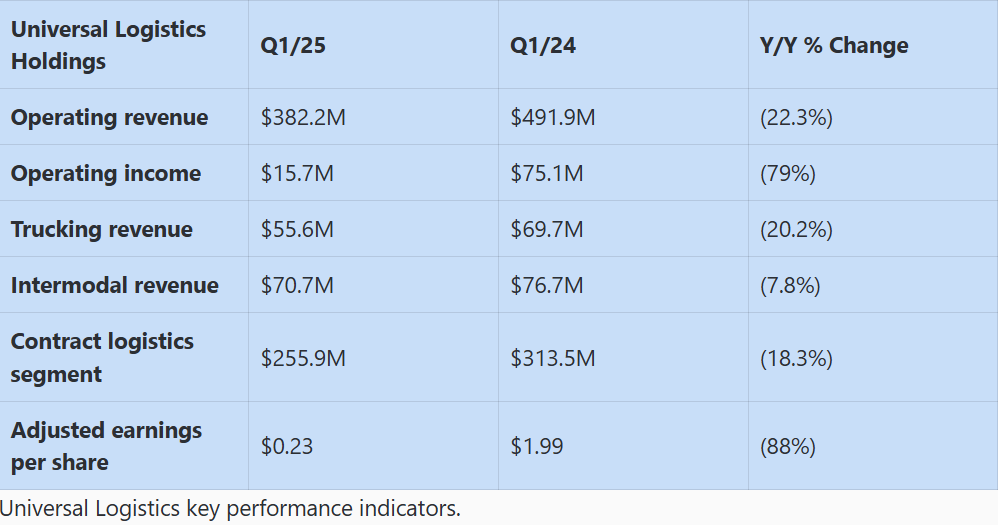

Universal Logistics’ (NASDAQ: ULH) first-quarter operating revenue decreased 22.3% year over year to $382.4 million. First-quarter earnings per share came in at 23 cents per share, an 88% year-over-year decrease.

“The overall freight environment remained sluggish, and our largest vertical, automotive, saw a slowdown in January but improved as the quarter progressed,” CEO Tim Phillips said during a call with analysts Friday. “While the results of this quarter were below our historical benchmarks, we remain confident in the resilience of our business model.”

The company released first-quarter financial results after the market closed on Thursday.

Universal Logistics is a Warren, Michigan-based truckload transportation, intermodal and logistics provider. The company provides services across the U.S, Mexico, Canada and Colombia and has more than 10,000 employees.

Universal Logistics missed Wall Street analysts’ revenue estimates of $454.1 million in the fourth quarter and earnings per share expectations of $1.04.

The company’s first-quarter results showed year-over-year decreases in its trucking, contract logistics, intermodal and managed brokerage segments.

CFO Jude Beres said the year got off to a slow start.

“In January of this year, Universal experienced its first loss ever in a January. We went into February 5 cents in the hole, losing 5 cents of earnings per share,” Beres said. “Then the quarter slowly got better. We went from negative 5 cents a share in January to positive 9 cents a share in February, and then 19 cents a share in March. So the quarter really started out low and the business really rebounded well.”

Universal’s contract logistics segment, including value-added and dedicated services, posted first-quarter revenue of $255.9 million, a decrease of 18.4% year over year from the same quarter in 2024.

By the end of the first quarter, Universal Logistics managed 87 value-added programs, including 20 rail terminal operations, compared to a total of 71 programs at the end of the same period in 2024.

“We have three key launches in contract logistics that will begin in the second quarter,” Phillips said. “These launches will increase our contract logistics annual revenue by 50 million per year.”

Universal’s trucking segment decreased 20.2% year over year to $55.6 million. During the first quarter, Universal moved 28,622 loads compared to 41,691 loads during the same period last year, a 31% decline.

“We continue to see strong demand in our specialized heavy-haul window operation, which remains a strategic differentiator and a stabilizing force for this segment,” Phillips said. “Looking ahead, we expect this business to be a key contributor in 2025 especially as renewable energy infrastructure projects continue to move forward.”

The trucking segment’s average operating revenue per load, excluding fuel surcharges, increased 24% year over year to $1,874. The average number of Universal tractors decreased 22% year-over-year to 633.

Universal Logistics officials said while freight movements were slow in January, they rebounded in February, March and April.

“The quarter really started out low and the business really rebounded well,” Beres said. “For example, our cross-dock tonnage in February was up 30% from January, March’s cross-dock tonnage was up 64% from January. Auto production was up 29% in February compared to January, and then up 67.1% in March compared to January. If we just would have had an environment in January that was similar to February, the results would have looked a lot different. We would have definitely been within our guidance range of around $400 million in revenue and earnings of around 41 cents.”