State of Freight five takeaways: a strong market likely sticking around

The February State of Freight webinar was the third consecutive event where after months–years, really–of talking about weak freight markets, the discussion was once again about one that was increasingly strong.

And as FreightWaves and SONAR CEO Craig Fuller and SONAR Zach Strickland looked out over a radically different freight landscape than just three to four months ago, it raised the inevitable question: does this rally have legs?

The answer from both of them was unequivocal: yes, it does.

That was one of the conclusions from this month’s discussion. It’s one of five takeaways from the February two-person roundtable held Thursday.

The strengthening market isn’t going to fade away

“The big disagreement in the market is why and how is this sustainable,” Strickland said in the opening minutes of the discussion.

Fuller chimed in that “there is no disagreement that this is a very different market today. The big disagreement is why and how it is sustainable.”

Fuller believes it is. He noted that conditions that might have temporarily made the market tighter in late January and early February are out of the market, including the impact from the storms that hit the Northeast and parts of the South in late January, are out of the market. And yet the strength continues.

“It is still very, very tight and we’re in a situation where the market has not gone back to where it was before,” Fuller said.

Snapshots of several iterations of the Outbound Tender Rejection Index (OTRI) in SONAR were shown in the presentation, with the primary national index hitting about 12.2% at the end of December, sliding back slightly through much of January but then soaring once again to a recent number of about 13.7%.

Fuller said demand is not a “market catalyst” that is strengthening markets, owing more to tightening capacity. The current rejection rates, he said, “are telling us that this market is really primed for a breakout in mid-February.”

February, Fuller joked, is usually the time to do cat memes if you’re in the business because of the lack of activity. “Especially in the second half, there’s nothing that happens in February,” he said. “You get a little bit of activity for the Super Bowl, you get a little bit of activity for Valentine’s Day, and then from mid-February to really early March, nothing interesting happens in freight.”

Industrial activity is a big factor in the surge

Fuller and Strickland rolled out a map of rejection rates by region, with the darker blue areas showing a higher rejection rate than other parts of the country. Fuller said the tighter freight market is occurring in “the industrial parts of the economy.”

Fuller said the OTRI rate has always skewed toward industrial activity. Its increase “is telling me that the recovery we’re seeing is starting to show up in manufacturing,” he said.

Discussions between SONAR representatives and their shipper clients, Fuller said, have pointed out that “this tightness in the Midwest is very unusual.” And what’s unusual about it is that a corresponding surge is not happening on the coasts, particularly the U.S. West Coast, where a significant amount of consumer goods is imported. (The OTRI for Los Angeles has been less than 5% for all of 2026).

Quickly running through a series of Midwest cities with rising OTRI rates, Fuller noted that many of those locations provide products such as batteries, “heavy equipment that goes into the auto sector and aircraft parts out of Kansas City.”

“We have not seen the Midwest perform like this in years when the West Coast was not,” Fuller said. “I can’t remember the last time that ever happened.”

Shippers are getting more selective and demanding quality

The tough freight market of the past few years means that some of the equipment on the road is showing its age, Fuller said. “We’re not getting new capacity added in, and it means the sustainability of this market is quite good,:” he said.

But it also means that shippers are going to have to fight to secure high-quality capacity. Fuller spoke of products like GenLogs that enable shippers to better screen the capacity that is in the market.

“I’m hearing that shippers in their RFPs for capacity in this round of bids are asking brokers to talk about their process for avoiding non-domiciled CDL owners,” Fuller said. “Do you have a way to screen out bad carriers? Talk about your compliance processes, talk about your fraud mitigation solutions. What is your process for ensuring that my freight stays safe?”

The end result, Fuller said, is that “companies have the tools to filter a lot of the bad actors out of the business. These bad actors aren’t getting freight. So we’re seeing a rally in contract rates.”

A drop in bankruptcies is not assured

It may seem counterintuitive, but Fuller said the current market conditions may accelerate bankruptcies. First, it’s been a “long, long journey of really abysmal conditions and the sins are starting to pile up.” Company balance sheets “have memories,” he said.

In some cases, real estate and equipment assets start to rise in value as the market strengthens, with the result that a company may be more valuable broken up than continuing even in a stronger market, Fuller said.

Those conditions mean that lenders can start to put pressure on their creditors, “and that’s going to accelerate bankruptcy.” Fuller noted that the bankruptcy of Celadon in late 2019 occurred as a weak freight market that year was starting to strengthen, not at the bottom of the trough.

A strengthening market is new to some market participants

With spring 2022 generally seen as the start of the freight recession, Fuller noted that some people in the industry, brokers in particular, may never have seen rising markets and might not be primed to take advantage of the new conditions.

What constitutes a great market can differ among market participants. For example, brokers have discussed how the rise in spot rates has been painful for their margins given that they secured contract business from shippers at lower numbers.

Fuller said he recently had a conversation with a CEO of a major brokerage firm. The CEO was asked how the market was. The response: not great.

“I asked you about the market,” Fuller said. “I didn’t ask you about your margins.” From that perspective, Fuller said, the conversation was quite different. “He’s like, oh, it’s great. Volumes are popping and demand is there.”

Shipping executives also might find themselves in a world they haven’t been in for awhile. Fuller said those C-suite denizens might want to think about increasing their shipping budgets by 10%, “because remember, you don’t get to be the shipping executive if you miss your budget by a long yard. So I would ask for some real higher budgets this year.”

To back up that request, Fuller said a chart of the SONAR OTRI should be used.

FMCSA finalizes changes to reduce burdens on truckers

WASHINGTON — Following a broad deregulatory initiative launched last year, the Federal Motor Carrier Safety Administration has finalized 11 of 18 rulemaking actions originally proposed in May 2025.

The final rules, published on Thursday, address a range of operational requirements, from vehicle equipment standards to administrative recordkeeping, and are an effort to modernize regulations that affect trucking.

Highlights among them include:

Electronic recordkeeping: FMCSA has formally clarified that Driver Vehicle Inspection Reports may be created, maintained, and signed electronically, removing ambiguous language that previously suggested a need for paper-based methods.

Safety equipment modernization: FMCSA is removing the requirement for trucks to carry liquid-burning flares and spare fuses, noting that these devices are largely obsolete or easily replaced at retail locations.

Military personnel inclusion: The “military exception” from CDL standards is now extended to dual-status military technicians, harmonizing the treatment of all personnel operating commercial motor vehicles for military purposes.

The American Trucking Associations and the Owner-Operator Independent Drivers Association weighed in on most of the proposals, describing many of the changes as “commonsense regulatory reform.”

FMCSA emphasized, however, that while the slate of operational reforms collectively will make life easier for drivers and carriers by reducing administrative burdens and potentially extending the useful life of older equipment, the economic impact of each specific rule is expected to have a small or negligible effect on costs and savings for the industry.

U.S. e-commerce as a share of Walmart’s total sales reached a record 23% in the fourth quarter after growing 27% year over year and drove the majority of its sales growth, underscoring the retail titan’s ability to compete with Amazon in the online and delivery space.

For the full year, e-commerce sales exceeded $150 billion for the first time, up 5.5% from two years ago, Walmart (NASDAQ: WMT) said in its fourth-quarter earnings report on Thursday. The e-commerce operation has well exceeded the breakeven level. Management said e-commerce was profitable each quarter last year in the U.S. market, with roughly double-digit incremental margin growth as the company enjoys the economies of scale from its marketplace infrastructure.

Online sales were a mix of store-fulfilled pick up and delivery, as well as the third-party marketplace. In the United States, sales through store-fulfilled delivery channels grew more than 50%. Marketplace sales were up 20%, with a record 52% of sellers utilizing Walmart fulfillment services.

Customers took advantage of Walmart’s fast-delivery service, with orders delivered in under three hours increasing more than 60% for the year, President and CEO John Furner said during a call with analysts. At Walmart U.S., 35% of store-fulfilled orders were delivered in under three hours in the fourth quarter. And the company is averaging delivery in less than an hour when customers opt for express delivery

A new AI-powered agentic shopping assistant called Sparky is helping U.S. customers fill their digital cart with an average order value about 35% higher than non-Sparky customers.

“When Sparky builds a basket, we execute it through fast delivery, pickup, or in store, turning AI engagement into immediate physical outcomes. And as we expand Sparky across experiences like voice, in store, and through services, we expect continued acceleration in customer adoption and the impact on commerce,” said Furner.

Walmart’s e-commerce sales globally increased 24%, with the international business lagging the U.S. at 17% growth. In China, e-commerce sales grew 28% and represented more than 50% of the sales mix in that market. Flipkart, an e-commerce and quick-delivery platform in which Walmart owns a more than an 80% stake, is delivering orders in less than fifteen minutes across more than 30 cities in India. And Sam’s Club U.S. doubled growth in club-fulfilled delivery sales, according to management.

During the previous quarter, the retailer’s e-commerce sales increased 27% year over year.

Overall, Walmart said quarterly revenue increased 5.6% to $190.7 billion. Operating income was $800 million, up 10.8%. Net sales for Walmart U.S. was $129 billion. For the full year, operating income only grew 1.6% to $500 million because Walmart recorded two quarterly losses.

Strong inventory management

Technology, artificial intelligence and automation helped Walmart keep inventory growth to half the rate of sales growth for the year, helping to keep a lid on costs.

“In Walmart U.S., approximately 60% of stores are receiving some freight from automated distribution centers, and approximately 50% of e-commerce fulfillment center volume is automated. This enables better visibility into what inventory we own and inventory we can access and also improved our labor productivity. With the proximity so close to customers, we’re increasingly leveraging stores as digital fulfillment nodes to move inventory faster and more efficiently than ever before,” said David Guggina, the head of Walmart U.S.

The number of facilities getting some form of automation will continue to grow this year as old conveyor systems are retired. Meanwhile, the retailer recently began deploying warehouse automation to Sam’s Club U.S. and its international operations, he added.

The combination of hand-held scanners in stores with computer vision to map stocks, and careful seasonal ordering by buyers also helped Walmart manage its inventory levels.

Detroit rolls out Gen 6 engine portfolio for Freightliner and Western Star trucks

DETROIT — Daimler Truck North America’s Detroit powertrain brand unveiled its Gen 6 heavy-duty engine portfolio Thursday.

Engineers showed the updated DD13, DD15 and DD16 engines earlier that week at the company’s manufacturing facility in Redford Township, Michigan.

Detroit designed the lineup to meet the Environmental Protection Agency’s strict 2027 emissions standards. Executives also say the changes bring meaningful fuel-efficiency gains for fleets working through the longest freight recession on record.

Fleets are holding equipment longer than normal trade cycles. They watch every capital dollar. As a result, the value question becomes especially important right now.

“At a moment in the marketplace where customers are particularly focused on value, their capital, where they utilize their capital, then the next decisions about stepping into 2027 are really focused on what do I get on my investment? Is it just an emissions change, or is there more value there?” said David Carson, senior vice president of sales and marketing at Daimler Truck North America. “There’s a tremendous amount of value in this product.”

The engines will be available for all heavy-duty Freightliner and Western Star trucks. DD13 and DD15 will be available beginning in January 2027, with Gen 6 DD16 production following in January 2028.

“Freightliner and Western Star customers depend on Detroit to operate reliably, efficiently and powerfully, and we’re honored by the trust placed in both the Detroit brand and the DD13, DD15 and DD16 engines to help navigate past transitions as well as this next one,” Carson said. “With our Gen 6 engines, we have a successor that builds on years of proven performance to be prepared for 2027 and beyond.”

This is the sixth generation of Detroit’s Heavy-Duty Engine Platform. Detroit first introduced it in 2007 as a clean-sheet design. More than 1.2 million of these engines now run across North America and global markets.

Detroit completely redesigned the fuel system. The company switched to an oil-lubricated high-pressure pump that delivers 2,500-bar common rail pressure with simplified non-amplified injectors. It also added Miller cam timing and an electronic variable-displacement oil pump to cut parasitic losses.

“Our customers can’t always control the quality of the fuel that they have access to,” said Steve Collins, director of field sales engineering for Detroit. “A robust fuel system improves efficiency and reliability.”

Engineers added an asymmetric intake port to increase swirl. They combined this change with Miller cam timing. As a result, the engines improve combustion and raise compression ratios. Detroit projects a 3 percent improvement in real-world fuel efficiency.

To meet the tougher NOx rules, Detroit added a pre-Selective Catalytic Reduction (pre-SCR) system upstream of the familiar aftertreatment system. It uses the same proven technology fleets already know.

“It became very clear to us that once 35 milligram was decided on, the pre-SCR strategy was the best way to go,” said Greg Braziunas, head of powertrain engineering for North America. “This known technology delivers familiarity, robustness and the best value for customers.”

The thermal control valve, once available only on the DD13, now comes standard on every Gen 6 engine. Braziunas said it has greatly reduced or even eliminated the need for parked regens on many vocational trucks.

Detroit kept most familiar Gen 5 power ratings. However, it added three new options: a 505-horsepower, 1,750 pound-feet torque DD13 for vocational customers and two DD15 ratings at 425 and 455 horsepower with 1,900 pound-feet of torque for more downspeeding.

The company tested the platform for seven years and more than 8 million real-world miles in temperatures from minus 40 to 130 degrees Fahrenheit. Oil maintenance and diesel particulate filter ash-cleaning intervals remain the same as Gen 5.

All Gen 6 engines are built at the Redford Township plant. That facility recently received a $285 million investment supported by Michigan Economic Development Corp. incentives

WASHINGTON — New guidelines released by the Federal Motor Carrier Safety Administration reveal just how aggressive the agency plans to be in enforcing its final rule cracking down on non-domiciled CDLs.

The new FAQ provides details on a federal purge of unvetted foreign drivers, introducing mandatory operational changes not detailed in the final rule issued last week.

Targeting “temporary” credentials for revocation

The most significant escalation in the new directives targets the nomenclature found on the license. Under the final rule, all eligible licenses must unmistakably display the term “non-domiciled.”

However, the new FAQ goes further, revealing that licenses marked with terms like “temporary” are no longer just out of date but are non-compliant. FMCSA is now “strongly encouraging” states to immediately revoke and reissue these specific credentials rather than waiting for them to expire.

In addition, simply adding a “non-domiciled” restriction code to a standard design is explicitly forbidden, according to the new directives. Instead, the word must be “conspicuously and unmistakably” located on the face of the card.

Spouses and asylum seekers formally blocked

The agency has also slammed the door on derivative and pending immigration statuses that were previously gray areas.

Specifically, the FAQ clarifies that those with E-2S status – spouses of treaty investors – are not eligible for a non-domiciled CDL. Similarly, state agencies are strictly prohibited from accepting Form I-797C (Notice of Action) as evidence of status, even if it serves as a receipt for a pending immigration benefit.

Only those in H-2A, H-2B, or E-2 status with an unexpired foreign passport and an I-94 showing a clear “Admit Until Date” may hold these credentials.

Final Rule vs. FAQ: Key Mandates

Final Rule

New Directives

Nomenclature

Required “Non-domiciled” marking on license face.

Mandates immediate revocation of any licenses marked “Temporary”.

Eligibility

Limits to H-2A, H-2B, and E-2 statuses.

Explicitly excludes E-2S (spouses) and clarifies I-797C is insufficient.

Duplicate/Address

Generally mandates in-person issuance.

Clarifies that even simple address changes and duplicates must now be in-person only.

Deadlines

48-hour document production rule for states.

Clarifies the 48-hour window includes weekends and holidays.

Technology

Requires SAVE query.

Reveals VLS is being phased out and warns states against relying on legacy systems.

Hard operational deadlines for states

The new directives significantly ramp up federal oversight of state agencies. The final rule requires states to produce licensing documents within 48 hours of an FMCSA request. The FAQ now clarifies that this 48-hour window includes weekends and holidays, leaving no room for administrative delays.

FMCSA also signaled a significant technological shift: the directives revealed that the Verification of Lawful Status (VLS) system used by some states is being phased out.

“Even if VLS is proven to be the functional equivalent and a pass-through for SAVE [Systematic Alien Verification for Entitlements], USCIS [U.S. Citizenship and Immigration Services] has confirmed that VLS is being phased out and will no longer support updated features of SAVE,” the guidelines state.

“Therefore, states must continue to ensure that a VLS query will return the equivalent real-time results as an SDLA’s direct query to SAVE, even as VLS is phased out” or face non-compliance findings.

In-person mandate for carriers

For motor carriers, the FAQ reinforces the need for immediate audits of driver qualification files. Because the FMCSA now classifies “reinstatements” (such as returning a driver to service after a medical downgrade) as a new “issuance,” these transactions must now be handled in-person only and require fresh evidence of H-2A, H-2B, or E-2 status.

Asia-U.S. container rates continue to fall as industry change swirls

Analyst Freightos said Asia-U.S. East Coast prices in the latest week fell 12% to about $3,000 per forty foot equivalent unit (FEU) and back to early December levels before pre-Lunar New Year demand picked up.

The holiday is a traditional fallow period for trans-Pacific demand as China factories close for several weeks.

Asia-North Europe rates slid 5% to about $2,400 per FEU, also back to December levels while prices to Mediterranean ports fell 4% to $3,600 per FEU. The latter remains several hundred dollars above the December mark.

Freightos (NASDAQ: CRGO) is a contributor to the SONAR data platform.

Elsewhere, the Trump administration released its long-delayed Maritime Action Plan that includes protectionist policies aimed at reviving domestic shipbuilding. Among other steps, it proposes port fees of between one and twenty five cents per kilo of freight arriving on foreign-buillt vessels. Analyst Lars Jensen and others estimate these fees would range from about $150 per FEU for a one cent per kilo charge to as much as $3,750 per FEU.

The White House offered no timeline for implementation of the plan. Two maritime bills were introduced in Congress after President Donald Trump prioritized shipbuilding plans this past April, but there has been little progress since.

Freightos analyst Judah Levine said a side effect of Trump’s ongoing trade has been a diversification of trade partners and growing commerce between non-U.S. economies. “This trend of exporting countries seeking alternative sources for growth is also being reflected in ocean freight flows, with carriers shifting some capacity and resources to Far East-West Africa lanes as demand increases,” Levine said. “This shift may also be a factor in recent service reductions on the trans-Atlantic.”

In one of the biggest deals to hit the container market in years, Germany’s Hapag-Lloyd has agreed to acquire Zim (NASDAQ: ZIM) of Israel for $4.2 billion. Levine noted that the deal won’t move Hapag-Lloyd from its spot as the world’s fifth-largest carrier by capacity. But adding 10th-ranked Zim would push it closer to the number four spot held by Cosco (1919.HK) of China, with more than 3 million TEUs combined.

“That capacity will help Hapag-Lloyd, whose Gemini Cooperation partner Maersk (MAERSK-B.CO) was also a bidder, increase its overall market share, particularly on the Far East-North America and trans-Atlantic lanes,” Levine said.

The Dumping Ground: Insuring America’s Most Dangerous Truckers. No Questions Asked.

I knew we had significant concerns about trucking insurance, given the rising underwriting absence rates. Instant issue policies are increasingly prevalent, particularly among the worst-performing fleets. What I found was a massive hole in the regulatory framework so large that you could drive a truck through it. Based on the numbers, someone already has. About 589,690 times.

I’ve held a CDL for over 25 years. I’ve managed fleets, owned fleets. I consult for Fortune 500 carriers; I’ve overseen large, multi-entity private equity fleets; I’ve testified as an expert witness in highway accident litigation; and I have spent the better part of my career within the compliance machinery of American trucking. I thought I understood how the system worked. Most would have you believe I know more about the U.S. truck insurance market than most. Then I started pulling that data.

An analysis of 2.8 million insurer-carrier relationships in FMCSA data reveals extreme crash concentration: the top 5% of carriers by insurer portfolio risk account for 31.9% of all crashes and 31.8% of all fatalities. The reason? No federal or state law requires insurance companies to evaluate a motor carrier’s safety record before issuing a policy. The $750,000 federal minimum hasn’t changed since 1980. The result is a system where insurance is a financial barrier to entry but not a safety gate.

What the data says

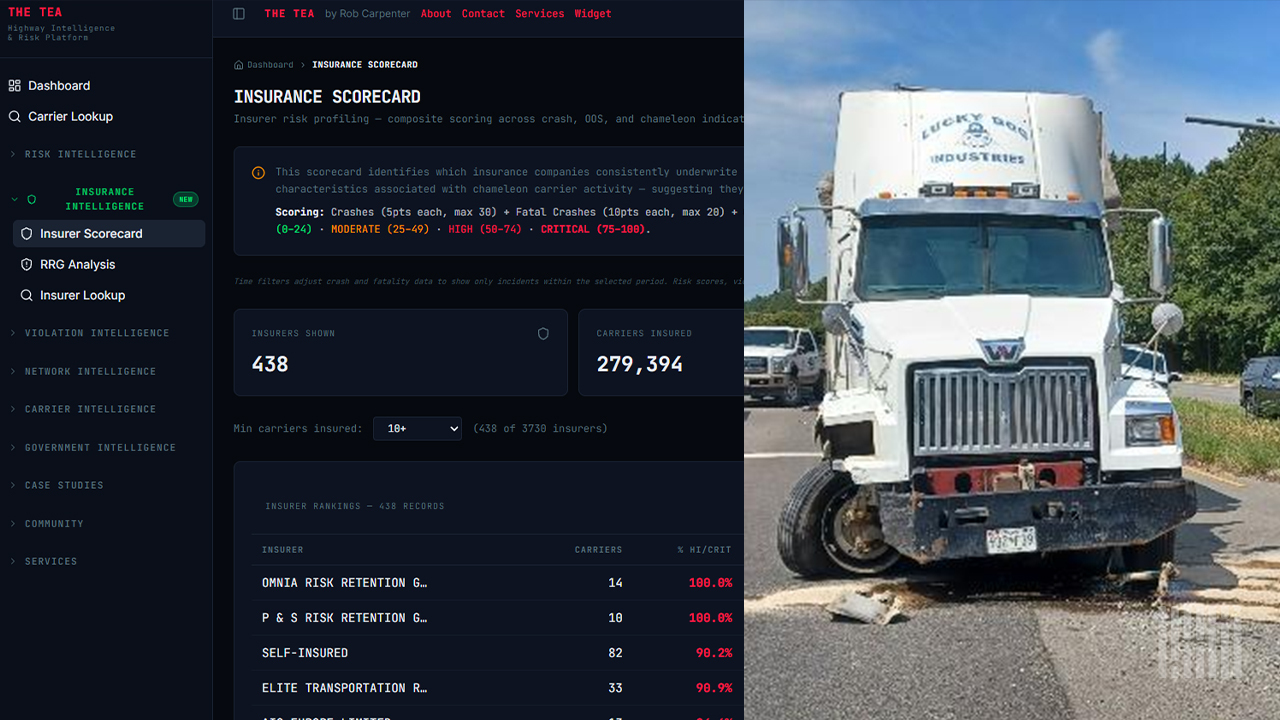

I analyzed 2.8 million insurer-carrier relationships in the FMCSA’s public data. You can see my insurance scorecards on my site here; each trucking carrier profile also includes an insurance risk rating. Every active insurance filing for every interstate for-hire motor carrier in the United States. Then I scored each carrier using a peer-normalized risk framework that evaluates crash severity, inspection quality, authority stability, and compliance patterns within fleet size cohorts. The scores were aggregated to the insurer portfolio level.

Insurer portfolios in the highest-risk tier, with average risk scores between 21 and 50 on a 100-point scale, cover just 1.8% of all carriers. But those carriers account for 16.9% of all crashes and 16.6% of all fatal crashes in the dataset. The weighted crash rate per carrier in this tier is 58.9. In the lowest tier, it’s 1.13. That’s an insane difference.

When I ranked carriers by the riskiness of their insurer’s portfolio and computed cumulative crash shares, the concentration curve was almost vertical. The top 5% of carriers account for 31.9% of all crashes and 31.8% of all fatal crashes. At 25%, the curve captures 70.1% of both.

One-quarter of carriers, identifiable by their insurers, are involved in seven out of every 10 truck crashes in America.

The long tail is where the bodies are

I split the insurance market into two segments: the 50 largest insurers by carrier count, and everybody else. The 50 biggest cover 55.2% of carriers. The remaining 3,680 insurers account for the remaining 44.8%.

The top 50 have a weighted average risk score of 6.24 and a crash rate of 3.22 per carrier. They account for 27.7% of crashes. The long tail, those 3,680 smaller portfolios, has a risk score of 9.55, a crash rate of 10.32 per carrier, and accounts for 72.3% of all crashes. That’s 72% of crashes from 45% of carriers, concentrated in the segment of the market where surplus lines, specialty programs, and residual market placements are located.

This is the predictable result of a regulatory structure that imposes no quality gate on the insurance procurement process.

Nobody has to check

No federal or state law requires an insurance company to evaluate a motor carrier’s safety fitness before binding a commercial trucking policy.

Not FMCSA. Not your state insurance department. Nobody.

FMCSA sets the floor for how much coverage a carrier must carry: $750,000 for general freight, established during the Reagan administration and never adjusted. The agency checks that a BMC-91 form is on file. It does not check, and has no authority to check, whether the insurer that filed the form reviewed the carrier’s crash history, BASIC scores, out-of-service rates, driver qualification files, or anything else before issuing the policy.

Under the McCarran-Ferguson Act of 1945, insurance regulation is exclusively a state matter. State insurance departments regulate insurer solvency, licensing, rate filings, and claims practices. They do not mandate that insurers conduct prospective underwriting of individual policyholders. The decision to underwrite, and the rigor of that underwriting, is entirely at the insurer’s discretion.

Some insurers choose to underwrite. Group captive programs require on-site risk-control assessments, reviews of driver qualification files, evaluations of maintenance programs, and continuous monitoring of members. Carriers that underperform get placed on alert status. Carriers that don’t improve get removed.

Other insurers don’t. An algorithmically priced, instantly bindable policy from a major instant-issue provider can be obtained without a single human reviewing the carrier’s FMCSA record. The carrier self-reports. The algorithm prices. The policy binds. Authority activates. Trucks roll.

Both pathways are perfectly legal. The regulatory framework doesn’t distinguish between them.

The market of last resort

There’s another piece to this puzzle that almost nobody in trucking talks about, the assigned risk market.

AIPSO, the Automobile Insurance Plans Service Office, has administered the residual market for automobile insurance since 1973. In most states, carriers that cannot obtain coverage in the voluntary market may apply to the Commercial Automobile Insurance Procedure (CAIP). The state plan assigns the carrier to an insurer in proportion to that insurer’s share of the voluntary market. The assigned insurer must provide coverage regardless of the carrier’s risk profile.

The insurer has no discretion to reject the carrier. Assignment is mandatory.

This means that every insurer writing commercial auto in a given state can be forced to cover carriers that the entire voluntary market has already evaluated and rejected. The premiums are higher, but the coverage is issued. The carrier gets its BMC-91 filed. FMCSA activates the authority.

Now consider what happens if anyone ever proposes mandating underwriting standards. Every carrier that fails the assessment gets pushed into the assigned risk pool. The same pool designed to accommodate a small residual population now absorbs potentially tens of thousands of carriers with documented safety problems. The assigned insurers involuntarily bear the risk. The premiums go up. The losses go up. And the pool was never built for that kind of load.

This isn’t hypothetical. In 1992, the New Jersey Automobile Insurance Plan sued over widespread fraud in the Pennsylvania and New Jersey commercial auto assigned-risk plans, in which intermediaries had exploited loopholes in AIPSO-drafted rules to secure substantial premium reductions for trucking companies, shifting losses to assigned carriers. The case went to federal court and lasted for years. The assigned risk system was never designed to serve as a dumping ground for America’s riskiest trucking operations. But that’s exactly what it becomes when the voluntary market has no obligation to screen.

A $750,000 rubber stamp

The federal minimum levels of financial responsibility for motor carriers were set under the Motor Carrier Act of 1980. For general freight, the floor is $750,000 per occurrence. It has not been adjusted in 45 years.

Adjusted for inflation alone, that $750,000 should be approximately $2.2 million. The Truck Safety Coalition, citing FMCSA’s own 2014 review, argues it should be $10 million per occurrence. Their reasoning is worth quoting: the minimums should be “set sufficiently high to give the insurance companies a reason to set realistic underwriting standards that would reward safe companies and identify unsafe operations.”

That sentence reveals the intended but unrealized function of the federal minimum. Congress didn’t design the insurance requirement merely as financial protection for crash victims. It was supposed to be a mechanism that incentivized private-sector underwriting. If the minimum were high enough, insurers would have a financial incentive to evaluate carriers before binding coverage, because the potential loss exposure would justify the cost of risk assessment.

At $750,000, a fraction of the cost of a single fatal truck crash in litigation, the incentive is insufficient. The average verdict in a nuclear truck crash case now exceeds $20 million. The minimum coverage limit is 3.75% of that. You could not design a system more perfectly calibrated to discourage underwriting if you tried.

Risk Retention Groups: one state’s oversight, 50 states’ risk

The Liability Risk Retention Act of 1986 authorized Risk Retention Groups, liability insurance companies owned by their members, to operate nationally under the supervision of a single state. An RRG domiciled in Vermont or South Carolina can insure trucking companies in all 50 states while being regulated by only its home state’s insurance department.

Non-domiciliary states may require registration and tax payments, but they may not impose additional licensing, underwriting, or solvency requirements beyond those of the domiciliary state. The GAO found in 2005 that this created “a regulatory environment characterized by widely varying state standards.”

Here’s the part that matters most: RRG policies are not backed by state guaranty funds. Every RRG policy must include a disclosure that guaranty fund protections are unavailable. If a trucking-industry RRG becomes insolvent, the crash victims whose injuries were supposed to be covered by those policies may face uncollectible judgments. The LRRA’s preemption creates both a regulatory and a consumer-protection gap.

What should we do about it?

Raising the minimum is necessary but not sufficient. If an insurer can bind a $10 million policy on a carrier with 50 crashes without reviewing the carrier’s FMCSA record, the underwriting gap persists. The premium goes up. The screening doesn’t.

The more direct intervention is to mandate minimum underwriting standards. Either through FMCSA rulemaking or through a model act adopted by states via the NAIC, require that commercial auto insurers conduct a minimum safety review before binding coverage on a for-hire interstate motor carrier. The requirement doesn’t have to be complicated: review FMCSA safety data, document the risk assessment, and maintain ongoing monitoring conditions. Convert the insurance barrier to entry from a purely financial requirement. “Do you have a policy?” Should be turned into a safety quality requirement: has someone evaluated your operation?

Any mandatory underwriting regime must address the assigned risk market. Carriers that fail the assessment will be pushed into the residual pool. The current AIPSO-administered plans were not designed for that volume. Options include tiered assigned-risk premiums that reflect actual loss experience, mandatory safety improvement plans as a condition of assigned-risk coverage, and federal coordination with state plans to ensure that the residual market doesn’t become a regulatory bypass.

FMCSA already has the data to act. The insurance filing data is in their systems. Insurer portfolio risk could be incorporated into the Inspection Selection System tomorrow. A carrier insured through a portfolio in the top risk tier may receive prioritized inspection, investigation, or compliance review. No new data collection required. No new legislation needed. Just a decision to use what’s already there.

This is why I built THE TEA Intel.

THE TEA is an insurance intelligence and carrier risk scoring platform. It doesn’t just score carriers; every carrier vetting tool does that to some degree. THE TEA scores the insurance companies themselves. It uses the same peer-normalized methodology described in this article, crash severity, inspection quality, authority stability, and compliance patterns, benchmarked within fleet-size cohorts, and applies it at the insurer portfolio level. You can see which insurers are covering the highest concentration of high-risk and critical-risk carriers. You can see which Risk Retention Groups are writing policies for carriers that share VINs, officers, phone numbers, and addresses with shut-down operations. You can pull a DOT number and see not just that carrier’s risk score, but the risk profile of every other carrier insured by the same company.

That has never existed before. Not from FMCSA. Not from any commercial carrier vetting product. Not from the insurers themselves.

When the data shows that 13 insurers have 500-plus carriers each classified as high or critical risk, that’s intelligence the market has never had. When you can map which carriers in the worst-performing insurer portfolios share common ownership networks, that’s not carrier vetting anymore. That’s risk control intelligence. And it’s the kind of intelligence that insurance underwriters, captive group managers, brokers, shippers, and regulators have been making decisions without for decades.

THE TEA doesn’t replace underwriting. It gives underwriters, risk managers and compliance professionals the data layer that should have existed all along, the ability to see not just what a carrier looks like in isolation, but what the carrier’s insurer portfolio looks like, what that portfolio’s crash concentration looks like, and whether the carrier is sitting inside an insurer book of business that has a documented pattern of covering the industry’s worst performers. That context shifts the conversation from “Is this carrier safe?” to “Who else is standing next to this carrier in the same insurance pool, and what does that tell us?”

So What?

Based on a scoring model applied to 2.8 million records and the resulting output, the information exists to identify where crash risk is concentrated. It is visible. It is measurable. It is sitting in publicly available federal data.

The regulatory framework simply does not require anyone to use it.

That is not a failure of data or technology. It is not a failure of the insurance market. It is a failure of regulatory design, a system built in 1945, expanded in 1980, fragmented in 1986, and never updated for a world in which 5,936 people die on American highways every year in truck crashes. The patterns in this data are not hidden. They are just ignored.

It’s time to stop ignoring them.

Autotech Ventures bets big on hard-to-copy logistics startups

LAS VEGAS — Autotech Ventures is placing its chips on logistics startups that can’t easily be copied. It’s a strategy its managing director says separates lasting winners from the crowded field of AI solutions flooding the market.

Numerous AI-powered freight technology companies were showcased at Manifest 2026.

The early-stage venture capital firm manages roughly $600 million and focuses exclusively on industrials and transportation. Logistics and the supply chain represent a significant portion of its portfolio.

Its limited partners include major global manufacturers and logistics companies, creating what Burak Cendek calls the firm’s “secret sauce.”

“We connect our founders with business development opportunities within our LP base and extended network,” Cendek said. “Think of it as car manufacturers, parts manufacturers with huge supply chains, and logistics companies. We work very closely with them.”

That network has helped fuel investments in freight intelligence platform GenLogs, logistics AI productivity platform Augment and other emerging players including BasicBlock, KlearNow and Retail Ready.

Cendek describes GenLogs as “fresh air” in a landscape cluttered with easily replicable agentic AI tools. The company exemplifies what he calls an “n of one” business, something with no direct equivalent in the market.

“They have a very big moat with their network — nobody else has that. Nobody else has this data,” Cendek said. “It’s not just the data — it’s also the data science you apply on top of that data to make sense of it.”

Cendek notes the distinction matters because entry barriers for application-layer AI have collapsed. Building an AI tool has become straightforward; building something defensible has not.

“When we looked at agentic AI solutions, we realized this is easily replicable,” Cendek said. “You can get traction because there’s clear ROI, but you’ll have tens and hundreds of competitors, which is going to impact pricing power down the road. You’re going to start undercutting each other.”

For Augment, Autotech saw a different proposition: a holistic platform rather than a narrow point solution. Cendek noted that enterprise partners don’t want to manage fragmented AI tools that handle single workflows in isolation.

“You cannot just do one single workflow, because when we talk to enterprise partners, they don’t want to deal with four or five different AI solutions. It becomes messy — they don’t talk to each other,” he said.

Augment’s founder, Harish Abbott, previously sold logistics technology company Deliverr to Shopify for $2.1 billion. Cendek called him “a phenomenal operator” whose vision for an end-to-end freight platform attracted significant capital and aggressive hiring.

“Enterprises love that because it fits neatly into their AI strategy, which many are still figuring out. Augment is a good partner to figure it out with them,” he said.

The broader shift threatens traditional software gatekeepers. Cendek believes the value of being a system of record is declining as AI extracts more value from workflow automation and context.

“In the past, ERPs and TMSs locked in your data — once they had it, it was hard to move. I think that value will decline because the real value is making sense of the data,” he said.

Looking ahead, Cendek sees physical AI and robotics as the next investment frontier. Falling hardware costs and improved software now allow robotic systems to be taught new skills faster and cheaper than traditional warehouse automation ever permitted.

“AI is on its path, but in logistics, you’ll capture significantly more value once AI reaches the physical layer: automating warehouses, loading and unloading,” he said. “That’s the next chapter.”

The deal flow reflects these dynamics. Autotech Ventures now reviews approximately 7,000 startups annually. That is up from 1,000 six years ago, forcing the firm to deploy its own AI tools to manage the explosion.

Cendek’s advice for separating hype from substance: Look past raw revenue momentum.

“If not defensible, it can disappear when a better or cheaper solution arrives,” he said. “Sustainability, health and defensibility of revenue matter.”

Canadian firm to acquire breakbulk, steel terminal at Mexico’s Port of Altamira

Logistec Corp., a Montréal-based marine and logistics provider, has entered into an agreement to acquire 100% of IPA Terminal, a breakbulk and steel handling facility at the Port of Altamira, marking the company’s first move into Latin America.

The transaction, announced Tuesday, aims to position Logistec as a broader global multi-purpose marine terminal operator and expands its presence beyond its established North American footprint, company officials said.

“This expansion is a defining moment for Logistec, as we position our organization for accelerated international growth,” CEO Sean Pierce, said in a news release.

“Mexico is a dynamic market, and by acquiring IPA, we are extending our reach, connecting our network to key industries, delivering value-added cargo solutions and opening new global opportunities for our customers and partners.”

Terms of the transaction were not disclosed. Completion of the transaction is subject to regulatory approval by Mexican authorities.

IPA Terminal — which includes IPA, ATEMSA, SMA and STEEL — is described as a pivotal hub in the Gulf of Mexico specializing in breakbulk and steel commodities. The facility serves major industrial customers and regional supply chains with modern infrastructure, deepwater access and a skilled workforce.

The Port of Altamira is an industrial port facility located on Mexico’s coast on the northwest side of the Gulf of Campeche. It is located in Altamira, Tamaulipas, about 56 miles from the U.S.-Mexico border.

The port saw 18.5 million tons of cargo in 2025, according to Mexico’s federal port administration. Altamira handles everything from containerized cargo, liquid/dry bulk, petrochemical fluids, liquified natural gas and specialized oversized project cargo. It is a leading port for vehicle exports and imports (over 300,000 units annually).

Logistec currently operates across a North American network of 63 ports and 86 terminals, providing bulk, breakbulk and container cargo handling, as well as logistics services including trucking and warehousing.

TFI already seeing a tough set of first quarter numbers

The TFI International fourth quarter 2025 earnings call took place in the middle of the first quarter of 2026, but the company’s two management representatives on the forum made it clear that the first three months of the year have not been going well for the trucking conglomerate.

After posting adjusted earnings per share of $1.09 in the first quarter, which topped the 80 to 90 cents that TFI had projected for 4Q on its third quarter earnings call, TFI said it expected its adjusted first quarter earnings to be 50 cents to 60 cents per share.

“This is down year over year versus 2025, because we’re still in a transition environment,” CEO Alain Bedard said on the conference call. TFI had adjusted net income in the first quarter of 2025 of 76 cts/share.

David Saperstein, TFI’s CFO, said the decline would be created in part because of about a 250 basis point decline in the company’s U.S. LTL operations, which has been the focus of attempted improvement at TFI for several years. But Saperstein added that a first quarter decline in general was not unusual.

“Quarter one is unique in the year in that it’s very back end-weighted to March, so it’s very difficult to get a sense for the trends based on January and the first half of February,” Saperstein said.

Hard hit by weather

But the natural decline has been exacerbated by weather. Saperstein said TFI has probably lost about 100 basis points of U.S. LTL margin because of the weather and its impact on both revenue and costs. For example, Saperstein said overtime expenses have risen this quarter for weather-related issues.

“We’re estimating that we’ve lost like $5 million to $6 million already on the weather,” just through extra overtime and inefficiencies and cleaning up the dock and all that cost,” Saperstein said .

He said January was “very, very difficult, both from a volume perspective and from a cost perspective. But LTL volumes improved in February, he added, and it may turn out that first quarter 2026 volumes are flat to the numbers from 2025,” he added. “We’ll see how the pricing follows as it relates to that, but we can see that the volumes are up.”

Stock market reaction to the earnings Wednesday was relatively muted. TFI stock (NYSE: TFII) closed down 93 cents, or 1.49% to $61.67. The S&P 500 was up 0.56% for the day.

TFI’s stock is down 15.3% in the last year and 10.55% in just the last month, the latter number driven in part by the general logistics and trucking selloff that occured last week.

For the last three months, TFI is up 21.18%, per Barchart data.

What’s up in specialty truckload

While most TFI earnings calls focus on LTL and in particular the company’s U.S. LTL segment, its truckload operations were a topic of more discussion than usual.

The call featured significant focus on TFI’s specialty truckload segment, a business that includes the flatbed operations acquired by TFI when it purchased Daseke in late 2023.

In the company’s slide presentation released in conjunction with the call, TFI said the specialized truckload operations are 35% of the company’s total revenue. What it described as “conventional” truckload is only 4% of total revenue.

Bedard said an OR of 93% for the company’s truckload segment, which is what it reported in the fourth quarter, is “not acceptable, absolutely not.” But he also blamed that on “market conditions.”

Bedard said TFI is “not a van carrier that moves retail freight for a Walmart or Amazon. We move steel, we move aluminum, we move building materials. That’s our core.”

The CEO said he wants to see that group begin targeting freight business tied to the construction of data centers.

For example, Bedard said TFI is working with Bechtel on the construction of a data center. TFI also made a small acquisition late last year–the name of the company was not identified and could not be found in any TFI SEC filings–that is giving TFI an entree into other projects.

“What we’re trying to do is build some kind of a recipe partnering with the builder of those centers,” Bedard said. “And then once this data center has been completely built, they will need servicing, right? So that’s also something that we’re trying to get into and to grow that business.”

Bedard ticked off a list of several areas of growth for specialty truckload beyond data centers, including energy in general and wind and solar in particular.

Bedard also said wind–which has been targeted for rollback by the Trump administration–will be “quite active in ’26.”

As far as the outlook for existing specialty truckload operations tied to industrial activity, Berard said “hopefully that starts to move.”

Difference in drivers

Asked about government crackdowns on non-English speaking and non-domicile CDL holders, Bedard said the specialty truckload sector was protected from that in part by the demands of the job. “On a flatbed or on a tanker operations, there’s more than just driving the truck,” Bedard said. “Whereas the van, you just pick up a trailer and you drive it. So it’s much easier than to tarp a load on a flatbed.”

But Bedard said he could see the driver enforcement cascading down into more specialized types of driving. “Once the spot market moves on the van, it starts to move on the reefer, and we see also some movement on the price on the flatbed side year-over-year,” he said. “So I don’t know is it because the supply is constrained or is it the demand that’s more?”

The largest part of the business, TFI’s LTL operations, continued to struggle in the U.S. in the quarter, but with some areas of improvement.

Bedard was asked if the company had made enough changes in its LTL operations and management that it would be able to capitalize on a turn in the market.

“We are very well equipped,” he said, speaking first of an integration of financial data into a wider portion of the company’s daily operations. That software–Optym–has been implemented for incoming freight into the TFI system. Phase 2, Bedard said, will implement Optym for pickups.

“So we’re ready,” Bedard said. “We have the tools. We are improving our team on the commercial side. We have way more stability in our sales force than ever.”

Cash is king

Bedard in the first minutes of the call turned his attention to TFI’s generation of free cash flow.

“You’ve heard me emphasize many times (we are) producing strong free cash flow regardless of the cycle,” Bedard said. “At TFI, we view this free cash flow as very important given our strong track record of strategic capital allocation. We intelligently invest for the long term, even during down markets, and whenever possible, return our excess capital to shareholders.”

TFI generated $258.9 million in free cash flow in the fourth quarter, up from $207.5 million a year earlier. For the year, the figure was $832.3 million, up from $768.6 million a year earlier.

For a company with so many trucks on the road, it is notable that a slide in the company’s presentation referred to TFI as an “asset-light model.” That description was in conjunction with its capital spending, which showed capex as a percent of revenues at 1.8%, compared to 6.2% of a group of truckload peers and 9.9% for a group of LTL peers. Tighter capital spending produces larger free cash flow.

The TFI data for its comparison was for the trailing 12 months through the fourth quarter of 2025, while the peer groups’ data is through the third quarter.